Wipro Q1 FY27 Results | 7 Key Takeaways Every Investor Should Know

Wipro's Q1 FY27 results reflect cautious near-term growth but continued focus on long-term expansion. Strong deal wins, AI investments, shareholder payouts, and a resilient pipeline remain the key highlights from the quarter.

In This Article

- Introduction

- Revenue guidance reflects cautious demand environment

- Margin recovery is expected to be gradual

- Large deal pipeline remains a key positive

- Technology & communication leads Wipro’s growth

- AI remains at the core of Wipro's strategy

- Wipro’s dividend focus

- Management guidance on growth recovery

- Investor takeaway

Introduction

Wipro's latest quarterly update reinforces a trend investors have been watching for several quarters.

It delivered modest year-on-year growth, maintained a healthy large deal pipeline and continued to expand its AI capabilities. However, cautious enterprise spending and slower decision-making continued to weigh on revenue growth and profitability.

While the quarter provides a snapshot of where the business stands today, management's commentary also offers important clues about what investors can expect over the coming quarters.

Here's a breakdown of Wipro's Q1 performance and the key trends likely to shape FY27.

Revenue guidance reflects cautious demand environment

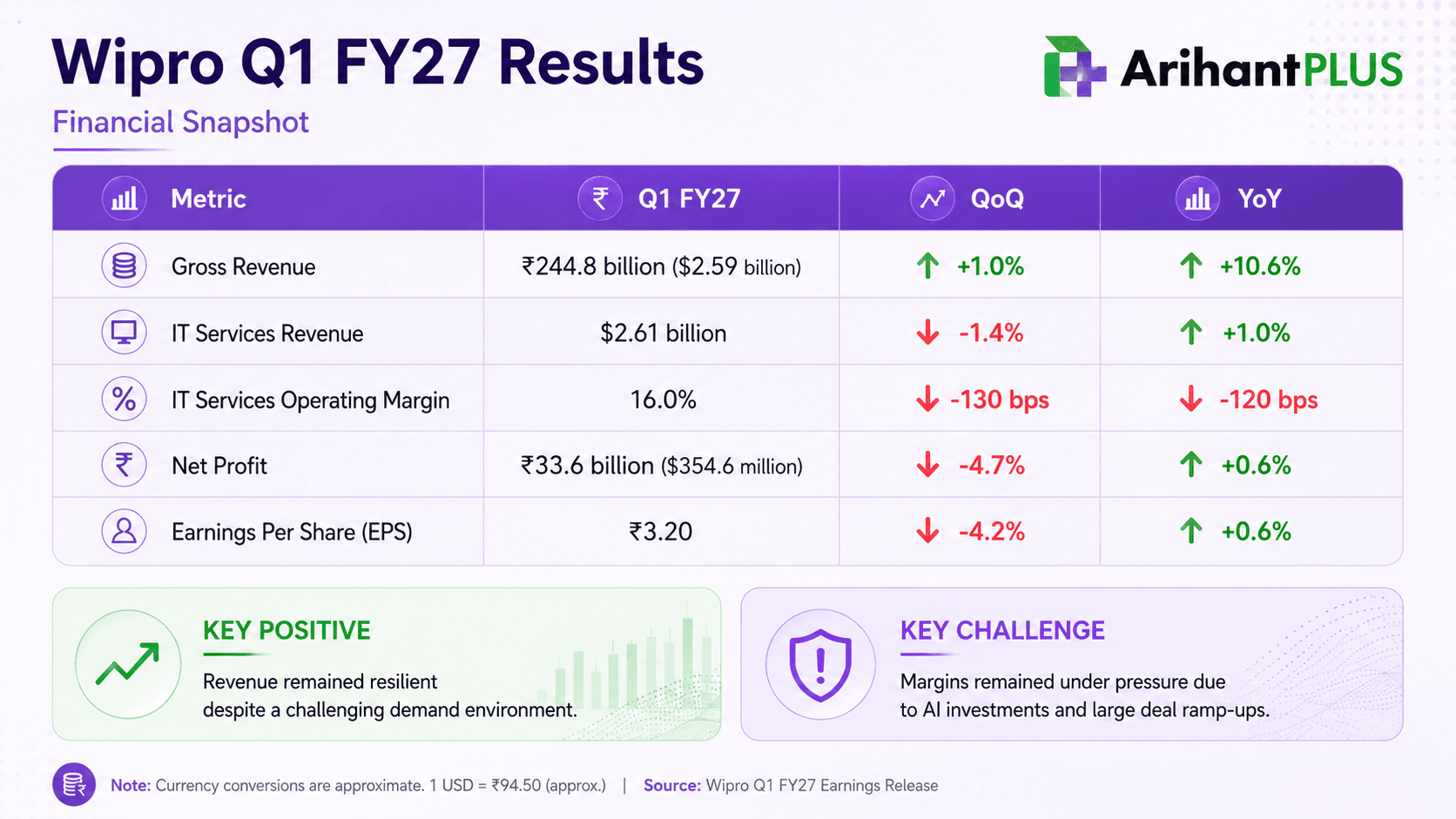

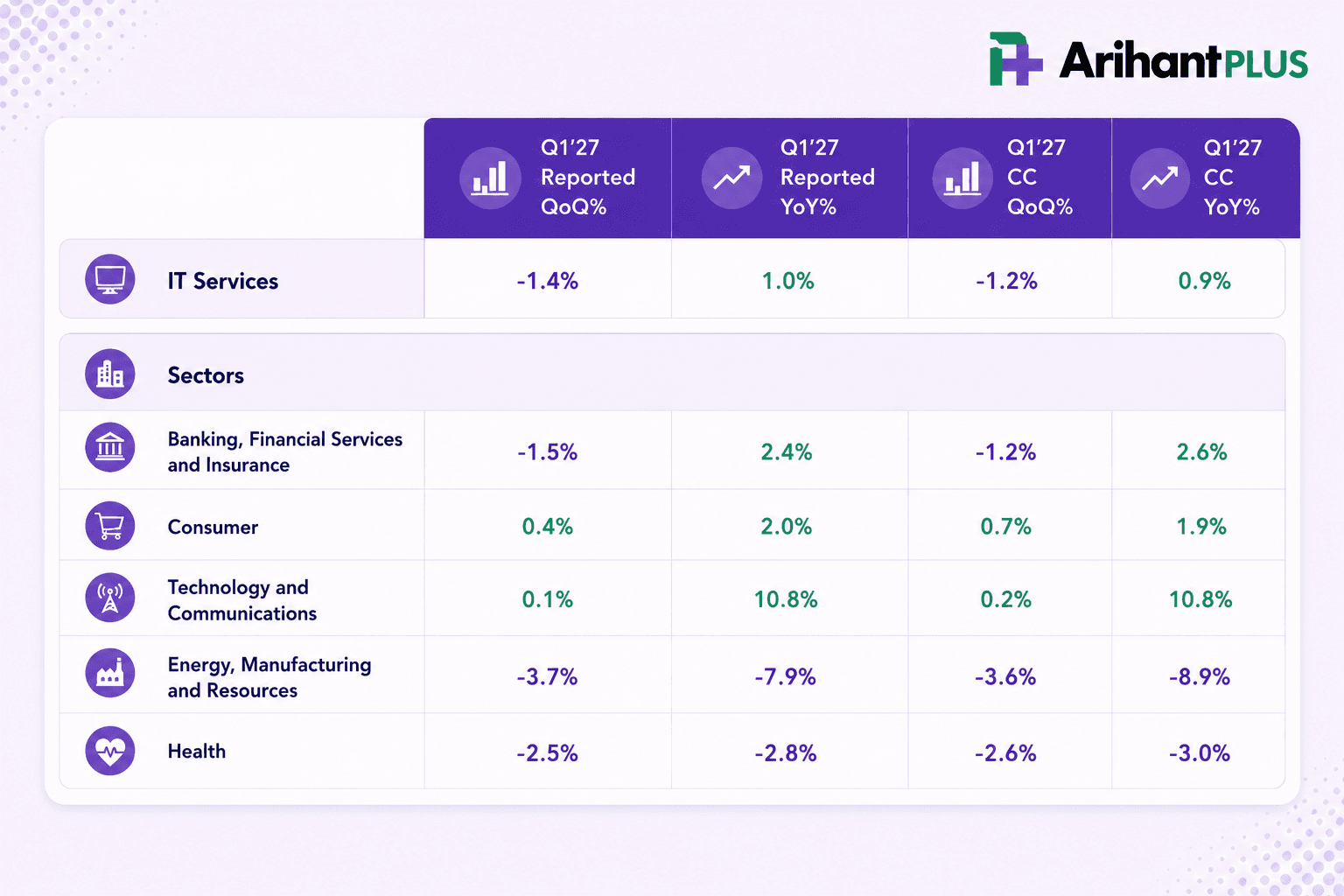

Wipro's revenue performance suggests demand remains uneven. IT Services revenue grew 0.9% year-on-year in constant currency, but declined 1.2% sequentially, indicating that enterprise spending has yet to recover meaningfully.

For Q2 FY27, Wipro expects IT Services revenue between USD 2.574 billion and USD 2.627 billion, implying constant currency sequential growth of -1.5% to +0.5%. The guidance suggests clients continue to delay discretionary spending and take longer to finalize projects.

Management's confidence, however, is tied to execution rather than a demand recovery. The company expects growth to improve as recently won large transformation deals begin contributing to revenue over the coming quarters.

Margin recovery is expected to be gradual

While Wipro expects operating margins to gradually improve to the 17% to 17.5% range over time, profitability remained under pressure in Q1 FY27. The IT Services operating margin came in at 16%, down 120 basis points year on year, as annual salary hikes, the ramp-up of previously won large deals and continued AI investments weighed on margins.

Management believes these investments are necessary to capture the next wave of AI-led demand. Alongside its AI-native Business & Platforms unit, Wipro is investing through its USD 500 million Wipro Ventures fund and Innovation Network to build new AI capabilities, even if it limits near-term margin expansion.

Large deal pipeline remains a key positive

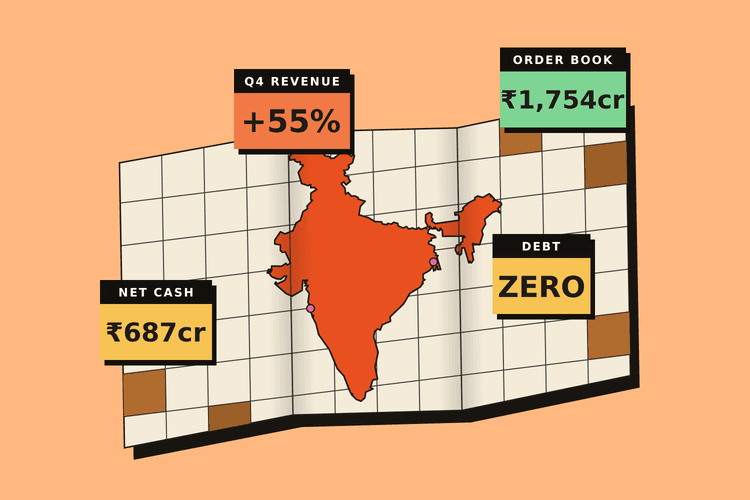

Despite a cautious demand environment, Wipro's deal momentum remained resilient during the quarter. The company reported total order bookings of USD 3.4 billion, including USD 1.6 billion in large deal bookings across 13 large deals, highlighting continued enterprise demand for cost optimisation and AI-led transformation.

Among the notable wins were a deal with a leading global animal healthcare provider to modernise digital operations across its hospitals and clinics using Wipro Intelligence, and another with a leading European specialty chemicals company to transform its application landscape using the WINGS platform, improving automation, delivery efficiency and operating costs.

Technology & communication leads Wipro’s growth

Technology & Communications continued to be Wipro's strongest vertical, growing 10.8% YoY (CC), while BFSI remained resilient with 2.6% YoY (CC) growth despite a softer sequential performance. Consumer also posted modest growth during the quarter.

On the other hand, energy, manufacturing & resources and health remained weak, reflecting continued softness in client spending. Management expects the energy, manufacturing & resources business to improve as recent deal wins move into execution, while a broader recovery in Healthcare will depend on higher discretionary spending and greater adoption of AI-led automation.

AI remains at the core of Wipro's strategy

AI dominated Wipro's Q1 FY27 earnings call, with management mentioning it 154 times, underscoring its role in the company's growth strategy.

Since launching its AI-native Business and Platforms unit last quarter, Wipro has moved from strategy to execution by building AI-powered industry platforms, expanding ecosystem partnerships and developing AI-native business models. The company also launched an Applied AI Centre of Excellence for Anthropic's Claude models to help clients adopt frontier AI with enterprise-grade governance.

The momentum is reflected in external recognition as well. Capco won the AI Governance and Risk Excellence Award at the OpenAI Partner Summit, while Wipro's UK AI Lab won the OpenAI Codex Hackathon for an AI-powered banking solution.

Management believes the focus is shifting from technology modernisation to AI-enabled operating models that improve productivity, resilience and operational efficiency, positioning AI as a key long-term growth driver.

Wipro’s dividend focus

Alongside its investment strategy, Wipro continues to maintain a strong focus on returning capital to shareholders. The board declared an interim dividend of ₹2 per share, with a record date of 27 July and payment on or before 14 August.

Wipro also completed a USD 1.56 billion buyback during the period, retiring 600 million shares. Together with the dividend, total shareholder payouts over the past year are expected to exceed USD 3 billion.

Cash generation supported these returns: operating cash flow was ₹3,288 crore, converting roughly 98% of net income into cash.

Management guidance on growth recovery

Wipro expects the demand environment to remain challenging in the near term as enterprises continue to take a cautious approach to technology spending. Longer decision cycles, macroeconomic uncertainty and weak discretionary spending are likely to keep growth under pressure.

That said, management expects a gradual recovery as recently won large deals move into execution and AI-led transformation spending continues to gain traction.

Investor takeaway

While investors may have to wait for these initiatives to translate into stronger revenue growth, Wipro's disciplined capital allocation remains intact. The company has announced an interim dividend of ₹2 per share, with total shareholder payouts over the past year expected to exceed USD 3 billion, reflecting strong cash generation and a continued commitment to returning capital.

Wipro's Q1 FY27 update doesn't change the broader investment narrative. Growth is likely to remain under pressure in the near term, but the company continues to strengthen the building blocks for a gradual recovery through AI investments, a healthy large deal pipeline and operational improvements.

Related Topics

Ethical Investing Gets Real: NSE and BSE Launch Saatvik and Ahimsa Indices

Can REITs and InvITs Become India’s Next Retail Portfolio Essential?

Everyone Knows Bajaj Finance’s Playbook. So Why Can’t Anyone Copy It?

Beyond the Dark Store: Is Advertising Zepto's Real Business?

Vedanta Demerger: Why Aluminium Became the Market’s Favourite/Darling

NSE Extends F&O Market Close to 3:40 PM: What Traders Must Know

Elon Musk’s $119 Billion Terafab Bet: Can It Reshape AI Chips?

Rupee Crashes to ₹96: How Investors Can Profit From the Fall

The Rise of India’s Defence Sector: Stocks, Trends & Opportunities

SEBI introduces Verified Badge for Trading Apps to Curb Fake App Scams

TCS Q4 Concall: AI Infrastructure to Drive the Next Growth Cycle

Rupee Slips Past 95/USD | Factors Driving the Fall Despite RBI Intervention

The Popcorn Trade: How Dhurandhar 2 is driving PVR INOX Stock Higher

Oil Is Surging After The Iran Strikes. So Why Isn’t Gold Following?

What’s Getting Cheaper & Costlier in Budget 2026: A Simple Money Guide

Union Budget Day & Market Behaviour: 15 Year Trend Analysis (2011-2025)

Maruti Q3FY26 Profit Up 4%: Losing Grip on India’s Car Market?

New Year, New Financial Goals: Make SIP Your 2026 Resolution

Infosys ₹18,000 Crore Share Buyback: Record Date & Why Promoters Opted Out?

Nifty 50 Performance Since Last Muhurat Trading: Nifty Top 10 Performers

Diwali Muhurat Trading: Can Nifty’s 7-Year Winning Streak Continue?

Tata Motors Demerger Gets NCLT Nod: What Shareholders Must Know

Muhurat Trading 2025 on 21 Oct: Everything You Should Know

Tuesday is the New Thursday: NSE & BSE Expiry Shift from Sep 2025

How Jane Street Snatched ₹36,500 Crore While India's Youth Lost Everything

Axis Bank Q1FY26 Results: A Mixed Bag, but Long-Term Picture Still Intact

Indian Stock Market Outlook: What Happened And Way Forward