Svatantra Microfin IPO: Can Ananya Birla Disrupt Microfinance?

By

Arihant Team

From a quiet 2013 startup to India’s second-largest microfinance company, Svatantra Microfin is now eyeing a massive ₹3,000 crore IPO. Backed by the Birla bloodline and global PE giants, this tech-first lender recently pulled off a game-changing acquisition to slash geographic risk. But as rural credit cycles tighten and a major merger hangs in the balance, is Svatantra truly resilient, or is the real test just beginning?

In This Article

- Introduction

- Acquisition That Redefined Svatantra’s Microfin Growth

- PE Validation

- Svatantra Microfin’s road to IPO

- Svatantra’s competitive moat

- Why Birla bloodline matters..

- Industry tailwinds

- Merger still being incomplete..

- Investor outlook

Introduction

In early 2026, Ananya Birla's microfinance institution quietly began inviting the country's top investment banks to pitch for one of the most anticipated rural finance listings in recent memory. The mandate: take Svatantra Microfin public, raise more than ₹3,000 crore, and list the company on the Indian stock exchange.

The numbers are staggering for a sector that, as recently as 2012, was fighting for survival.

The IPO structure is expected to include both a fresh issue which would directly capitalise the company and an offer for sale from existing investors. Private equity giant Advent International, which led the largest-ever PE investment in India's microfinance sector just two years ago, will look for a structured path to eventual exit. So will Multiples Private Equity and 150 ESOP holders across the organisation that are looking to create wealth by getting an exit the day the company lists.

The company is yet to file its DRHP with SEBI, which will give a deep-dive into the company including its financials, business overview, industry analysis, risks, and use of proceeds.

For now, the question serious investors are asking is simple: how did this company get here?

Open a free account today

Invest in tomorrow with just one click

Acquisition That Redefined Svatantra’s Microfin Growth

Svatantra Microfin, founded by Ananya Birla, started its operations in 2013. It provides micro-scale financing to support women-led enterprises and individuals without access to traditional banking. It focuses on fostering financial inclusion, particularly for unbanked populations needing capital for business, and maintains a very low default rate of roughly 1% The company has today emerged as one of the most differentiated process and technology-driven microfinance companies in India.

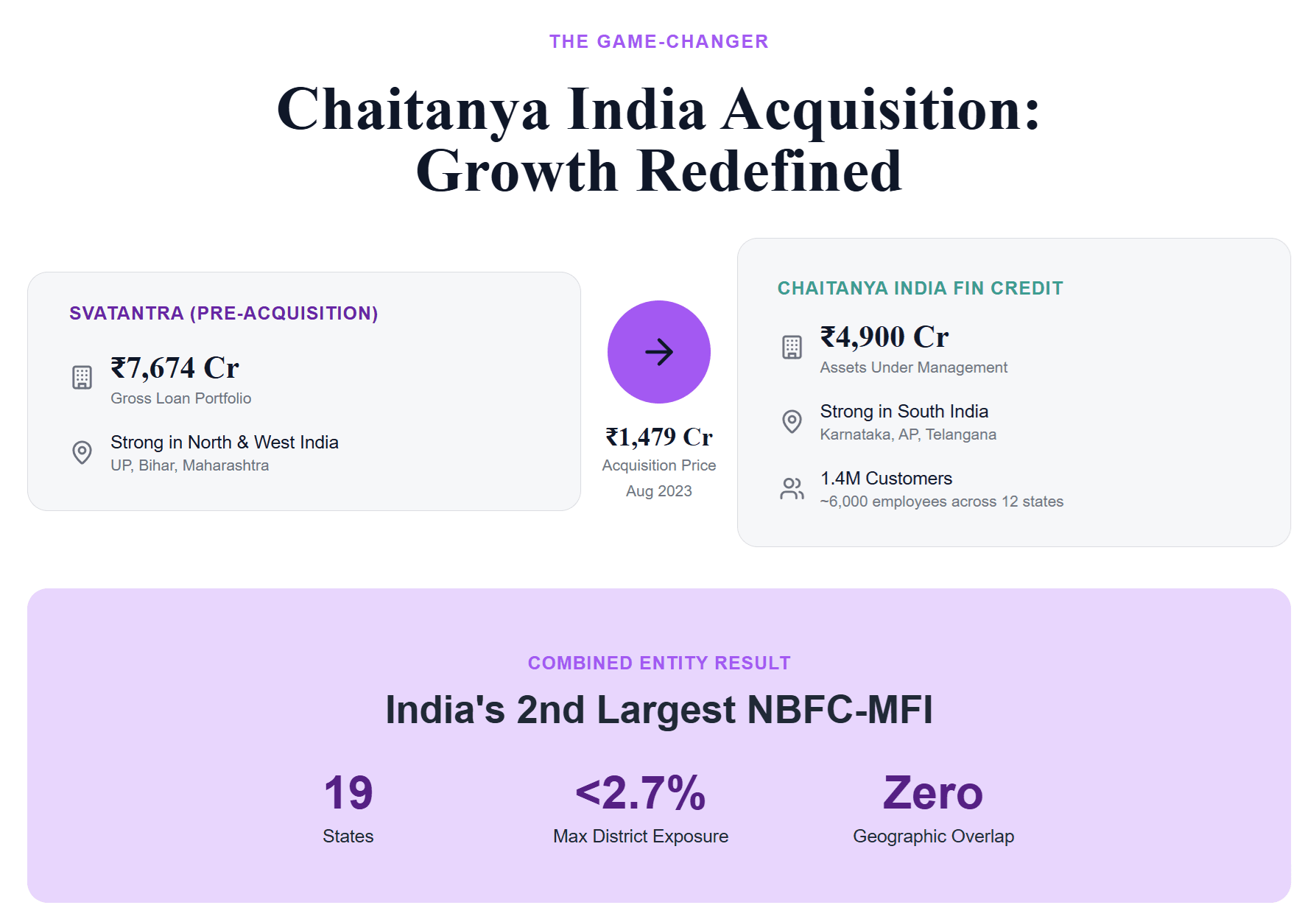

To understand how it reached this stage, it helps to rewind to mid 2023. At the time, Svatantra had built a compelling story but its loan book of ₹7,674 crore, while impressive, was not quite large enough to command the kind of public-market valuation its investors were targeting. Organic growth in microfinance is patient work; there are no viral network effects. Scale comes branch by branch, village by village.

Then a strategic opportunity presented itself. Chaitanya India Fin Credit, originally founded in 2009, had been acquired in 2019 by Sachin Bansal's Navi Group after Bansal exited Flipkart. Under Navi, the company had expanded its assets nearly sixfold, building a particularly strong footprint in South India (Karnataka, Andhra Pradesh, and Telangana). By 2023, Chaitanya carried roughly ₹4,900 crore in AUM, 1.4 million active customers across 12 states, and about 6,000 employees. The only problem? Its long-term direction inside Navi was uncertain.

That’s when Svatantra moved. On August 8, 2023, it announced the acquisition for ₹1,479 crore. By November 23, Chaitanya had become a wholly owned subsidiary. The logic was almost textbook: Chaitanya's southern stronghold barely overlapped with Svatantra's existing presence. The combined entity suddenly had its portfolio distributed across Karnataka, Uttar Pradesh, Bihar, and Maharashtra with no single district accounting for more than 2.7 percent of the gross loan portfolio. Geographic concentration risk historically one of microfinance's gravest vulnerabilities was dramatically reduced in a single stroke. Overnight, Svatantra became India's second-largest NBFC-MFI by AUM.

PE Validation

If the Chaitanya acquisition signalled ambition, the next development confirmed institutional conviction. In March 2024, Advent International and Multiples Private Equity Funds collectively invested ₹1,930 crore in Svatantra through Advent's entity Violicina Limited, the single largest private equity investment ever made in the Indian microfinance sector.

Svatantra now had world-class institutional backers, a significantly strengthened balance sheet, and the credibility that comes with marquee PE validation. The path to a public listing was no longer a possibility; it was a plan in motion.

Svatantra Microfin’s road to IPO

But to understand what Advent was buying into, you have to go back to 2010 and a crisis that nearly killed the entire industry.

2010

The Andhra Pradesh government issued an emergency ordinance after reports of aggressive loan recovery practices and borrower suicides. Loan repayments collapsed across the microfinance sector, pushing several of India’s largest MFIs to the brink of failure.

2012

RBI steps in. It introduces a comprehensive regulatory framework and creates a new category of lender, the NBFC-MFI licence with strict rules on borrower indebtedness limits, interest rate structures, and recovery practices. Ananya Birla incorporates Svatantra Microfin into this newly regulated environment.

March 2013

The RBI grants Svatantra its NBFC MFI licence; the very first institution licensed under the post Andhra Pradesh regulatory framework.

FY2014

Within its first year of operations, Svatantra reaches 10,000 customers across nine branches in two states with 0 defaults. The cashless disbursement model and mobile first field operations were established from day 1.

FY2017

ICRA assigns an A- credit rating. The company reached profitability in FY2017, less than four years after beginning operations. Demonetisation tests the portfolio.

FY2021

COVID and the government mandated moratorium stress the entire sector. Svatantra weathers it without a structural breakdown, evidence that the technology and collection infrastructure built over seven years was genuinely resilient.

FY2023

The company reports 2.2 million rural customers, 950+ branches in 19 states, and a gross loan portfolio of ₹7,674 crore. CRISIL upgrades it to “AA-”, a rating that is extraordinarily rare in microfinance and opens the door to the lowest-cost debt available in the sector.

Svatantra’s competitive moat

With so many microfinance companies with deep roots already in India, how did Svatantra rise? Let’s take a look.

- Cashless lending from day one: Every loan was transferred directly into the borrower’s bank account. When customers did not have accounts, Svatantra helped them open one, reducing cash-handling risks and creating a transparent digital record of every transaction.

- Real-time portfolio monitoring: Field officers used Android apps to record disbursements and collections instantly. This allowed the central risk team to see portfolio data live and identify repayment stress early at the branch or cluster level.

- Standardised, data-driven underwriting: A proprietary Business Rule Engine (BRE) used credit bureau and transaction data to guide lending decisions. This ensured consistent credit assessment across thousands of field officers and allowed lending rules to be updated quickly when regulations changed.

- Borrower-facing technology: Svatantra introduced apps such as Saathi and later Saksham, enabling borrowers to track their loans and make digital repayments, well before smartphone usage became common among rural borrowers.

- Joint Liability Group model: Lending still relied on the Joint Liability Group (JLG) model, where small groups of borrowers guarantee each other’s loans. Technology improved monitoring and transparency but the social accountability of the group remained the foundation of repayment discipline.

Why Birla bloodline matters..

Microfinance, at its core, is a spread business. Profitability depends on the gap between the cost of borrowed capital and the rate at which loans are extended. An institution that can borrow cheaply has a structural advantage over every competitor, it can price loans more competitively, grow faster, and still earn a reasonable return.

Svatantra entered the market with a connection to the Aditya Birla Group. That backing meant access to debt capital at borrowing costs significantly lower than most new entrants could achieve. As the company grew, its credit ratings improved steadily from A- at ICRA in 2016 to AA- (Stable) from CRISIL, with an A1+ rating on commercial paper.

Svatantra's funding base today spans six public sector banks, twenty private sector banks, non-convertible debentures, external commercial borrowings, and development finance institution loans. That diversification is itself a risk management tool.

Industry tailwinds

By FY2025, however, the microfinance sector was facing a new challenge. The rapid lending that followed the COVID recovery had left many rural borrowers overleveraged. As stress surfaced, institutions across the sector were forced to increase provisions, write off bad loans and slow growth. Several mid-sized MFIs reported sharp profit declines, leaving even the largest players stuck in cross hairs.

Svatantra’s standalone numbers which exclude Chaitanya and therefore provide the clearest comparison reflect this pressure. As of March 31, 2025, the company’s revenue from operations fell and profit before tax declined. Write-offs rose from ₹30,797 lakh to ₹38,015 lakh, while Stage 3 provisions stood at ₹15,153 lakh.

On the consolidated basis that includes Chaitanya, the picture is more encouraging: revenue from operations reached approximately ₹3,156 crore and profit before tax rose to ₹552 crore from ₹425 crore in the prior period (though that comparison is distorted by Chaitanya's partial inclusion in the earlier year). The combined AUM of ₹14,902 crore represented 13% YoY growth even as the industry overall was shrinking.

It’s proving the acquisition of Chaitanya was worth every dime paid.. Chaitanya acted as a stabilising engine, helping sustain growth and profitability at a time when the standalone business was facing sector-wide stress.

Merger still being incomplete..

However, one significant piece of organisational housekeeping remains in progress. A two-way Scheme of Amalgamation, approved by the board in November 2024, proposes to merge Svatantra Holdings Private Limited and Chaitanya India Fin Credit Private Limited into Svatantra Microfin Private Limited.

Also, while BSE issued a no-adverse-observations letter in February 2025 and the Competition Commission of India granted approval in the same month, the RBI approval is still pending, the most consequential step.

Investor outlook

The listing now appears to be the logical next stage.

Fresh equity would support loan book expansion while reducing reliance on ₹410 crore of subordinated debt.

Svatantra has begun inviting investment banks to pitch for an IPO expected to raise more than ₹3,000 crore, with listing plans on the NSE and BSE. The offer structure may include both a fresh issue and an offer for sale, allowing early investors such as Advent International and Multiples to begin their exit while raising new growth capital.

The company enters the market with several strengths: a diversified portfolio across 19 states, strong capitalization with CRAR of 29.61%, and access to low-cost funding through its AA- rating.

But risks remain.

Asset quality weakened in FY2025, and microfinance remains sensitive to rural income cycles, borrower over-indebtedness and political interventions such as loan waivers.

Ultimately, investors will be deciding how to value a company that combines scale, funding strength and a decade built technology platform against earnings that are still stabilising after a difficult credit cycle.

Related Topics

Important IPO terms all investors should understand before investing

Meesho IPO Opens on 3Dec - Is this ₹5,421 crores IPO worth investing?

10 Things to Know About Sudeep Pharma IPO: Date, Price, GMP & Complete Review

Canara Robeco AMC IPO: Should You Apply for MF Giant’s Public Debut?

Smartworks Coworking Spaces Limited IPO: 10 Key Things to Know Before Investing

Travel Food Services Limited IPO: 10 Key Things to Know Before Investing

Ellenbarrie Industrial Gases Limited IPO: 10 Key Things to Know Before Investing

HDB Financial Services Limited IPO: 10 Key Things to Know Before Investing

Sambhv Steel Tubes Limited IPO: 10 Key Things to Know Before Investing

Indogulf Cropsciences Limited IPO: 10 Key Things to Know Before Investing

Prostarm Info Systems Limited IPO: 10 Key Things to Know Before Investing

Aegis Vopak Terminals Ltd IPO: 10 Key Things to Know Before Investing

Schloss Bangalore Limited IPO: 10 Key Things to Know Before Investing

Belrise Industries Limited IPO: 10 Key Things to Know Before Investing

Hexaware’s Billion Dollar Markets Hits in Bear Market: Should You Invest?