When India’s Power Centres Said “No” to Gold

By

Arihant Team

Three powerful forces converged in 72 hours. The Prime Minister, a 15% customs duty hike, and HDFC Mutual Fund withdrawing its own gold NFO. Here is what it means for your portfolio and how to think clearly when everyone around you is still dazzled by yellow metal.

In This Article

- Introduction

- Understanding the Gold Rally

- The 72 hours that changed Gold Investing

- But Should You Actually Worry?

- The Behaviour Gap: The Tax You Pay Without Knowing It

- What the NFO Tells Us About the Industry

- Investor Takeaway

Introduction

11th May 2026, Prime Minister Modi made an appeal on national television: don't buy gold for the next year. By Tuesday morning, the Union government had raised customs duty on gold and silver to 15%. By Tuesday evening, HDFC Mutual Fund, India's largest AMC, quietly withdrew its Gold and Silver NFO that was supposed to open that Friday.

Three very different institutions, acting independently, reached the same conclusion within 72 hours. In the world of finance, that kind of convergence doesn't happen by accident.

But let's slow down and actually understand what just happened because "sell gold" or "don't buy gold" is easy advice to give and hard advice to understand. The nuance matters, especially if you're a retail investor who bought gold ETFs in the last 18 months.

Understanding the Gold Rally

To understand where we are, you need to understand how we got here. Gold's rise wasn't random. It was driven by a very specific set of fears that seemed, for a while, entirely rational.

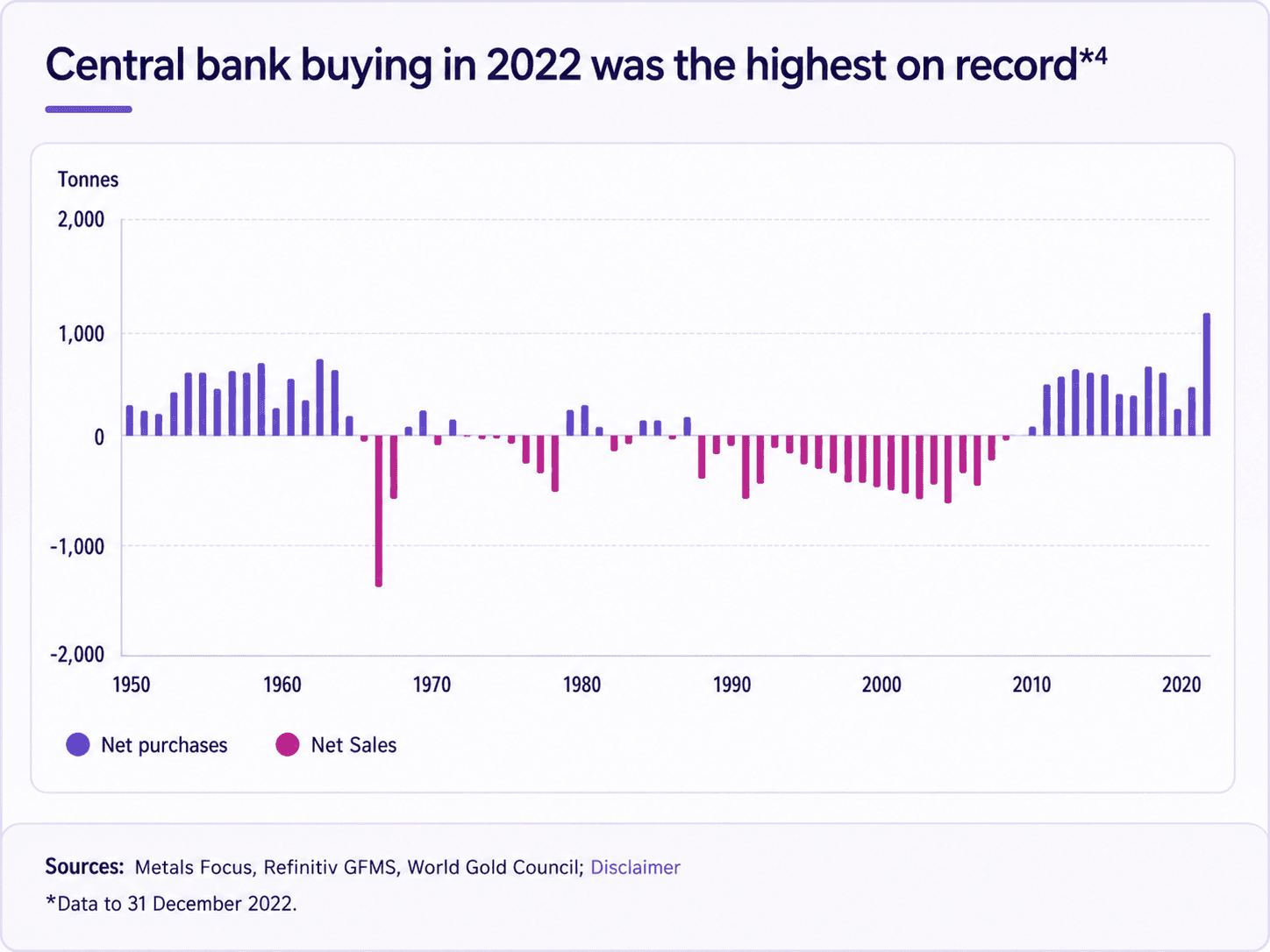

When Russia invaded Ukraine in 2022, Western nations did something unprecedented: they froze Russia's foreign exchange reserves, roughly $300 billion held in Western banks. Central banks around the world watched this and quietly asked themselves a chilling question: if it can happen to Russia, can it happen to us?

The answer, for many emerging market central banks, was to accelerate gold purchases. Gold can't be frozen. It doesn't sit on someone else's server. From 2022 onwards, central bank gold buying hit multi-decade highs, and this structural shift genuinely changed gold's demand picture. This is why even thoughtful, long-term analysts revised their view on gold upward as there was a real, structural reason behind it. Then came the geopolitical uncertainty of 2024-25: US election anxiety, tariff wars, Middle East tensions. Gold is the world's oldest safe haven, and in uncertain times, money poured in.

Indian retail investors, watching gold ETF returns of 60%, and more, began to notice. Notice what those numbers tell you: the massive 243% rise happened over five years, but the buying stampede i.e. the 75% of three years of inflows happened in just the last 8 months. Meaning, most Indian retail investors who piled into gold ETFs did so near the top, not at the beginning of the rally?!

The 72 hours that changed Gold Investing

Now let’s look at the timeline of that 72 hour:

- Sunday, May 11 - Prime Minister's Appeal

PM Modi publicly appealed to citizens to avoid buying gold for at least a year. India's gold imports are a major driver of the current account deficit. When oil prices rise and gold demand spikes simultaneously, it puts pressure on the rupee. - Tuesday, May 13 - Customs Duty Raised to 15%

A 15% customs duty on gold and silver was introduced to make imports expensive, dampening demand, making future returns harder to achieve, and signalling that the government is serious about curtailing the gold rush. For Gold ETFs (which track international gold prices but are denominated in rupees), this duty affects the physical gold backing the funds. - Tuesday, May 13 - HDFC Mutual Fund Withdraws Its Gold & Silver NFO

This is the one that should make retail investors sit up. HDFC Mutual Fund is India's largest AMC. They had planned a Gold and Silver NFO, a new fund offering to open on Friday. By Tuesday evening, they pulled it.

Launching an NFO involves filings, marketing and distribution work. So, withdrawing it at this stage suggests that the fund house may not be comfortable launching a new gold product at current valuations.

| Arihant Commentary: Mutual fund houses earn fees based on the assets they manage. So, an NFO is not just a new product. It also helps create buzz, bring in fresh money and grow AUM. When a fund house voluntarily withdraws an NFO, it means they genuinely believe the timing is bad and the reputational risk of launching at a market peak outweighs the fee income. |

But Should You Actually Worry?

If you bought gold for the right reasons early on, you're fine. Say you have ~10% of your financial portfolio in gold bought as insurance against currency debasement, geopolitical shocks, or systemic risk then you are doing exactly what gold is meant to do. You don't need to panic sell.

The question of "too much gold" is about allocation, not about gold being fundamentally worthless. It still serves a purpose in a diversified portfolio. The problem is concentration, not gold itself..

Most Indian families already have significant gold exposure that they don't count: their jewellery. The average middle-class Indian household holds gold jewellery worth 15 lakh, sometimes much more. If your jewellery represents ~20% of your net worth, and you've added gold ETFs on top, your actual gold allocation could be ~35% of your wealth. That counts as concentration, not diversification.

And here's a counterintuitive truth about safe havens: they stop being safe when everyone owns them. Gold at five standard deviations above its inflation-adjusted historical norm means the market has priced in a lot of bad news. When everyone is already holding the "safe" asset, there's limited upside and meaningful downside if sentiment shifts.

We saw proof of this in January 2026: gold touched $5,595 per ounce and then fell 21% in 48 hours not because of an economic event, but because of a single US government personnel announcement. A 21% drop in two days is not safe-haven behavior. That's speculation masquerading as safety.

The Behaviour Gap: The Tax You Pay Without Knowing It

There's a concept in behavioral finance called the "behaviour gap." It's the difference between what an investment actually returns and what the average investor in that investment actually earns. It exists because humans buy after prices have risen (when they feel safe) and sell after prices have fallen (when they feel scared), the exact opposite of what generates wealth.

Globally, this gap runs at about 2.5 percentage points per year. In Indian gold over the last 18 months, it's almost certainly wider. Gold ETF inflows hit a record ₹24,040 crore in January 2026, the highest ever. For the first time, gold ETF inflows actually exceeded equity mutual fund inflows. By April, those inflows had collapsed to ₹3,040 crore. An 87% fall in 90 days.

| Arihant Commentary: Tens of thousands of retail investors poured money into gold ETFs at or near the peak. The rally has already started losing steam. Many of those investors are now sitting on flat or negative returns after paying entry-level prices for an asset they bought because it had already gone up 243%. |

What the NFO Tells Us About the Industry

Also, there's a broader lesson here that goes beyond gold. Mutual fund NFOs tend to cluster around hot themes. We've seen infrastructure NFOs at infrastructure peaks, PSU NFOs at PSU peaks, small cap NFOs at small cap peaks. The NFO pipeline is often a contrary indicator, it tells you what retail investors are currently excited about, not what will deliver returns over the next five years.

HDFC pulling its gold NFO at this moment is genuinely unusual. And it's worth internalizing: even the institutions that profit from selling you gold products are saying the timing is wrong. Listen to what they do, not just what they say.

Investor Takeaway

Gold has been a genuine wealth preserver over very long time horizons. It has a place in a well-constructed portfolio. None of that has changed.

What has changed is the price, the narrative density around it, and the policy environment. When the PM, the government, and India's largest AMC all act in the same direction within 72 hours.

The gold party isn't necessarily over forever. If you're holding gold sensibly as ~10% portfolio insurance, do nothing. If you've been chasing the rally and gold now dominates your portfolio, use any strength to rebalance.

And if you were about to start a gold SIP this month, put that money in equity instead, and revisit gold when it's boring again.

Related Topics

Everyone Bought Gold ETFs in January. Here's Why They're Selling Now

EGR vs Gold ETF: Key differences, taxation & which should you choose?

Electronic Gold Receipts Explained: A Smarter Way to Invest in Gold?

Oil Is Surging After The Iran Strikes. So Why Isn’t Gold Following?

Physical Gold vs Gold ETFs: Which investment is best for Indian investors?

How Your Gold Profits Are Taxed And Budget 2026 Expectations For Gold

Gold & Silver Rally Amid US–Venezuela Conflict: What Should Investors Do?

Silver vs gold 2025: Why smart investors are choosing silver now