In This Article

- Introduction

- Inside C.E. Info Systems Business Model

- 5 Reasons That Make MapMyIndia A Value Stock?

- Making Sense of Financial Year 2026 numbers

- Risks

- Investor Takeaway

Introduction

MapmyIndia's shares climbed nearly 15 percent today. The company, listed as C.E. Info Systems caught investors' attention after what looked like just another sharp move in the market.

Why did the stock soar? Did the company announce something significant, or was the market simply looking past its weak FY26 numbers?

After going through the financials and management commentary, we realized the story was more nuanced than the headline results suggested.

Whether today's rally is justified remains to be seen, but we do think the business deserves a closer look.

Open a free account today

Invest in tomorrow with just one click

Inside C.E. Info Systems Business Model

Now, most people know MapmyIndia as India's homegrown alternative to Google Maps.

That comparison is understandable, but it captures only a small part of what the company actually does.

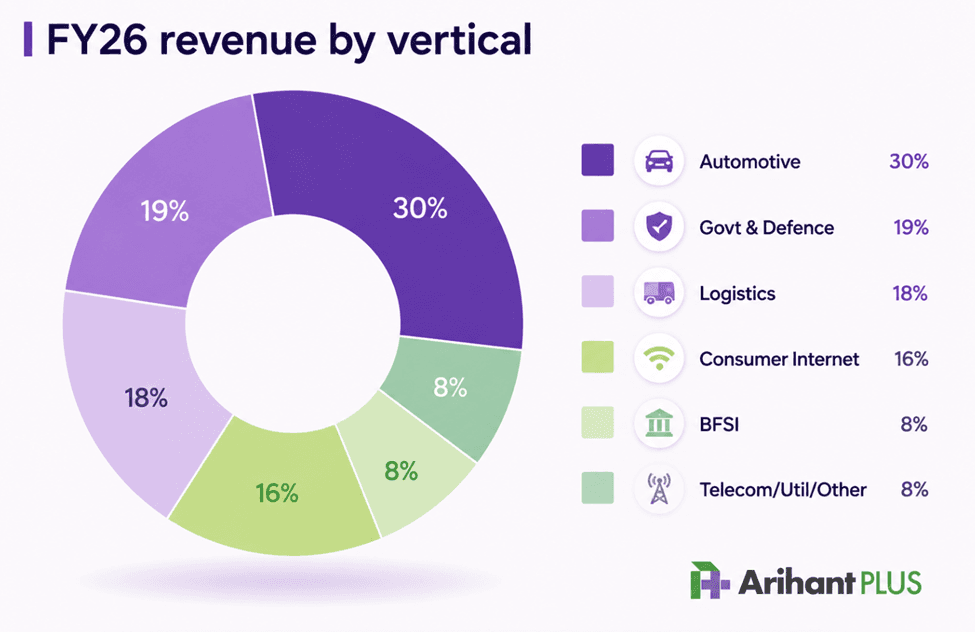

Over the past three decades, MapmyIndia has built one of India's largest proprietary digital mapping databases. Today, its technology supports businesses across a wide range of industries, including automobiles, logistics, banking, ecommerce, government, and defence.

The company generates revenue through three core businesses.

- Mapping and Location Intelligence: This is the company's largest business. Enterprises pay MapmyIndia for digital maps, navigation software, APIs, and location intelligence solutions that power everything from in-car navigation to address verification and route optimization.

- Internet of Things and Fleet Management: MapmyIndia also provides GPS tracking devices and telematics software for commercial vehicles. While the hardware helps acquire customers, recurring software subscriptions generate long term revenue. One of its largest deployments is a five year project covering nearly 23,000 LPG tankers for Indian Oil.

- Mappls Consumer App: The Mappls app has crossed 45 million downloads. Although it contributes little revenue today, every user helps improve the company's maps by sharing real time traffic and road data, creating a feedback loop that strengthens the platform over time.

5 Reasons That Make MapMyIndia A Value Stock?

We dug deeper to understand why many long term investors have not written off the company despite its disappointing FY26 performance. Here are the five factors that stood out the most.

1. Competitive Edge: Building a high quality digital mapping platform takes years of surveying, constant updates, and massive amounts of location data. After nearly three decades of investment, MapmyIndia has built an asset that would be difficult and expensive for competitors to replicate.

2. Revenue Quality: A large share of the company's revenue comes from recurring subscriptions rather than one time sales. Mapping services, licensing fees, and fleet management software provide predictable cash flows that should grow alongside its customer base.

3. Positive Guidance: Management says around ₹47 crore of expected revenue shifted into FY27 because several government and automotive projects were delayed rather than cancelled. If that plays out as expected, FY26 could prove to be a timing issue instead of a demand problem.

4. Multiple Growth Drivers: MapmyIndia serves customers across automobiles, logistics, banking, government, defence, ecommerce, and consumer internet. That diversified customer base reduces dependence on any single industry while creating multiple avenues for future growth.

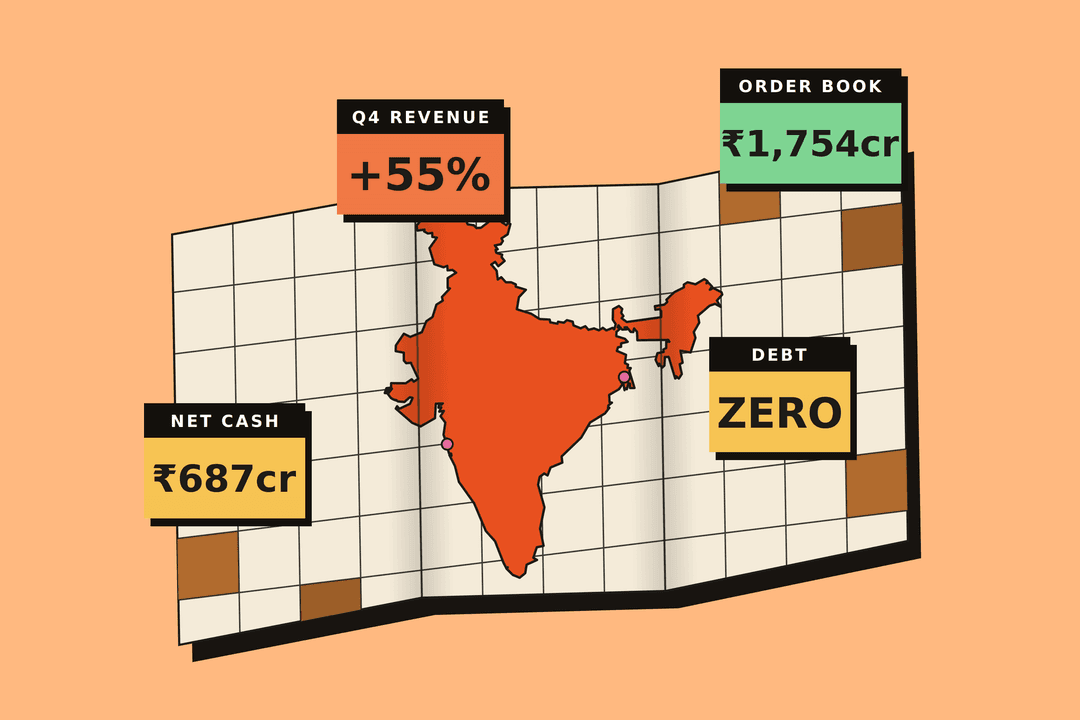

5. Strong Balance Sheet: MapmyIndia has zero debt, nearly ₹687 crore in net cash, and consistently generates free cash flow. With founders still owning around 51% of the company, management remains well aligned with long term shareholders.

Making Sense of Financial Year 2026 numbers

If you looked only at the headline numbers, it would be easy to conclude that MapmyIndia's growth story had lost momentum.

FY26 revenue grew by just 2% to around ₹474 crore, while EBITDA margin moderated to roughly 37%. Unsurprisingly, the market reacted negatively.

However, management attributes the slowdown largely to execution delays rather than weaker demand. According to the company, nearly ₹47 crore of expected revenue shifted into FY27 after several government and automotive projects were postponed instead of cancelled.

The fourth quarter lends some support to that explanation. Revenue rose nearly 55% sequentially, EBITDA increased 141%, and the order book expanded to roughly ₹1,754 crore, suggesting the demand pipeline remains healthy.

Map-led (INR cr)

IoT-led

That said, one strong quarter is not enough to call it a turnaround.

The real test will be the Q1 FY27 results, which should indicate whether delayed projects are finally translating into revenue and whether the company's growth is beginning to recover.

Risks

Every business has some risks, which as a smart investor you should consider. Here are key risks for MapMyIndia:

- Execution Risk: Government projects do not always move according to schedule. Even if demand remains strong, delays between winning a contract and recognizing revenue can lead to weak quarterly numbers and increased volatility in the stock.

- Auto Exposure: Automotive industry remains an important revenue driver for MapmyIndia. If vehicle production slows meaningfully, demand for its navigation and software solutions could also soften for a period.

- Competitive Pressure: MapmyIndia has built a strong domestic mapping platform, but competition is unlikely to ease. Global technology companies continue investing heavily in digital maps and location intelligence, making continuous product innovation essential.

- Valuation Risk: The stock has historically traded at a premium because investors view it as a high quality business. That premium leaves little room for disappointment, which means even small misses on growth expectations can trigger sharp corrections.

Investor Takeaway

MapmyIndia still possesses many of the qualities that investors typically look for in a long term compounder. It operates in a niche with high barriers to entry, generates a meaningful amount of recurring revenue, maintains a debt free balance sheet, and continues to be led by founders who own a significant stake in the company.

At the same time, today's ~13% rally does not change the investment case overnight.

Disclaimer: This article is for educational and informational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. The securities mentioned are exemplary and not recommendatory. The author, research analyst, or Arihant Capital Markets Ltd. and its associates may hold positions in the securities discussed. Investments in the securities market are subject to market risks; read all the related documents carefully before investing. Please consult your financial advisor before making any investment decisions.

RA: Abhishek Jain

Related Topics

Wipro Announces Record Date 5June for ₹15k Cr Buyback: Opportunity or Growth?

Maruti’s Q4FY26 Profit Drops but Growth Outlook Remains Strong: Should you buy?

Trent announces 1:2 bonus; record date May 29, posts strong Q4FY26 results