TCS Q4 Concall: AI Infrastructure to Drive the Next Growth Cycle

By

Arihant Team

Tata Consultancy Services reported a muted quarter at first glance, but there is more taking shape beneath the surface. There are early signs of demand stabilising, and a quieter shift towards AI-led spending that could matter more than the headline numbers.

In This Article

- Introduction

- From Experimentation to Execution: AI Infrastructure

- TCS Q4 Concall: Sector Tailwinds & Margin Pressure

- Investor Takeaway

Introduction

TCS just reported its Q4 numbers, and at first glance, there isn’t much to get excited about.

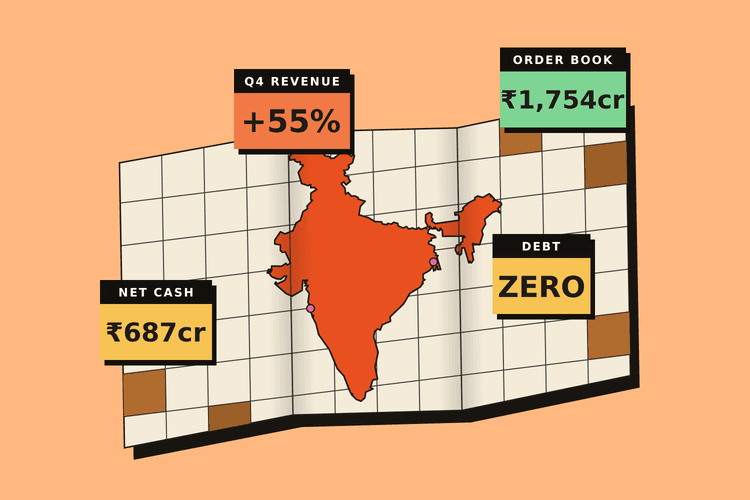

Revenue grew 1.2% QoQ in constant currency, while margins remained flat at 25.3%. On the surface, this looks like a fairly uneventful quarter.

But have you stopped to wonder that maybe this quarter isn’t really about growth.. It's about things not getting worse.

Management commentary clearly points to early signs of stabilisation in large and mid-sized accounts, which typically marks the first phase of an IT recovery cycle.

Importantly, despite global uncertainties, including the Middle East conflict, there has been no visible disruption in demand, suggesting that enterprise technology spending is becoming more resilient and less reactive to short-term geopolitical noise.

Open a free account today

Invest in tomorrow with just one click

From Experimentation to Execution: AI Infrastructure

The most meaningful shift, however, is happening in artificial intelligence. TCS highlighted a clear transition from experimentation to implementation, which fundamentally changes the revenue profile of AI. During the last phase, enterprises were testing AI capabilities with limited budgets. Now, they are beginning to deploy AI at scale, which requires significantly higher and more sustained spending.

TCS is positioning itself not merely as an AI application provider but as an infrastructure enabler. Through its “Hyper Vault” initiative and partnerships such as the one with OpenAI, where it has secured access to 100MW to 1GW of AI data centre capacity, the company is effectively building the foundational layer required for large-scale AI adoption. A potential partnership with Anthropic further strengthens this multi-ecosystem strategy. Instead of competing in short-cycle AI projects, TCS is investing in the long-duration, high-dependency layer of AI infrastructure, which tends to be more stable and scalable over time.

Another subtle but important insight is that many enterprises are underutilising AI tools they have already deployed. This creates an additional revenue opportunity, not from new deals alone, but from helping clients extract more value from existing investments. In effect, the AI opportunity is both expansionary and efficiency-driven.

TCS Q4 Concall: Sector Tailwinds & Margin Pressure

At a sector level, demand recovery remains uneven. BFSI continues to be cautious due to elevated interest rates, while manufacturing faces pressure from geopolitical and tariff-related uncertainties. On the other hand, the consumer segment is showing relative strength with market share gains, and telecom is emerging as a bright spot, supported by large deal wins such as the recent UK engagement. This divergence indicates that while the cycle is improving, it is not yet broad-based.

From a margin perspective, the near term will see some pressure. Wage hikes in Q1 are expected to create a 150-200 basis point headwind, which is typical in the early stages of recovery when costs adjust before revenues fully catch up. Management expects Q1 and Q2 to be seasonally stronger, and remains optimistic about international growth improving meaningfully by FY27, following a decline of 2.4% in FY26.

At the current valuation of approximately 16.8x FY27 estimated earnings, the stock reflects moderate expectations rather than aggressive growth assumptions. This leaves room for upside if the stabilisation in demand translates into a stronger recovery, particularly with AI-led spending gaining momentum.

Investor Takeaway

In essence, this concall does not signal a sharp turnaround but rather a transition phase. TCS is moving from a period of demand compression into one of gradual normalisation, while simultaneously investing in the next structural opportunity through AI infrastructure. This combination of stabilising demand and forward-looking capability building is what defines the current phase of the company.

Related Topics

Can REITs and InvITs Become India’s Next Retail Portfolio Essential?

Everyone Knows Bajaj Finance’s Playbook. So Why Can’t Anyone Copy It?

Beyond the Dark Store: Is Advertising Zepto's Real Business?

Vedanta Demerger: Why Aluminium Became the Market’s Favourite/Darling

NSE Extends F&O Market Close to 3:40 PM: What Traders Must Know

Elon Musk’s $119 Billion Terafab Bet: Can It Reshape AI Chips?

Rupee Crashes to ₹96: How Investors Can Profit From the Fall

The Rise of India’s Defence Sector: Stocks, Trends & Opportunities

SEBI introduces Verified Badge for Trading Apps to Curb Fake App Scams

Rupee Slips Past 95/USD | Factors Driving the Fall Despite RBI Intervention

The Popcorn Trade: How Dhurandhar 2 is driving PVR INOX Stock Higher

Oil Is Surging After The Iran Strikes. So Why Isn’t Gold Following?

What’s Getting Cheaper & Costlier in Budget 2026: A Simple Money Guide

Union Budget Day & Market Behaviour: 15 Year Trend Analysis (2011-2025)

Maruti Q3FY26 Profit Up 4%: Losing Grip on India’s Car Market?

New Year, New Financial Goals: Make SIP Your 2026 Resolution

Infosys ₹18,000 Crore Share Buyback: Record Date & Why Promoters Opted Out?

Nifty 50 Performance Since Last Muhurat Trading: Nifty Top 10 Performers

Diwali Muhurat Trading: Can Nifty’s 7-Year Winning Streak Continue?

Tata Motors Demerger Gets NCLT Nod: What Shareholders Must Know

Muhurat Trading 2025 on 21 Oct: Everything You Should Know

Tuesday is the New Thursday: NSE & BSE Expiry Shift from Sep 2025

How Jane Street Snatched ₹36,500 Crore While India's Youth Lost Everything

Axis Bank Q1FY26 Results: A Mixed Bag, but Long-Term Picture Still Intact

Indian Stock Market Outlook: What Happened And Way Forward