Maruti’s Q4FY26 Profit Drops but Growth Outlook Remains Strong: Should you buy?

By

Arihant Team

Why did the investors ignore 7% dip in Maruti's profit and were bullish on the company as it jumped 5% after its results announcement? The answer lies in looking beyond profit. Maruti Suzuki’s Q4FY26 update reflects strong demand recovery and improving operational performance, With a large order backlog and low dealer inventory highlighting supply constraints, the company is accelerating capacity expansion to unlock growth.

In This Article

- Introduction

- Maruti’s Q4FY26 Performance Highlights

- Demand trends and underlying strength

- Supply Constraints and Capacity Expansion

- Product Portfolio and Strategic Positioning

- Maruti’s Evolving Customer Base

- Exports

- Margins and Cost Environment

- Growth Outlook

- So why does the confidence remain?

Introduction

There has been a growing belief in the market that Maruti Suzuki is no longer what it used to be. A legacy leader that once defined the passenger vehicle market now appears to be lagging behind, which is visible from its declining market share. It missed the early SUV momentum, has been cautious on electric vehicles, and continues to be associated with entry level cars in a market that is steadily moving up.

Add to that a decline in quarterly profits, and the question naturally follows. If the numbers are not perfect and the industry is evolving so quickly, why does confidence around Maruti remain intact?

Maruti’s Q4 update offers enough detail to understand how the pieces are coming together. Before we get to it, let’s take a look at its Q4FY26 results.

Maruti’s Q4FY26 Performance Highlights

- Net profit declined 6.9% year-on-year (yoy) to ₹3,590.5 crore. This was primarily due to a mark to market loss of around ₹750 crore linked to bond yield movements

- Maruti’s revenue remained strong at ₹52,449 crore recording a growth of 28.21% yoy .

- Volumes grew by 11.8 percent yoy to 676,209 units, with domestic sales at 538,994 units and exports at 137,215 units.

- Earnings before interest and tax increased by about 30.4% yoy to ₹4,400 crore.

- The company also declared its highest ever dividend of ₹140 per share, reflecting strong cash generation and balance sheet strength.

While the quarterly performance saw a temporary impact on profitability, the full-year picture remains strong.

FY26 turned out to be a record year for Maruti, with volumes reaching 24.2 lakh units. Net sales grew 20.2% yoy to ₹1,83,316 from ₹1,52,913 crore. Its consolidated net profit jumped1.2% to ₹14,679 crore from ₹14,500 crore.

Demand trends and underlying strength

The first sign that something is shifting comes from demand itself.

After a relatively soft first half of FY26, where growth stood at about 5.6%, the second half saw a clear pickup to around 12.3%. This was not just a cyclical bounce. The GST cut, especially on small cars, improved affordability and brought a large segment of buyers back into the market.

But the more telling signal is not just growth, it is unmet demand.

Maruti is currently sitting on a pending order book of around 1.9 lakh units, including nearly 1.3 lakh small cars. At the same time, dealer inventory is only about 12 days. In simple terms, cars are getting sold almost as soon as they reach dealerships.

Supply Constraints and Capacity Expansion

What makes this more interesting is that Maruti has not left this gap unaddressed.

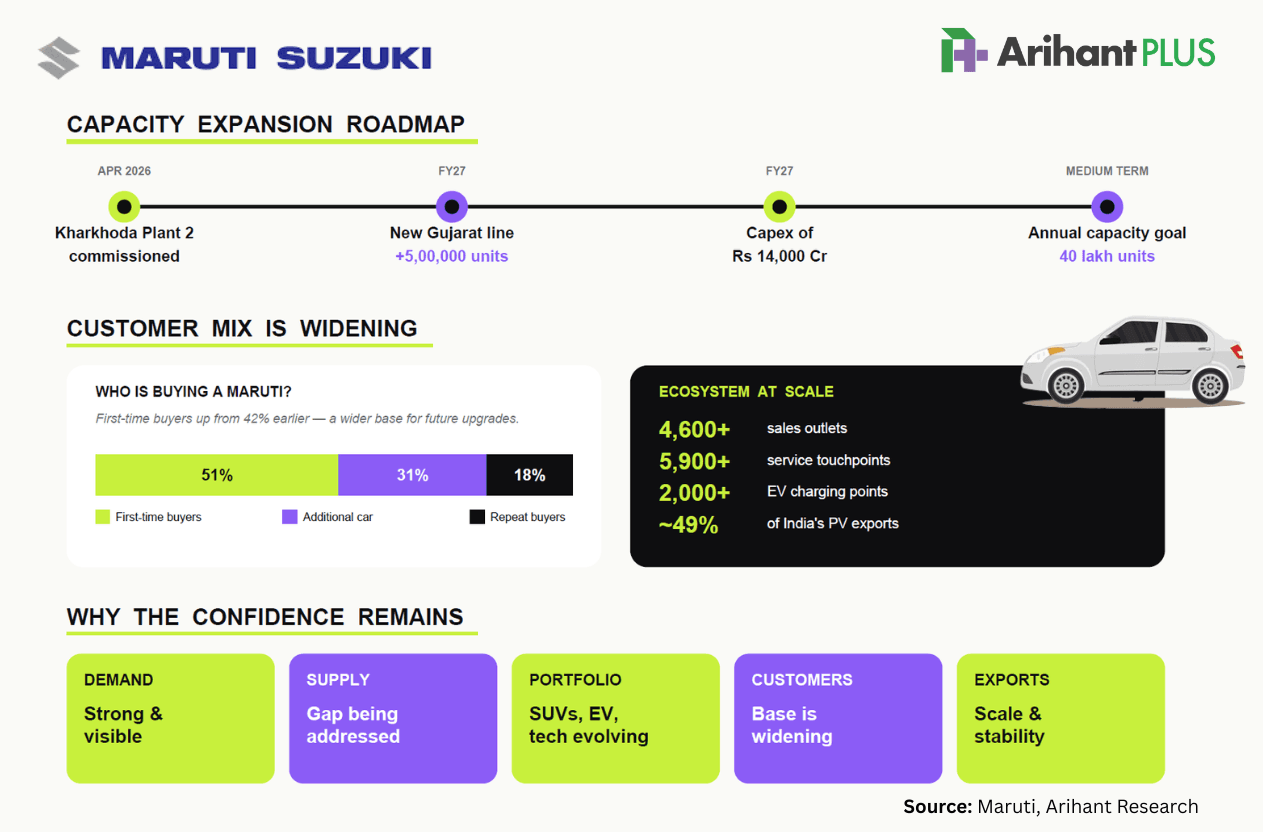

The company has already moved to expand capacity in a meaningful way. The second plant at Kharkhoda was commissioned in April 2026, and a new line in Gujarat is expected to come on stream in FY27. Together, these will add around 5 lakh units of incremental capacity in FY27.

Over the medium term, Maruti is working towards an annual production capacity of 40 lakh units.

This is backed by a planned capital expenditure of about ₹14,000 crore in FY27. As this capacity comes online, the current supply gap is expected to narrow, allowing Maruti to convert existing demand into actual sales rather than letting it remain in the pipeline.

Product Portfolio and Strategic Positioning

At the same time, the product story is also changing, even if it has not been widely acknowledged.|

In SUVs, where Maruti was once seen as behind the curve, traction is improving. The company’s Victorious model has scaled up quickly, becoming the fastest to reach 50,000 sales and winning Indian Car of the Year. The Dzire continues to remain among the top selling passenger vehicles, showing that the core portfolio still holds strong relevance.

On the technology side, Maruti has entered the electric vehicle space with the e Vitara, which is being positioned for close to 100 global markets. At the same time, the company is keeping a broader technology roadmap, including flex fuel vehicles as a five to ten year opportunity.

Maruti’s Evolving Customer Base

Another important shift is happening quietly in the customer mix.

First-time buyers now account for 51% of total customers, up from 42% earlier. Repeat buyers contribute around 18%, while additional car purchases make up 31%.

This matters because it expands the base of the market. A higher share of first-time buyers today means a larger pool of customers who can upgrade over time. It strengthens the long-term demand cycle rather than just supporting near-term volumes.

Exports

Maruti recorded strong sales in FY26. The company made highest ever domestic sales in FY26 with 19,74,939 units and its exports were also at a record of 4,47,774 units against 3,32,585 units a year ago.

Maruti is India's top passenger vehicle exporter, accounting for approximately 49% of PV exports, supported by a well-diversified global presence. This aspect of the business often receives less attention than it deserves, but it remains a critical pillar of Maruti’s long-term strategy.

Margins and Cost Environment

There are, of course, challenges.

Commodity prices, energy costs, and supply chain disruptions continue to create pressure. Geopolitical developments, including the situation in West Asia and constraints in rare earth materials, have added to uncertainty.

However, management expects these factors to stabilise over time. As that happens, margins are likely to benefit from better pricing, improved product mix, scale efficiencies, and ongoing cost control measures. The long-term aspiration of around 10% EBIT margin remains intact.

Growth Outlook

Maruti continues to invest in strengthening its ecosystem. The sales network has expanded to more than 4,600 outlets, supported by over 5,900 service touchpoints. This wide reach remains a key competitive advantage.

In the electric mobility space, the company has already set up more than 2,000 charging points and is working towards a significantly larger network over the long term. Logistics efficiency has improved as well, with the share of rail transport increasing to 26.5% from 5.1% in 2016.

So why does the confidence remain?

When viewed in isolation, parts of the story can raise questions. A cautious EV approach, a temporary dip in profits, or a legacy perception can all shape the narrative.

But when the pieces are brought together, a different picture emerges of Maruti.

- The company’s demand is strong and visible.

- The supply gap is being actively addressed through capacity expansion.

- The product portfolio is evolving across SUVs, safety, and technology.

- The customer base is widening.

- Exports continue to provide scale and stability.

And importantly, the company is investing ahead of the curve rather than reacting late.

Related Topics

Trent announces 1:2 bonus; record date May 29, posts strong Q4FY26 results

What should Indian investors do amidst Iran-Israel-Gulf conflict

Tata Motors Demerger Gets NCLT Nod: What Shareholders Must Know

ICICI Lombard Q1FY26 Result: Profit jump 28.7%, Strong Margin & Digital Momentum