Rupee Crashes to ₹96: How Investors Can Profit From the Fall

By

Arihant Team

The Indian rupee has hit an all-time low of ₹96.90 against the US dollar, down 7.8% in 2026 alone. Most investors treat this as macro noise. It isn't. Currency depreciation quietly erodes returns, reshuffles sector leadership, and demands a deliberate portfolio response. Smart investors take action to make the depreciating rupee in their favour.

In This Article

- Key Takeaways

- Introduction

- Why the rupee is falling & why this isn't a temporary dip

- The invisible hit on your investments

- What 2018 taught us

- 2018 vs. 2026: The Pattern looks familiar

- 3 ways to respond

- What you can actually do right now

- Conclusion

Key Takeaways

- A weakening rupee impacts wallet and portfolio of every Indian. Smart investors need to take the right action to safeguard their money and take strategic bets.

- Investors may profit from a falling rupee by owning international ETFs (dollar-based) or investing in Indian exporting companies.

- Weakening rupee can benefit exporters, making their goods cheaper for international buyers.

- Oil marketing companies (OMCs), airlines, and import-dependent FMCG face the sharpest pain. A double squeeze of dollar costs and rupee revenues is a structural headwind, not a short-term dip to buy.

- A weak rupee can signal economic downturns, rising inflation, or both, impacting investments.

- Every major rupee cycle since 2013 has rewarded diversification over reaction. Adding gilt funds to your portfolio and adding a layer of diversification is a good idea.

Introduction

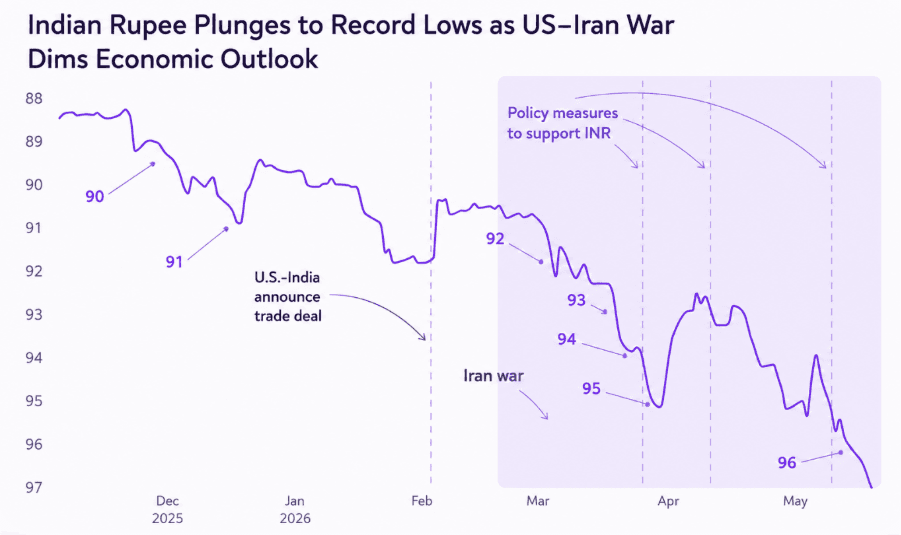

The Indian rupee crashed to an all-time low of ₹96.96 per against the US dollar this week due to rising crude oil prices and mixed global cues driving the sentiment of investors.

₹96.90 Rupee all-time low | –7.8% Rupee fall in 2026 YTD | $110 Brent crude per barrel |

Some of us shrugged this as just a headline meant for bankers or exporters. But a weaker rupee impacts us all - it quietly drains our savings, raises grocery bills, makes our gadgets and electronics expensive and inflates fuel costs. And..... it has a huge impact on our portfolio too!

Source: Reuters

Why the rupee is falling & why this isn't a temporary dip

Three structural forces are at work simultaneously, and none has a near-term resolution. India imports over 85% of its crude oil in dollars. With Brent crude price reaching $110 per barrel and Strait of Hormuz disruptions raising shipping and insurance costs, refiners are buying dollars at a relentless pace, widening the trade deficit. India's trade gap reached $28.4 billion in April 2026, up from $20.67 billion in March alone.

At the same time, foreign portfolio investors (FPIs) have pulled over $22 billion out of Indian equities and bonds since February 2026, a pace that already exceeds all of last year's outflows. Each exit sells rupees to buy dollars. And with the US Federal Reserve holding rates elevated and signalling no cuts, dollar assets continue to offer better risk-adjusted returns than emerging markets, keeping that outflow pressure alive.

The Reserve Bank of India has intervened by selling dollars to slow the fall. However, its reserves have declined roughly $37 billion from peak levels, limiting how long and how hard it can defend the currency. The rupee is not correcting toward a floor. It is adjusting to a new structural reality, and investors who treat it as a temporary blip are making an expensive assumption.

Open a free account today

Invest in tomorrow with just one click

The invisible hit on your investments

Every time the Indian rupee falls, the stock market takes a hit. Not just that, even the real value of your money erodes.

Here is the arithmetic. Say your mutual fund returned 12% last year – good! But if the rupee weakened 5% against the dollar in the same period, your real purchasing power, measured against the world, only grew by about 7%. The rest quietly evaporated - no alert, no statement entry. Investors call this the "invisible loss."

Beyond your portfolio, a weaker rupee means higher fuel prices (India imports most of its crude in dollars), pricier imported electronics, and more expensive foreign travel or education. This impacts a lot of companies, their profitability and consequently their stock prices, which impacts your portfolio too!

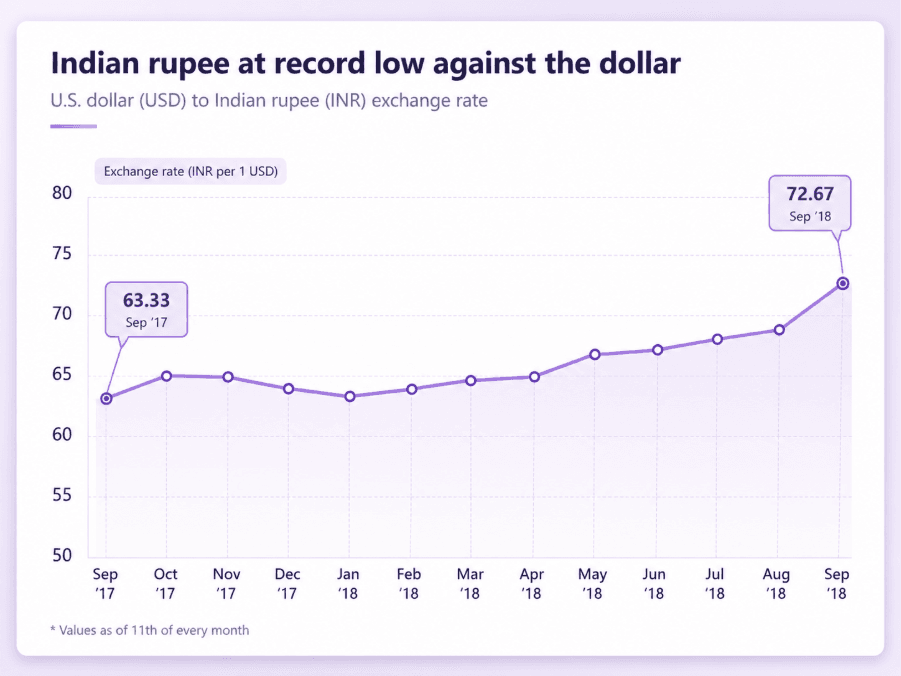

What 2018 taught us

The last major rupee crisis ran from January to October 2018, when the rupee fell nearly 17% - from ₹63.5 to ₹74.5 per dollar. The culprits were rising US interest rates, elevated crude prices, and a widening trade deficit. Sound familiar? The same forces are at work today.

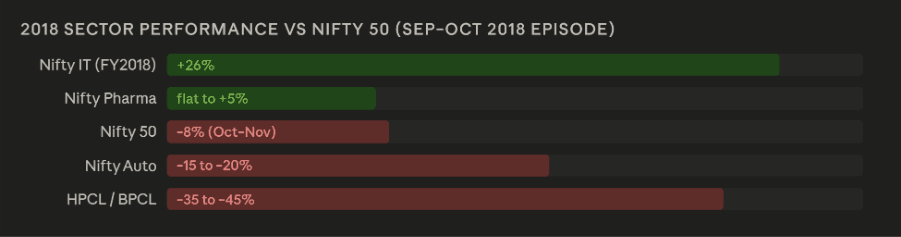

What made 2018 instructive wasn't the fall itself, it was how differently sectors responded.

History has shown that currency depreciation does not hit every sector equally. It creates a sharp and predictable divide between companies that earn in foreign currencies and those that depend on imported inputs. The performance gap between the two groups during rupee stress episodes has been consistently large.

Sectors that benefit | Sectors that suffer |

IT Services ~90% revenue in USD, costs in INR. TCS reported 3.7% INR growth vs 0.6% USD growth in one quarter, the gap is pure currency gain. Infosys attributed 60 bps of recent margin improvement directly to the rupee. In 2018 also, Nifty IT rose ~26% while the broader Nifty 50 went nowhere. | Oil marketing companies Dollar crude costs rise while retail prices are politically capped. HPCL and BPCL face the sharpest structural squeeze in this environment — historically, their worst episodes. |

Pharma exporters 50–60% revenue from exports. Weaker rupee lifts realisations and makes Indian generics more price-competitive in the US and EU markets. | Airlines & Auto Companies Fuel in dollars, leases in dollars, revenue in rupees. A 7.8% rupee fall can eliminate an entire year's profitability for a mid-size carrier. Auto companies depend on imported components. A weaker rupee meant higher costs and squeezed margins. In 2018, Tata Motors fell nearly 60%. |

Textiles & specialty chemicals Dollar revenues against fixed rupee costs. Margin expansion is immediate and mechanical. | FMCG & import-heavy auto Imported inputs (palm oil, crude derivatives, components) cost more. Margins squeezed; pricing power limited by slowing consumer demand from inflation. |

Same market, same crisis but completely different outcomes based on where you were positioned.

2018 vs. 2026: The Pattern looks familiar

Same market, same dynamics, but with one difference: you now have the 2018 roadmap in front of you before the episode fully plays out. The question is whether you use it.

Factor | 2018 | 2026 |

US interest rates | Rising sharply (Fed hiking cycle) | Elevated, no cuts in sight; rate hike risk returning |

Crude oil | Surging, ~$85/barrel peak | ~$110/barrel; Strait of Hormuz disruptions |

Rupee move | -17% over 9 months (₹63.5 → ₹74.5) | -7.8% in 3 months (₹87 → ₹96.90) and falling |

FII outflows | Significant but contained | $22B+ since Feb 2026 — a decade-high pace |

Sector winners | IT, pharma, specialty chemicals | Same playbook in motion |

Sector losers | Auto, OMCs, real estate | Same headwinds, possibly worse |

3 ways to respond

There is a well-established multi-asset framework used by global investors whenever there is a currency fall, expressed across equities, commodities, bonds, and international exposure, rather than relying on a single bet. Here is how that framework translates directly to Indian investors right now.

- Add exposure to export-driven sectors

IT and pharma are the most direct beneficiaries of a weaker rupee. If your portfolio leans heavily on domestic sectors like banking or real estate, consider gradually redirecting new SIPs toward Nifty IT ETFs, pharma mutual funds, or sector index funds. No need to overhaul everything - even a small tilt makes a difference.

- Add some international exposure

Here's a simple example: ₹10,000 invested in an international index fund in January 2022 (at ₹74.5/dollar) would have grown to roughly ₹11,700 by early 2025, just from the currency move, even with zero market returns. International index funds let you own global companies like Apple and Microsoft in plain rupees, through regular platforms, fully regulated by SEBI.

A well-diversified portfolio, as a thumb rule, should have 5–15% of money parked in international equities. It's not a bet against India, it’s just simple diversification rule so you are safeguarded from currency risks.

- Look at gilt funds as a defensive cushion

Gilt funds invest in government bonds, you're essentially lending to the Government of India, which means near-zero credit risk. The interesting part: when the rupee weakens and growth slows, the RBI tends to cut rates.

When rates fall, bond prices rise, and gilt fund NAVs go up. This counter-cyclical quality makes them a useful buffer when equities are under pressure. Best suited for a 2–3-year horizon.

Here’s a snapshot of how investors should counter weakening rupee:

ASSet class | Why it works in a weak rupee environment | Indian instrument | Allocation |

Export companies shares | Earn in USD, spend in INR - mechanical margin expansion | Nifty IT ETF, pharma mutual funds, textile companies | Core |

Gold | Priced globally in USD. Every 1% rupee fall = ~1% INR gold price rise. | Gold ETF | 10–15% |

International equities | Dollar-denominated returns convert to more rupees as the currency weakens, a structural tailwind even with flat market performance | International funds like S&P 500 / Nasdaq FoF (SEBI-regulated, no LRS paperwork), Motilal Oswal Nasdaq 100 ETF & Mirae Asset S&P 500 Top 50 ETF | 5–15% |

Gilt funds | Counter-cyclical: when currency stress slows growth, RBI eventually cuts rates — bond prices rise, gilt NAVs go up. Zero credit risk. | SBI Magnum Gilt, ICICI Prudential Gilt, Nippon India Gilt Securities | Debt buffer |

Commodities (selective) | Dollar-priced commodities rise in INR terms. ONGC gains ~₹6,180 crore per $1 crude rise. Upstream oil benefits vs OMC pain. | ONGC for upstream exposure; commodity mutual funds for broader access | Tactical |

What you can actually do right now

You don't need to act on all three this week. Here's a measured, sequenced approach:

- Check your sector mix — if you're heavily weighted in banking, real estate, or domestic FMCG, plan a gradual shift. Add IT or pharma exposure via index ETFs as new money comes in.

- Check your international allocation — if you don’t have any international exposure, start with 5–10% allocation, it will act as a buffer against sustained rupee weakness. You can invest in SEBI-regulated funds of funds tracking the S&P 500 or Nasdaq.

- Review your debt allocation — consider if gilt funds fit your medium-term goals as a counter-cyclical anchor alongside your equity holdings.

- Move gradually, not in a lump sum — spread any rebalancing over 3–6 months via SIPs. Currency cycles are hard to time precisely; cost-averaging is your friend.

- Avoid panic-selling broad index funds — as 2018 showed, the Nifty 50 itself wasn't catastrophic. The damage was concentrated in specific sectors. Rotation beats exit.

Conclusion

Rupee weakness is cyclical, not permanent. It happened in 2013, 2018, and 2022 — and each time, investors who stayed diversified and disciplined came through stronger. The ₹96 level isn't a reason to panic. It's a prompt to check whether your portfolio is built for the world as it actually is.

Export sectors, international funds, and gilt funds aren't complicated strategies. They're practical tools, and now is a reasonable time to consider them.

Related Topics

Can REITs and InvITs Become India’s Next Retail Portfolio Essential?

Everyone Knows Bajaj Finance’s Playbook. So Why Can’t Anyone Copy It?

Beyond the Dark Store: Is Advertising Zepto's Real Business?

Vedanta Demerger: Why Aluminium Became the Market’s Favourite/Darling

NSE Extends F&O Market Close to 3:40 PM: What Traders Must Know

Elon Musk’s $119 Billion Terafab Bet: Can It Reshape AI Chips?

The Rise of India’s Defence Sector: Stocks, Trends & Opportunities

SEBI introduces Verified Badge for Trading Apps to Curb Fake App Scams

TCS Q4 Concall: AI Infrastructure to Drive the Next Growth Cycle

Rupee Slips Past 95/USD | Factors Driving the Fall Despite RBI Intervention

The Popcorn Trade: How Dhurandhar 2 is driving PVR INOX Stock Higher

Oil Is Surging After The Iran Strikes. So Why Isn’t Gold Following?

What’s Getting Cheaper & Costlier in Budget 2026: A Simple Money Guide

Union Budget Day & Market Behaviour: 15 Year Trend Analysis (2011-2025)

Maruti Q3FY26 Profit Up 4%: Losing Grip on India’s Car Market?

New Year, New Financial Goals: Make SIP Your 2026 Resolution

Infosys ₹18,000 Crore Share Buyback: Record Date & Why Promoters Opted Out?

Nifty 50 Performance Since Last Muhurat Trading: Nifty Top 10 Performers

Diwali Muhurat Trading: Can Nifty’s 7-Year Winning Streak Continue?

Tata Motors Demerger Gets NCLT Nod: What Shareholders Must Know

Muhurat Trading 2025 on 21 Oct: Everything You Should Know

Tuesday is the New Thursday: NSE & BSE Expiry Shift from Sep 2025

How Jane Street Snatched ₹36,500 Crore While India's Youth Lost Everything

Axis Bank Q1FY26 Results: A Mixed Bag, but Long-Term Picture Still Intact

Indian Stock Market Outlook: What Happened And Way Forward