Raajmarg Infra Investment Trust IPO| Should You Invest?

By

Arihant Team

Raajmarg Infra Investment Trust (RIIT), backed by NHAI, is launching a ₹6,000 crore InvIT IPO. It offers investors exposure to toll-road cash flows from operational highway assets. But can this infrastructure yield product deliver stable income? Here’s a detailed analysis of the business, risks, and investment potential.

In This Article

- Introduction

- What are InvIT?

- Business Overview

- Key IPO Details: RIIT

- RIIT IPO Objectives

- Financial Snapshot

- Peer Comparison

- Key Risks

- Investor Takeaway

- FAQs

Introduction

India has 1,46,145 km of national highways. That sounds like a lot until you realise it's just 2% of the country's total road network. Yet that 2% carries nearly 60% of all road traffic in India. 87% of all passenger traffic in India travels by road.

Roads are the backbone of how this country moves. CareEdge Research projects ₹15,50,000 crore worth of investment into national highways between FY25 and FY28, growing at roughly 11% annually.

The pipeline is enormous. And to fund it, the government needs to recycle capital from roads already built. That's where Raajmarg Infra Investment Trust comes in.

Raajmarg Infra Investment Trust (RIIT), an InvIT backed by the National Highways Authority of India (NHAI), is coming to the public markets as part of the government’s broader highway asset-monetisation push. For retail investors, this is effectively a chance to own a slice of toll-road cash flows through a listed instrument.

The trust’s ₹6,000 crore IPO will open for subscription on 11 March 2026 and close on 13 March 2026, with the price band fixed at ₹99-₹100 per unit.

But can RIIT genuinely deliver stable income from India’s busiest roads, or does the structure add more risk than the headline suggests?

Let’s find out!

Open a free account today

Invest in tomorrow with just one click

What are InvIT?

Before we get into the IPO details, let’s understand what are InvITs?

An InvIT pools investor money to buy income-generating infrastructure - highways, power transmission lines, telecom fibre. Think of it like a mutual fund, but one that owns real assets instead of stocks.

You could also bet on infrastructure by buying shares in a company like L&T. But that's a bet on their business, their ability to win contracts, build on time, and manage costs. An InvIT is different. The assets are already built and already earning. The roads are laid, the power lines are live. You're simply buying the right to collect the tolls and tariffs without any construction risk involved.

Business Overview

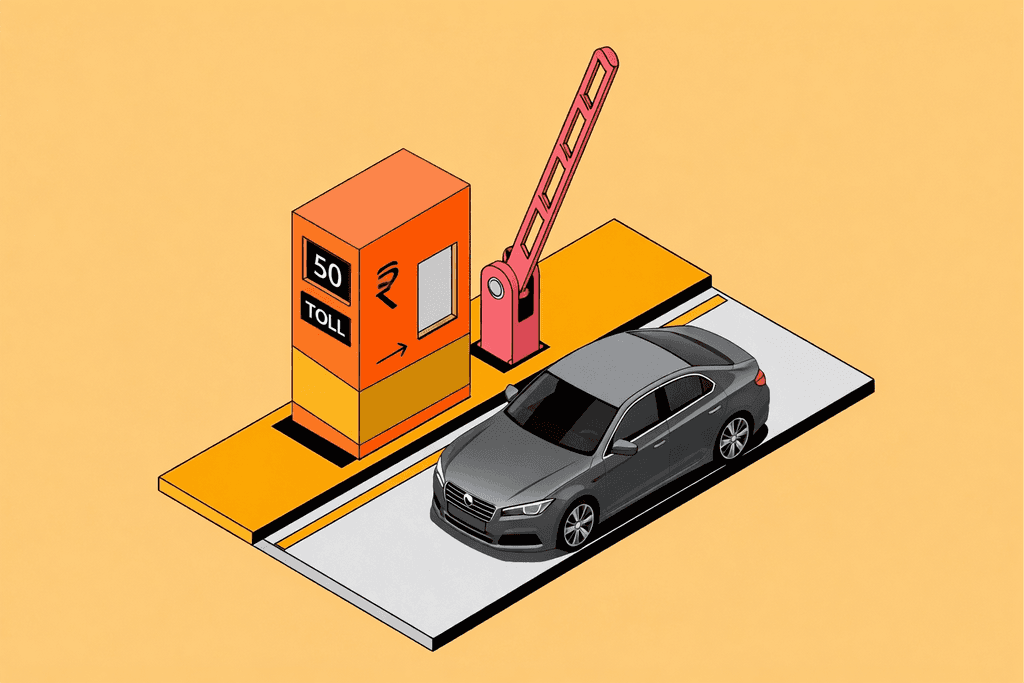

Raajmarg Infra Investment Trust (RIIT) is a government-backed infrastructure investment trust created to own and monetise operational toll roads. Sponsored by the National Highways Authority of India (NHAI), the InvIT gives public-market investors a way to participate in highway cash flows that were previously accessible mainly to institutional buyers.

In practical terms, the model is simple: the roads are already built, vehicles pay tolls to use them, and after operating costs, debt servicing and other trust-level obligations, a portion of that cash is distributed to investors.

RIIT was registered with SEBI in December 2025 and has been set up to acquire, operate and maintain highway assets transferred by NHAI under the Toll-Operate-Transfer (TOT) framework. Its starting portfolio consists of five operational road assets spanning 260.19 km across Karnataka, Tamil Nadu, Andhra Pradesh and Jharkhand. These are mature, revenue-generating stretches rather than under-construction projects, which makes the trust fundamentally a yield-oriented infrastructure vehicle rather than a development bet.

Key IPO Details: RIIT

- Issue size: ₹6,000 crore

- Price band: ₹99 - ₹100 per unit

- IPO dates: March 11-13, 2026

- Issue type: 100% Fresh Issue

- Lot size: 150 units

- Minimum investment: ₹14,850-₹15,000

- Listing date: March 24, 2026 (BSE & NSE)

- Lead managers: SBI Capital Markets, Axis Capital, ICICI Securities, and Motilal Oswal Investment Advisors

RIIT IPO Objectives

The ₹6,000 crore IPO proceeds will largely be used to fund the acquisition of the road assets from NHAI through the trust’s project entities, with a smaller portion earmarked for general corporate purposes.

NHAI will also invest in the issue, subscribing to 15% of the total size as sponsor commitment. In addition, strategic investors such as EPFO and SBI Life Insurance Company have already committed ₹1,260 crore, giving the issue early institutional backing. That institutional backing supports credibility, but it should not be mistaken for a return guarantee. Retail investors still need to assess yield, leverage and traffic sensitivity independently.

Financial Snapshot

Because RIIT is newly constituted, investors do not have historical standalone financials to analyse. That makes projected cash flows useful, but also increases dependence on assumptions.

Revenue is projected to rise over the concession period, helped by expected traffic growth and periodic toll revisions. However, for retail investors, projected revenue is less important than how much of that cash ultimately becomes distributable after debt servicing and reserves.

The ~95% EBITDA margin reflects the operating model of mature toll roads, where variable costs are limited once the asset is built and operational. But investors should be careful not to confuse high EBITDA margins with equally high distributions, because debt servicing, maintenance and trust-level cash-flow waterfalls still matter.

The IPO proceeds of ₹6,000 crore flow into the special purpose vehicle (SPV), which uses them alongside external debt to pay NHAI ₹5,850 crore as concession consideration. The SPV will carry debt post-listing. Distributions will depend on revenues comfortably exceeding both operating costs and debt service.

Peer Comparison

India currently has six publicly listed road InvITs falling into two categories: power transmission InvIT and roads InvIT. Here's how RIIT stacks up against all of them on an operational scale.

RIIT starts with 5 toll assets across 4 states and about 260.2 km, while larger peers such as NHIT operate at much greater scale and others like Cube, Vertis, Interise and IRB InvIT have broader portfolios or mixed toll/HAM/annuity exposure. That means RIIT is smaller and more concentrated, but also cleaner and easier to underwrite as a pure toll-cash-flow platform. The trade-off is that you get clearer revenue drivers, but also more direct exposure to traffic risk than in more diversified peers.

Key Risks

- No binding agreements at filing: The concession agreements and financing arrangements for the SPV were not executed at the time of the RHP filing. Everything, asset transfer, SPV setup, toll collection hinges on these being signed. Any delay could disrupt timelines and projections.

- SEBI exemption unconfirmed: RIIT has applied for regulatory exemptions, including on combined financial statements. These may not be granted on time or at all which could delay the IPO or limit disclosure quality.

- Traffic is the only revenue driver: Toll collections can fall due to economic slowdowns, rising fuel prices, pandemic-type disruptions, or new bypass roads. The Jharkhand and Andhra Pradesh corridors are especially sensitive to freight and industrial cycles.

- Fixed 15 year life cycle: Assets revert to NHAI at concession end. There is no terminal value for unit holders. You're buying a time-limited income stream, plan your return expectations accordingly.

- Debt servicing pressure: The SPV carries external debt alongside IPO equity. If revenues disappoint or interest rates rise, distributions get squeezed before they reach you.

Regulatory and tax changes: InvIT rules are still evolving in India. Changes to toll policy, SEBI frameworks, or how distributions are taxed can alter your actual post-tax returns, sometimes significantly. - Sponsor concentration: NHAI retains meaningful voting influence post-IPO. If government priorities shift, say on future asset transfer pricing minority unit holders have limited recourse.

- Market liquidity risk: InvITs are still a niche product in India. Secondary market liquidity can be thin, and sentiment-driven selloffs can push unit prices well below NAV, especially in the early years before the product gains wider investor familiarity.

- Government dependency: Asset identification, regulatory clearances, concession transfers, all of it runs through government channels. Delays in approvals or shifts in political priorities can slow down everything from asset acquisition to distribution timelines.

Investor Takeaway

Raajmarg Infra Investment Trust should be viewed as a listed yield product backed by operating toll-road assets, not as a conventional IPO driven by earnings growth or listing-day excitement. At its core, the investment case rests on one question: how much cash can these roads distribute to unit holders, and how dependable will that cash be over time?

That makes RIIT very different from a typical equity IPO. You are not buying into a fast-scaling business with open-ended upside. You are buying exposure to a finite stream of toll collections from a relatively small portfolio of operational roads. If traffic growth, toll revisions and financing assumptions hold, investors could benefit from regular distributions and some gradual scale-up if additional assets are acquired sensibly. But if traffic disappoints or debt servicing becomes tighter than expected, the impact will show up first in distributions rather than in headline revenue.

There are three genuine positives here.

- First, the underlying assets are already operational, so this is not a construction-risk story.

- Second, the NHAI sponsorship gives the platform institutional credibility and potential access to future road assets.

- Third, the toll-road model can generate high operating margins, which creates the potential for healthy distributable cash flows if leverage remains under control.

But retail investors should not confuse those strengths with certainty. RIIT is still a traffic-linked, leveraged, time-bound yield vehicle. It does not offer fixed coupons like a bond, it does not have perpetual asset life, and it does not yet have an established public-market distribution history that investors can rely on. That means the issue should be judged not on narrative comfort, but on four hard variables: expected yield, debt burden, asset concentration and downside resilience under weaker traffic assumptions.

Compared with larger listed peers, RIIT is simpler but also more concentrated. That simplicity is a plus from an understanding standpoint, but it also means there is less diversification to cushion underperformance in any one corridor. For that reason, pricing matters. Retail investors should be asking whether the expected post-tax yield at the issue price is sufficiently attractive to compensate for concentration, limited life and execution risk.

The bottom line is that RIIT may suit you if you are looking for medium to long-term infrastructure-linked income and are willing to evaluate it with the discipline of a cash-flow investor..

FAQs

What is the Raajmarg Infra Investment Trust IPO?

Raajmarg Infra Investment Trust IPO is a mainboard InvIT public issue worth ₹6,000 crore. The issue is priced in the band of ₹99 to ₹100 per unit and is proposed to be listed on BSE and NSE.

When will the Raajmarg Infra Investment Trust IPO open?

The IPO will open for subscription on Wednesday, March 11, 2026, and will close on Friday, March 13, 2026.

What is the price band of the Raajmarg Infra Investment Trust IPO?

The price band for the Raajmarg Infra Investment Trust IPO is ₹99 to ₹100 per unit.The minimum bid size or lot size of the Raajmarg Infra Investment Trust IPO is 150 units.

What is the minimum investment required for the Raajmarg Infra Investment Trust IPO?

Based on the upper price band of ₹100 and the lot size of 150 units, the minimum investment required is ₹15,000.

When will I get Raajmarg Infra Investment Trust InvIT IPO shares in my account?

If you receive Raajmarg IPO subscription, the shares will be credited in your demat account on March 23, 2026. The shares will be listed on the NSE and BSE on March 24, 2026

When is the allotment date for the IPO?

The allotment date for the IPO is expected to be Wednesday, March 18, 2026.

Related Topics

Important IPO terms all investors should understand before investing

Meesho IPO Opens on 3Dec - Is this ₹5,421 crores IPO worth investing?

10 Things to Know About Sudeep Pharma IPO: Date, Price, GMP & Complete Review

Canara Robeco AMC IPO: Should You Apply for MF Giant’s Public Debut?

Smartworks Coworking Spaces Limited IPO: 10 Key Things to Know Before Investing

Travel Food Services Limited IPO: 10 Key Things to Know Before Investing

Ellenbarrie Industrial Gases Limited IPO: 10 Key Things to Know Before Investing

HDB Financial Services Limited IPO: 10 Key Things to Know Before Investing

Sambhv Steel Tubes Limited IPO: 10 Key Things to Know Before Investing

Indogulf Cropsciences Limited IPO: 10 Key Things to Know Before Investing

Prostarm Info Systems Limited IPO: 10 Key Things to Know Before Investing

Aegis Vopak Terminals Ltd IPO: 10 Key Things to Know Before Investing

Schloss Bangalore Limited IPO: 10 Key Things to Know Before Investing

Belrise Industries Limited IPO: 10 Key Things to Know Before Investing

Hexaware’s Billion Dollar Markets Hits in Bear Market: Should You Invest?