Everyone Bought Gold ETFs in January. Here's Why They're Selling Now

Gold ETFs grabbed headlines in early 2026 after attracting record inflows that nearly matched equity mutual funds. But the momentum didn't last. Was it the end of the rally or simply a pause? And more importantly, what do the latest trends actually tell investors about gold today?

In This Article

- Introduction

- Inside the record Gold ETF inflows

- Why Gold ETF inflows lost momentum

- Long term Gold ETF trend is still intact

- Where Gold ETFs stand as on July 2026

- Investor Takeaway

Introduction

Every few months, one chart or one number does the rounds in every group chat I'm part of, and for a while this year, that number was simple. Gold ETFs had pulled in more money than equity mutual funds for the first time in India's history. People treated it like proof that gold had permanently taken over as the default place to park money.

I went back and actually traced what happened after that headline instead of just accepting it, and the real picture turned out to be a lot more useful than the original story.

Inside the record Gold ETF inflows

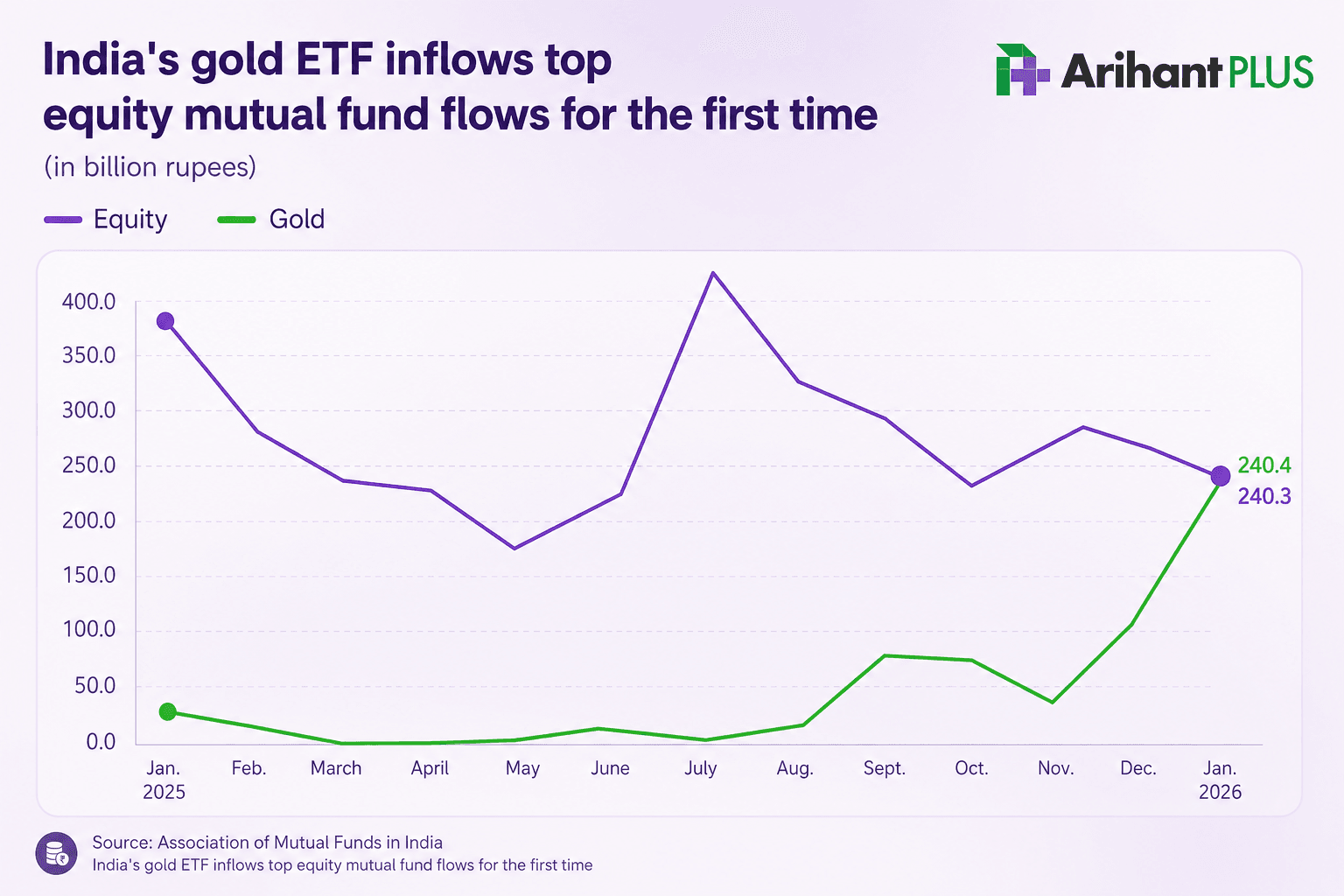

In January this year, gold ETFs pulled in close to 24,040 crore rupees in a single month, nearly matching equity mutual fund inflows of about 24,029 crore rupees, a gap of just 11 crore rupees separating history from an ordinary month. That surge didn't come out of nowhere either, since inflows had already jumped 211 percent in December and then roughly doubled again heading into January, pushing the financial year total for gold ETFs past 63,000 crore rupees.

Three things were feeding this at once.

• Geopolitical tension was pushing people toward an asset that doesn't depend on any government or company staying solvent.

• The rupee had weakened enough to make gold's rupee returns look even better on top of its dollar gains.

• Indian investors were genuinely getting smarter about treating gold as a core holding rather than a panic buy, with multi asset and hybrid funds pulling in over ₹10,000 crore that same month partly for this reason.

Right around the same time, SEBI stepped in and changed how gold and silver ETFs are actually priced. From April 1, 2026, fund houses had to stop leaning on the old London linked benchmark and start using domestic spot prices instead, the same ones used for settling physical bullion contracts in India.

Why Gold ETF inflows lost momentum

Here's what most people missed while that January number was making headlines. A rally that strong was always going to invite profit booking, and by May, that's exactly what happened. Gold ETFs recorded their first monthly outflow in 13 months, pulling out around ₹725 crore after a year of relentless inflows, and this wasn't investors losing faith in gold, it was simply people cashing out after a serious run, the same way anyone books profits on a stock that has climbed too far too fast. The series followed in June as well.

Policy gave the reversal an extra push too. India's gold import duty jumped from 6 percent to 15 percent, which made it costlier for fund houses to keep buying physical metal to back new ETF units, and a few large AMCs even capped fresh inflows into their gold schemes for a while as a result.

The bigger surprise, though, was what happened to equities in the meantime. Back in January, money had been rotating toward large caps for safety, the classic sign of a nervous market. By May, small caps and mid caps were back leading inflows again, which tells you risk appetite came back a lot faster than the January mood suggested it would.

Long term Gold ETF trend is still intact

None of this means gold's rise was fake or that it's done running for good. Gold ETF assets peaked at roughly ₹1.84 lakh crore, and the shift away from physical jewellery toward ETFs, digital gold, bars, and coins is still very real.

Yes, digital gold purchases, imports, and ETF flows have cooled since the January peak, but buying remains above recent averages. Much of the slowdown reflects higher import duties, volatile prices, and a seasonal lull rather than a collapse in demand. Retailers, meanwhile, have seen more customers exchange old gold instead of making fresh purchases, with many expecting demand to recover from August as the festive season approaches.

Where Gold ETFs stand as on July 2026

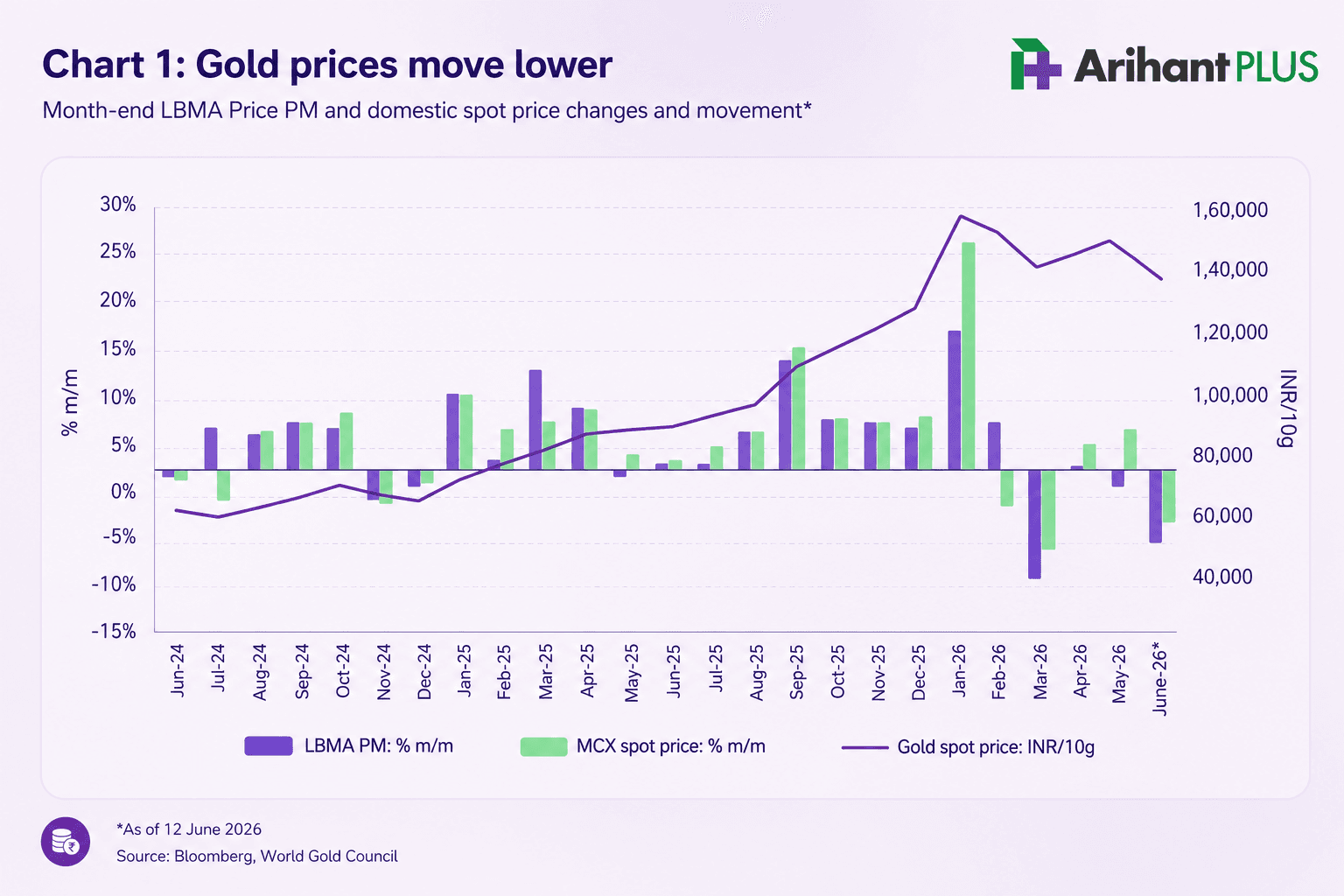

Gold touched over ₹1.6 lakh for 10 grams earlier this year but has since cooled, with domestic prices down about 3.7% since the end of May as expectations of higher global interest rates, improving risk sentiment, and ETF outflows weighed on demand. Even so, domestic gold remains up around 13.2% this year, largely because of the higher import duty and a weaker rupee, and is now trading near ₹1.4 lakh.

The Nifty, meanwhile, is trading near 24,290 while gold sits around 14,670 rupees per gram, which puts the Nifty to Gold ratio at roughly 1.66, back in the zone that has historically rewarded patience in equities rather than punished it.

Investor Takeaway

I'm not going to tell you gold's run is over or that equities are guaranteed to outperform from here. What the last six months actually taught me is that neither asset deserves blind loyalty, no matter how convincing the headline of the month sounds. Both have a place in your portfolio - one as a hedge and other as wealth creator.

Treat gold as a stabiliser you top up steadily, not a trade you chase after it's already run. Keep adding to quality equities through the dips instead of waiting for permission from the news cycle. The moment a "for the first time ever" headline starts feeling like gospel is usually the moment worth being a little more skeptical, not less.

Related Topics

EGR vs Gold ETF: Key differences, taxation & which should you choose?

Electronic Gold Receipts Explained: A Smarter Way to Invest in Gold?

Oil Is Surging After The Iran Strikes. So Why Isn’t Gold Following?

Physical Gold vs Gold ETFs: Which investment is best for Indian investors?

How Your Gold Profits Are Taxed And Budget 2026 Expectations For Gold

Gold & Silver Rally Amid US–Venezuela Conflict: What Should Investors Do?

Silver vs gold 2025: Why smart investors are choosing silver now