Capital Gains Tax in India: Simple Investing Guide in 2026

By

Arihant Team

Understand capital gains tax in India for FY 2025-26 with this simple guide. Learn LTCG & STCG rules, tax rates, indexation changes, and exemptions under Sections 54, 54F & 54EC. Discover smart strategies to legally reduce tax on shares, property, gold, and mutual funds.

In This Article

- Introduction

- What is a capital gain?

- Short-term vs long-term Capital Gain Tax

- Current tax rates for FY 2025-26

- What happened to indexation?

- How to legally reduce your capital gains tax

- One new rule to know for FY 2025-26

- Takeaway

Introduction

You invest in shares, mutual funds, property or gold with the hope that they grow over time.

When you sell them for more than you paid, the profit you make is called a capital gain. And like most income in India, a part of that profit may be taxable.

The good news is that capital gains tax is not as complicated as it sounds. Once you understand what you sold, how long you held it and which tax rate applies, it becomes much easier to plan better.

Here is a simple guide to help you understand the basics.

Open a free account today

Invest in tomorrow with just one click

What is a capital gain?

It's simply the profit you make when you sell a capital asset for more than you paid.

For example, if you bought shares, mutual funds, property or gold at one price and later sold them at a higher price, the difference is treated as a capital gain.

Capital Gain = Selling Price – Cost of Acquisition – Transfer Expenses – Cost of Improvement, if any

What you owe in tax depends on what you sold and how long you held it.

Short-term vs long-term Capital Gain Tax

Short-term capital gains arise when you sell capital assets within a short holding period, while long-term gains arise when you hold them longer. — The threshold being 12 months for listed equity shares and equity mutual funds, and 24 months for assets like gold, property, and debt funds.

In many cases, holding for the long term can reduce the tax rate. But the final tax depends on the asset, holding period and applicable exemptions.

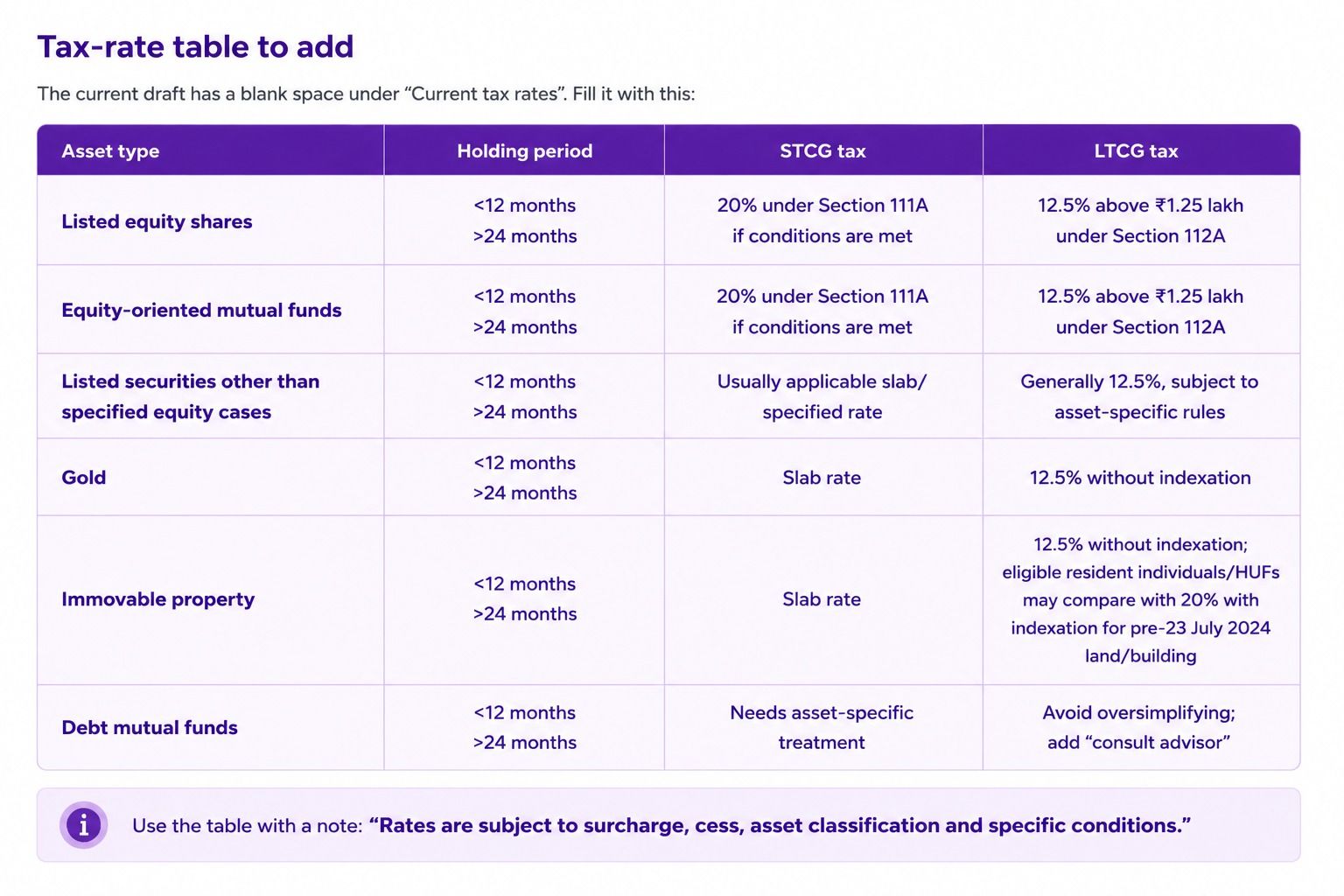

Current tax rates for FY 2025-26

Budget 20265 made no changes to capital gains tax rates — the rules from the Finance (No. 2) Act, 2024 continue to apply for FY 2025-26.

What happened to indexation?

Indexation was one of the most discussed changes from Budget 2024.

Earlier, indexation allowed investors to adjust the purchase price of an asset for inflation. This helped reduce the taxable capital gain, especially in the case of property held for many years.

Now, for land or building acquired before 23 July 2024 and sold on or after that date, resident individuals and HUFs have a choice. They can either pay 12.5% long-term capital gains tax without indexation, or 20% with indexation.

This means investors should calculate the tax under both options before making a decision. For older properties bought at a much lower price, the 20% rate with indexation may sometimes work out better

Scenario | Investment | Redemption Value | LTCG | Exemption Limit | Taxable Gain | Tax Payable |

Case 1 | ₹1,50,000 | ₹2,10,000 | ₹60,000 | ₹1,25,000 | ₹0 | ₹0 |

Case 2 | ₹1,50,000 | ₹2,95,000 | ₹1,45,000 | ₹1,25,000 | ₹20,000 | ₹2,500 |

How to legally reduce your capital gains tax

The Income Tax Act gives you three clean routes to save tax on long-term gains:

Section 54 - Sell a residential house and buy another residential house. If you sell a residential house and earn long-term capital gains, you may claim an exemption by reinvesting the gains in another residential house within the prescribed timeline.

In eligible cases, the exemption can also be claimed for two residential houses if the capital gains do not exceed ₹2 crore. However, this option is available only once in a lifetime.

Section 54F - Sell a long-term asset other than a residential house and buy a residential house. If you sell assets such as gold, shares, mutual funds or land, and reinvest the net sale proceeds in a residential house, you may be eligible to claim exemption under Section 54F.

This benefit is subject to conditions, including the number of houses you already own and the amount reinvested. The cost of the new residential house considered for exemption is capped at ₹10 crore.

- Section 54EC - Sell land or building and invest in specified bonds. If you sell land or building and earn long-term capital gains, you may invest up to ₹50 lakh in specified 54EC bonds within six months from the date of sale. These bonds are issued by specified institutions such as NHAI and REC, and must be held for five years.

One new rule to know for FY 2025-26

From FY 2025-26, capital losses have strict set-off rules. Short-term capital loss can be set off against any capital gains, while long-term capital loss can be set off only against long-term capital gains. Unabsorbed losses can be carried forward for up to 8 assessment years, subject to return-filing rules.

Also worth noting: LTCG does not qualify for the Section 87A rebate, meaning even if your total income is below ₹12 lakh, you still owe tax on capital gains.

Takeaway

Capital gains tax is not something to fear. It is something to plan for. A few simple habits can make a meaningful difference:

- Hold your investments for the right period. In many cases, moving from short-term to long-term can reduce the tax rate.

- Use the ₹1.25 lakh annual exemption on long-term gains from listed equity shares and equity-oriented mutual funds, wherever suitable. Some investors use tax harvesting by redeeming and reinvesting, but this should be done carefully after considering costs, market movement and tax rules.

- If you are selling property, gold or other long-term assets, check the available exemptions under Sections 54, 54F and 54EC before completing the transaction. Tax planning works best before the sale, not after it.

Most importantly, report your capital gains correctly in your ITR, even when the tax payable is low or nil.

A little planning today can help you avoid unnecessary surprises tomorrow.

Related Topics

EGR vs Gold ETF: Key differences, taxation & which should you choose?

Canara Robeco AMC IPO: Should You Apply for MF Giant’s Public Debut?

Dematerialisation of Mutual Funds: Complete Guide, Process & Benefits

What Is an Equity Fund? Types, Benefits & How to Invest in Equity Funds

Demystifying Demat Accounts: Meaning, Benefits, and How to Open One in India