Tamil Nadu CM Holds ₹213 Cr in One Bank Account — Smart Move?

By

Arihant Team

Tamil Nadu CM Vijay has ₹213 crore parked in a bank account—but is that really safe? This case reveals how inflation, low interest rates, and taxes silently erode wealth, turning “safe” savings into a losing strategy over time.

In This Article

- Introduction

- What is IOB actually paying on that money?

- Wait, but isn't keeping money in the bank "safe"?

- So, what should "growth money" actually be doing?

- What the Indian equity has actually delivered?

- Step-by-step comparison

- But what if the market crashes?

- So, what's the actual takeaway here?

Introduction

When Tamil Nadu's new Chief Minister C. Joseph Vijay filed his election affidavit in March 2026, the headline that went viral was simple: ₹624 crore networth. India's biggest box-office star had become one of Tamil Nadu's wealthiest politicians. Every news outlet ran the numbers.

What almost nobody talked about was where the money actually sits and what that quietly reveals about a financial mistake that millions of Indians make every single day.

Vijay's ₹624.74 crore breaks down into two buckets:

- Immovable assets (real estate): ₹220.15 crore — spread across residential, commercial, and agricultural properties in Chennai and Tamil Nadu

- Movable assets: ₹404.58 crore — investments, fixed deposits, and bank balances

Now look closer at that second number. Of the ₹404 crore in movable assets, more than half, i.e. ₹213.36 crore, is simply sitting in his savings account in the Indian Overseas Bank, Saligramam branch.

Imagine, a whopping ₹213 crore lying idle in a public sector bank. This is not unusual. In fact, this is exactly what most Indians do with large sums of money. It feels safe. It feels responsible. It is what our parents did and what their parents did before them.

So why is it a problem? Well, the problem is that "feels safe" and "is safe" are two very different things. Because everyday that money in his bank account is losing its value.

Open a free account today

Invest in tomorrow with just one click

What is IOB actually paying on that money?

Indian Overseas Bank's savings account interest rate is currently ~2.90%. Now, if Vijay's money is in a Fixed Deposit (which his affidavit suggests), IOB's FD rate on a 444-day scheme is around 6.60%.

Sounds decent, right? Then you introduce one number that changes everything: India's CPI inflation for April 2026 is 3.48% - the highest in over a year, with food inflation running at 4.2%.

Now let's do the math:

Indian Overseas Bank's savings account rate: 2.90%. On ₹213 crore, that's roughly ₹6.17 crore in interest every year.

Now bring in inflation. CPI for April 2026 stands at 3.48%.

- Savings account return: 2.90%

- Inflation: 3.48%

- Real return: −0.58%

Savings account interest is fully taxable. At the 30% bracket - which Vijay is firmly in — that 2.90% becomes an effective post-tax return of 2.03%.

- Post-tax return: 2.03%

- Real return: −1.45% (Factoring in inflation)

So, in actual rupee terms: Vijay earns ₹6.17 crore in interest, keeps roughly ₹4.32 crore after tax. Meanwhile, inflation is quietly eroding the purchasing power of ₹213 crore by about ₹7.41 crore every year.

Net result? He's losing nearly ₹3 crore in real purchasing power annually — even as the number in his passbook goes up.

The ₹213 crore isn't growing. It isn't even standing still. It's slowly going backwards.

Wait, but isn't keeping money in the bank "safe"?

Here's the honest definition of safety when it comes to money: your money is safe when it doesn't lose its purchasing power.

By that definition, an FD earning 6.6% when inflation is 3.48% and taxes take 30% of your interest is not safe money. It's slow-loss money. The number in your account goes up every year. Your passbook looks great. Everything feels fine.

But the ability of that money to buy things in the real world - groceries, school fees, petrol, property - is being quietly eroded. You're on a treadmill. You're moving, but you're not going anywhere.

And this isn't just one Vijay’s problem. This is a crore of Indians problem. ₹5 lakh in a savings account instead of ₹213 crore - same principle, same mistake, different scale.

So, what should "growth money" actually be doing?

Here's a framework that changes how most people think about their savings. Not all your money should do the same job.

Think of it in two buckets:

Safe Money — this is money you cannot afford to lose. Emergency funds. Goals you need to hit in the next 1–3 years. FDs, savings accounts, liquid funds all belong here. The job of this money is not to grow. Its job is simply to be there when you need it and beat inflation.

Growth Money — this is everything else. Money you won't touch for 2, 5, 7, 10 years. Money whose job is not just to beat inflation but beat it by a wide enough margin so you can build wealth and let compounding actually work for you.

Historically, among all the asset classes, equities has delivered one of the best returns in the long run. Real estate is great too – but you need to diversify your money across asset classes. Concentration in any single asset class is a risk in itself.

What the Indian equity has actually delivered?

Historically, the Indian stock market has delivered annualised returns of 12–15% over the long term, far outpacing both inflation and fixed deposit rates.

Nifty 50, the index of India's 50 largest publicly traded companies, is a good barometer of the performance of Indian equities and it has delivered a compounded annual growth rate (CAGR) of approximately 12.64% per annum over the last decade (2015–2025). In the current year (YTD February 2026), the 10-year CAGR sits at 13.7%

Assuming that Nifty would give a 12% return. Even after considering inflation of 3.48%, the real return would be well over 8.5% per year, compounding. Compare that to the FD's real post-tax return of roughly 1.12%.

Investment Option | FD (IOB 444-Day Scheme) | Nifty 50 Index Fund |

Starting Amount | ₹100 | ₹100 |

Nominal Annual Return | 6.60% | ~12.00% |

Tax Impact | 30% tax slab applicable | Long-term equity taxation more efficient* |

Post-Tax Return | 4.62% | ~12.00% pre-tax CAGR used |

Inflation (CPI April 2026) | 3.48% | 3.48% |

Real Return After Inflation | ~1.12% | ~8.52% |

Value After 10 Years | ₹157 | ₹310 |

Growth Multiple | 1.57x | 3.10x |

Step-by-step comparison

Calculation Stage | FD Calculation | Nifty Calculation |

Step 1: Annual Return | 6.60% FD rate | 12.00% CAGR |

Step 2: Tax Adjustment | 6.60% − (30% tax) = 4.62% | Not adjusted here |

Step 3: Inflation Adjustment | 4.62% − 3.48% = 1.12% | 12.00% − 3.48% = 8.52% |

Step 4: 10-Year Growth | ₹100 × (1.0462)^10 = ₹157 | ₹100 × (1.12)^10 = ₹310 |

Note: LTCG tax of 12.5% on equity gains above ₹1.25 lakh per year is not factored into the Nifty calculation here. Real equity returns would be marginally lower after tax. FD tax assumes the 30% slab. Both figures are illustrative.

Put ₹100 in an FD at 4.6% post-tax: after ten years, you have ₹157. Put ₹100 in a Nifty 50 index fund at 12%: after ten years, you have ₹310. As you can see, the difference in the return generated is not insignificant, its massive. And, over ten years, this difference can erode your wealth considerably.

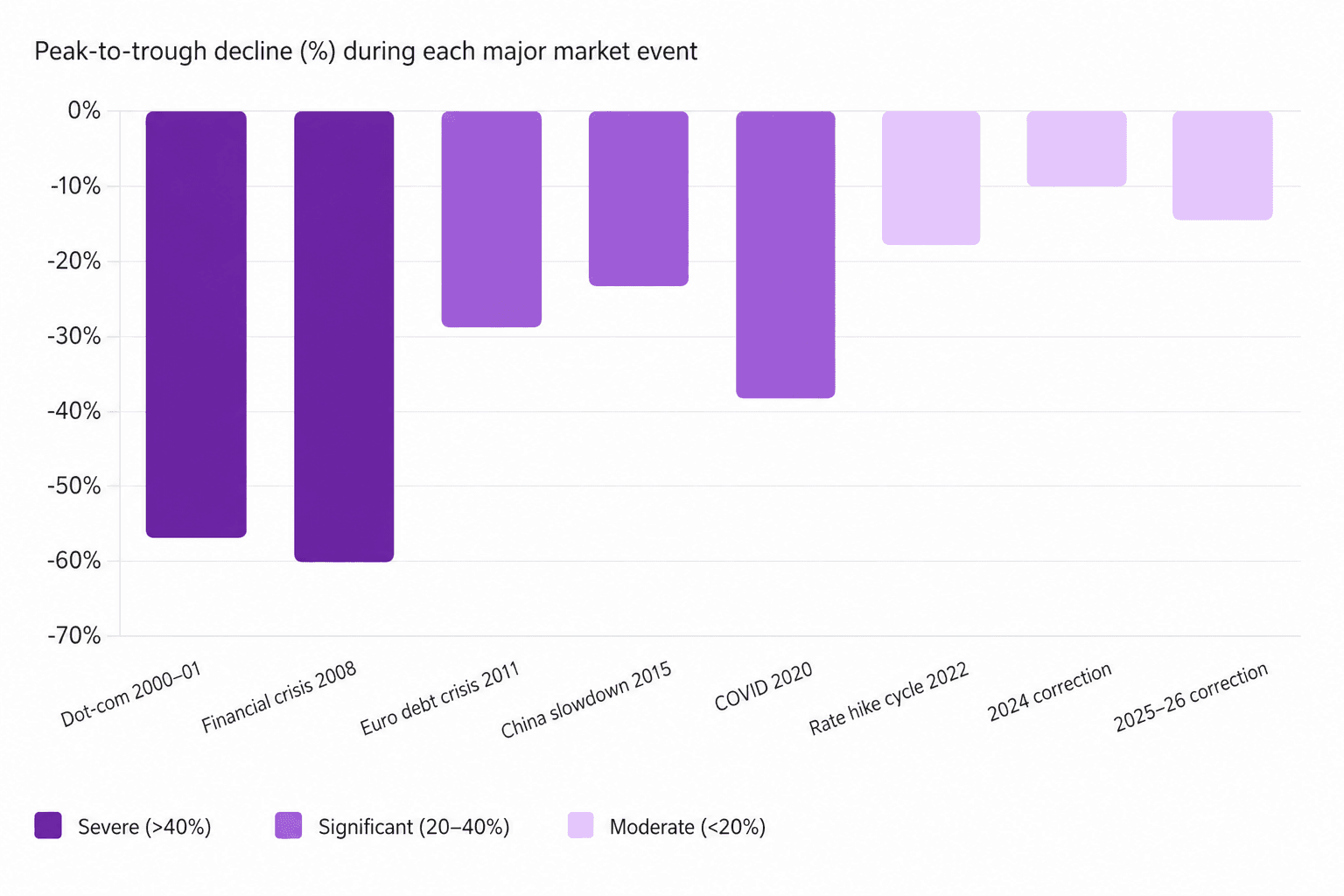

But what if the market crashes?

Fair question. And it deserves a straight answer.

The Nifty 50 can fall hard in any given year. In 2008, it dropped over 50%. In 2020, it fell 38% before recovering. A ₹1 crore portfolio can look like ₹60 lakh on paper within twelve months. That's real, and it's uncomfortable.

But here's the thing - that short-term pain is exactly why the returns exist. You're being compensated for sitting through the discomfort. And time horizon changes everything.

Equities are not for money you need next year. Not your emergency fund. Not your rent. markets can be volatile in the short term, and money invested for an emergency fund or a goal less than three to five years away has no business being in stocks. The key is time horizon. For the long-term investor, that short-term volatility is not a threat but a feature, it is precisely the risk premium that generates superior returns. Rupee-cost averaging through SIPs further smooths out market fluctuations, making equity investing accessible and disciplined.

The wealth that Vijay's ₹213 crore sitting in bank accounts will quietly lose to inflation over the next decade is exactly the wealth that a patient, long-term equity investor stands to gain.

Savings account risk is silent. No red numbers. No alerts. Just your purchasing power shrinking by 1.45% every year while the passbook keeps looking perfectly fine. Both risks are real. One just hides better.

So, what's the actual takeaway here?

This was never about Vijay. The man built ₹624 crore from scratch over three decades in cinema - that's extraordinary, and how he manages it is entirely his call.

But his affidavit handed us something rare - a verified, public, detailed look at how a very high net-worth individual structures their wealth. And what it shows is a pattern that's deeply familiar.

Overwhelming concentration in "safe" assets that are, in real terms, going backwards. Most of us do the exact same thing. Just with ₹5 lakh instead of ₹213 crore. The scale is different. The outcome isn't.

So here's the simple way to think about it:

- Safe money - 3 to 6 months of expenses, near-term goals, anything you'll need within 3 years - keep it liquid. Savings account, FD, liquid fund. Its job isn't to grow. Its job is to be there.

- Growth money - anything with a 5-year or longer horizon belongs in equities.

But you need to be cautious about where you invest in equities. Avoid tips from a cousin or a social media influencer, get help from real experts instead. You should start with mutual funds where the expert fund managers invest on your behalf for a small fee. Make sure to use SIP for rupee cost averaging and compounding benefit. A simple, diversified Nifty 50 exchange traded fund along with diversification with gold ETF is a good idea.

Related Topics

Understanding Bonus Shares and Their Impact on Your Portfolio

Understanding Stock Splits and Their Impact on Your Portfolio

What is share buyback? Why companies do it & how it impacts investors

How to Analyse a Stock in 2026: Fundamental + Technical Checklist

Where the Real Opportunities Lie in 2026: Investing in Uncertainty

Silver vs gold 2025: Why smart investors are choosing silver now

The Rise of Fake Trading Apps in India: Safe Investing Guide