OnEMI Technology Solutions (Kissht) IPO - Should You Apply?

By

Arihant Team

India’s credit demand is expanding rapidly, especially among younger and underserved consumers, and digital lenders are stepping in to fill that gap. Kissht, operated by OnEMI Technology Solutions, is one such platform that has scaled quickly by offering app-based personal loans and credit products.

In This Article

- Introduction

- Key IPO Details: Kissht IPO

- Business Overview

- Where Will Kissht’s IPO Proceeds Go?

- Financial Performance

- OnEMI Technology Solutions Peer Comparison

- OnEMI Technology Solutions IPO Valuation

- Key Risks

- Final Verdict

- FAQs

Introduction

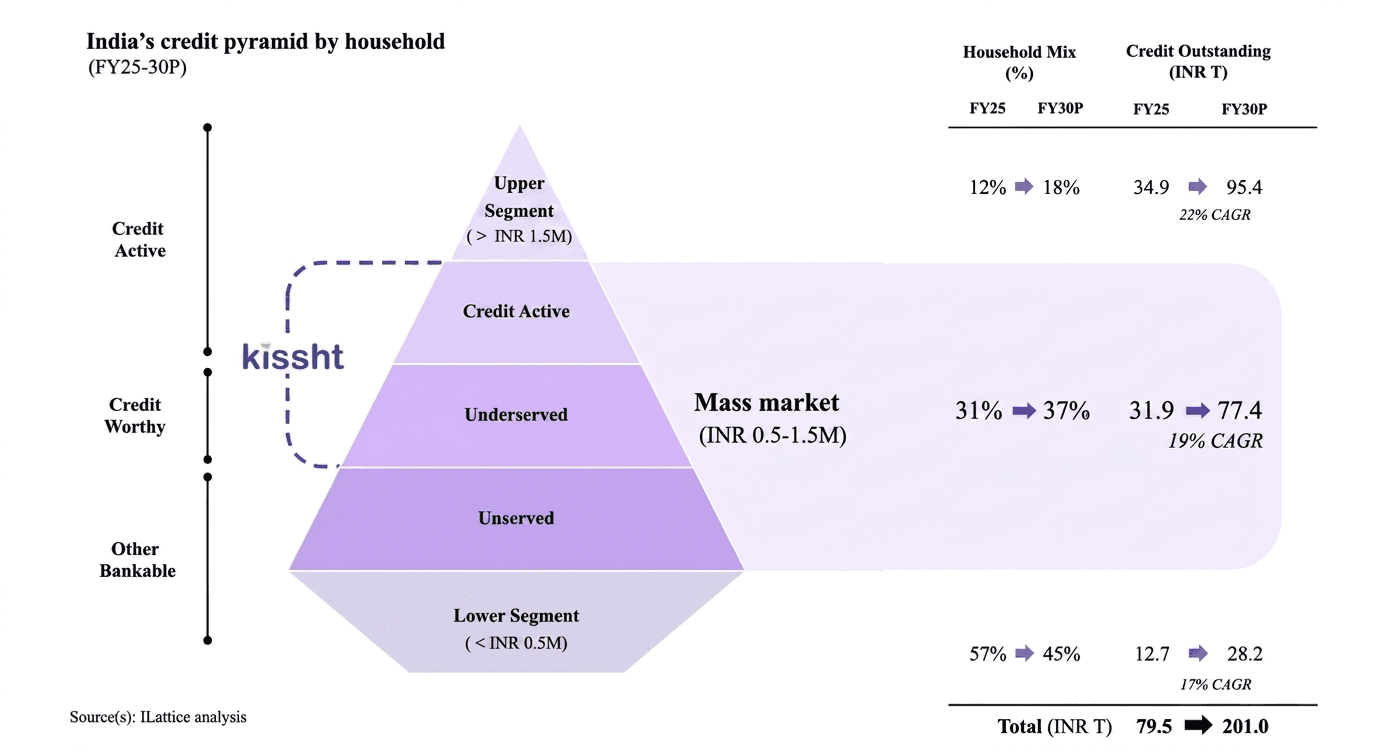

India is not short on demand for credit, but access to fast, small-ticket loans remains limited for a large section of the population. Traditional banks tend to focus on prime borrowers, leaving a significant gap in the mass-market segment.

This is where digital lending platforms like Kissht come into play.

Kissht operates at the intersection of technology and finance, offering quick, app-based loans backed by algorithm-driven underwriting.

Now, the company is coming to market with a ₹925.92 crores IPO comprising ₹850 crores in fresh issue and ₹0.44 crore in OFS.

The broader investment case is not just about a fintech company going public, but about whether a fast-scaling digital lender can sustain growth while managing credit risk in a highly regulated environment.

Let’s take a closer look!

Click here to apply:

Open a free account today

Invest in tomorrow with just one click

Key IPO Details: Kissht IPO

Here are the key details investors should know:

- Price Band: ₹162 to ₹171 per share

- IPO Dates: Thu, Apr 30, 2026 - Tue, May 5, 2026

- IPO Size: ₹925.92 crores

- Minimum Investment: ₹14,877 (87 shares: 1 lot size)

- IPO Type: Fresh Issue ( ₹850 crores) + Offer for Sale (0.44 crore)

- Listing Date: Fri, May 8, 2026

- Proposed Listing: BSE & NSE

- Promoter Holding: 24.8%

- Lead Manager: JM Financial Ltd.

Business Overview

Kissht is a technology-driven digital lending platform that offers personal loans and other credit products through a fully app-based interface. The company operates a hybrid model, where it manages customer acquisition, underwriting, and servicing in-house, while lending is conducted both on its own balance sheet and through partnerships with financial institutions.

Over a relatively short period, the company has built meaningful scale, with over 63 million registered users and more than 11 million customers served as of December 31, 2025. Its assets under management stood at approximately ₹59,557 million, comprising both on-book loans and off-book lending through partners.

The platform’s core differentiation lies in its technology-led underwriting and speed of execution. By leveraging a large set of data variables and machine learning models, Kissht enables rapid credit assessment, with many customers receiving loan offers within minutes. This has supported strong customer engagement and repeat usage.

AUM growth has been a key highlight, expanding significantly over the past few years, driven by both rising customer acquisition and increasing ticket sizes. While disbursements saw some moderation in FY25, this appears to be linked to a shift toward longer-tenure products rather than a decline in underlying demand.

The broader industry backdrop remains supportive, with increasing digital adoption and a large underserved credit market in India.

That brings us to the question, does Kissht have a lasting competitive edge? Not really. It operates in a crowded space, going up against several well-funded digital lenders like KreditBee, Navi Finserv, Fibe, and Moneyview. They’re all chasing the same underserved borrowers with similar products and tech-first approaches. There's little that meaningfully sets one apart from the other.

This means this space is competitive, with banks, NBFCs, and fintech players targeting similar segments, alongside rising regulatory oversight.

Where Will Kissht’s IPO Proceeds Go?

The issue is a combination of fresh issue of 4.97 crore shares aggregating to ₹850 crores and offer for sale of 0.44 crore shares aggregating to ₹75.92 crores.

The fresh issue proceeds will be utilised as follows:

The majority of the funds will be used to support the growth of the lending business by strengthening the capital base of its NBFC arm. This is essential for scaling assets under management. The remaining amount will be allocated toward general corporate purposes, within the defined limit. Overall, the utilisation reflects a focus on expanding lending capacity and strengthening the balance sheet.

Financial Performance

Now let’s examine Kissht’s financials:

Kissht’s total income declined from ₹1,700 crore in FY24 to ₹1,353 crore in FY25, reflecting a conscious moderation in disbursements rather than a slowdown in demand. The company appears to have slowed growth to stabilise its credit book following elevated impairments in FY24, where credit costs were significantly high. The recovery in 9M FY26 income to ₹1,584 crore, already exceeding the full-year FY25 level, indicates that growth has resumed.

EBITDA margins have expanded meaningfully, improving from 9.8% in FY23 to 21.1% in FY24 and further to 29.8% in FY25, reaching 30.8% in 9M FY26. This reflects clear operating leverage, where revenue growth has outpaced operating costs.

The cost-to-income ratio has also improved steadily, declining from 97.6% in FY23 to 83.2% in 9M FY26. While this remains higher than established peers like Bajaj Finance and Cholamandalam (typically in the 60-70% range), the direction of improvement is encouraging.

Operating cash flows were negative at ₹637 crore in FY24 and ₹661 crore in FY25. For an NBFC, this is not unusual, as loan disbursements are treated as operating outflows. This expansion has been supported by financing inflows, with cash flow from financing at ₹312 crore in FY24 and ₹542 crore in FY25, indicating reliance on borrowings to fund growth.

For an NBFC-led digital lender, the more important lens is not just revenue or PAT growth, but the quality of the loan book. Kissht’s AUM stood at around ₹5,956 crore as of December 2025, but over 90% of the book is unsecured, which makes credit discipline critical. Kissht’s PE stands at 17.9x and P/B 1.4x.

OnEMI Technology Solutions Peer Comparison

OnEMI Technology Solutions operates within the broader lending and fintech ecosystem, alongside players such as Bajaj Finance, Cholamandalam Investment, SBI Cards, HDB Financial Services, and newer digital lenders like Kissht.

Across the peer set, valuation reflects a combination of profitability and scale. OnEMI reports an ROE of 17.74% and is valued at around 17.9x P/E and 1.4x P/B, with a market capitalisation of approximately ₹926 crore.

In comparison, larger NBFCs such as Bajaj Finance and Cholamandalam operate at higher ROEs of around 19-20% and command premium valuations of 30-34x P/E and 5.5-6x P/B. Their significantly larger market capitalisation, exceeding ₹1 lakh crore, supports these higher multiples through scale, consistency, and established performance.

Mid-tier players like SBI Cards and HDB Financial Services, with ROEs in the range of 14-15%, trade at relatively moderate valuations, with P/E between 24–33x and P/B between 3.3-4.6x.

OnEMI Technology Solutions IPO Valuation

At first glance, Kissht's IPO valuation of 1.4x book value looks attractive. But there's an important catch.

Kissht lends to borrowers that traditional banks typically won't touch because of the risk involved. That's how it generates strong returns. But it also means higher risk of defaults, weaker loan quality, and a business that can get hit harder when the economy slows down.

Compare that to established NBFCs like Bajaj Finance or Cholamandalam, which trade at 4–6x book. Those valuations aren't just hype, they reflect years of proven performance across multiple economic cycles, consistent loan quality, and disciplined lending. Investors pay a premium because these companies have earned trust over time.

Kissht's growth story is compelling, but it hasn't yet been tested through a full credit cycle. Until it proves it can manage asset quality through both good times and bad, the discount to peers is justified, and the risk-reward may not be as attractive as the headline valuation suggests.

Key Risks

Despite its strengths, the business carries several important risks.

- Unsecured Lending Exposure: A large portion of the loan book is unsecured (~90%), which increases vulnerability to borrower defaults and limits recovery in stressed scenarios.

- Rising Asset Quality Stress: Gross NPAs have shown an upward trend, indicating growing pressure on credit quality as the business scales.

- Regulatory Risk: The digital lending space is closely regulated by the RBI, and any changes in norms around pricing, disclosures, or operations could impact growth and profitability.

- Dependence on External Funding: The business relies on continuous access to capital, both through its balance sheet and lending partners, to sustain growth.

- Credit Cycle Sensitivity: Performance is linked to economic conditions; any slowdown can lead to higher delinquencies and lower disbursements.

- Technology & Underwriting Risk: The model depends heavily on algorithm-driven credit assessment, where errors or model limitations can impact loan performance.

- Competitive Intensity: The company operates in a highly competitive space with banks, NBFCs, and fintech players targeting similar customer segments.

Final Verdict

Kissht represents a high-growth, profitable fintech company operating in a large and expanding market. Its scale, technology capabilities, and return metrics make it an attractive business on the surface.

However, the risks associated with unsecured lending, rising NPAs, and regulatory uncertainty cannot be overlooked. This is not a low-risk, steady compounder, but rather a business that could deliver strong returns if executed well, while also carrying downside risks if credit quality deteriorates.

For long-term investors who understand lending cycles and are comfortable with risk, the IPO could be worth considering, provided the valuation is reasonable. More conservative investors may prefer to wait and observe how the business performs post-listing before taking exposure.

FAQs

1. What are the IPO dates for Kissht (OnEMI Technology) IPO?

The IPO of OnEMI Technology Solutions Limited opens on April 30, 2026 and closes on May 5, 2026. The shares are proposed to be listed on the NSE and BSE.

2. What is Kissht IPO GMP?

Grey market activity reflects informal market sentiment toward the IPO. You can track the live GMP for the Kissht IPO through market sources here. However, GMP is unofficial, highly volatile, and should not be relied upon as a predictor of listing performance.

3. What is the lot size for retail investors?

The minimum lot size is 87 shares, which translates to a minimum investment of approximately ₹14,094 to ₹14,877 at the price band of ₹162 to ₹171 per share.

4. Is Kissht IPO a fresh issue or an OFS?

The IPO is a combination of a fresh issue and an Offer for Sale (OFS). The fresh issue (up to ₹850 crores) will be used primarily to strengthen the lending business by infusing capital into its NBFC subsidiary, Si Creva Capital Services, along with general corporate purposes. The OFS portion will go to existing shareholders.

5. Should I invest in the Kissht IPO?

Investors looking for exposure to the digital lending and fintech space may find the IPO interesting given the company’s growth, scale, and profitability. However, they should carefully consider risks such as high unsecured lending exposure, rising NPAs, regulatory oversight, and dependence on funding before making an investment decision.

Related Topics

Important IPO terms all investors should understand before investing

Meesho IPO Opens on 3Dec - Is this ₹5,421 crores IPO worth investing?

10 Things to Know About Sudeep Pharma IPO: Date, Price, GMP & Complete Review

Canara Robeco AMC IPO: Should You Apply for MF Giant’s Public Debut?

Smartworks Coworking Spaces Limited IPO: 10 Key Things to Know Before Investing

Travel Food Services Limited IPO: 10 Key Things to Know Before Investing

Ellenbarrie Industrial Gases Limited IPO: 10 Key Things to Know Before Investing

HDB Financial Services Limited IPO: 10 Key Things to Know Before Investing

Sambhv Steel Tubes Limited IPO: 10 Key Things to Know Before Investing

Indogulf Cropsciences Limited IPO: 10 Key Things to Know Before Investing

Prostarm Info Systems Limited IPO: 10 Key Things to Know Before Investing

Aegis Vopak Terminals Ltd IPO: 10 Key Things to Know Before Investing

Schloss Bangalore Limited IPO: 10 Key Things to Know Before Investing

Belrise Industries Limited IPO: 10 Key Things to Know Before Investing

Hexaware’s Billion Dollar Markets Hits in Bear Market: Should You Invest?