Vi Q4FY26 Review | Is Vodafone Idea Finally Turning the Corner?

By

Arihant Team

Vi's Q4FY26 results carry the hallmarks of a genuine inflection point, stabilising subscribers, rising ARPU, a debt-lightened balance sheet and a promoter writing a $500 million cheque. Here is what the numbers say, and what they don't.

In This Article

- Introduction

- Vodafone Idea’s Q4FY26 Performance

- Vodafone Idea’s Subscriber Base

- Vodafone Idea’s Network Expansion

- Vodafone Idea’s AGR Relief

- Aditya Birla Group’s $500 Million Investment in Vodafone Idea

- Investor Takeaway

- FAQs

Introduction

For the better part of three years, the investment thesis on Vodafone Idea has been a binary one: survival or dissolution. The company haemorrhaged subscribers quarter after quarter, watched its credit rating sit deep in junk territory, and carried the spectre of an unresolved AGR (Adjusted Gross Revenue) liability that made any balance-sheet model a work of fiction. The stock was, for many institutional investors, simply uninvestable.

Q4FY26 does not make Vi a finished turnaround. But it does move the story from "will it survive?" to "can it grow?" and that is a materially different conversation for equity holders.

Vodafone Idea’s Q4FY26 Performance

The numbers from Q4FY26 mark an important inflection point for Vodafone Idea.

Revenue for the quarter stood at ₹11,332 crore, up 2.9% year-on-year, with the highest average daily revenue in six years. On an equal-day basis, sequential revenue grew 2.3%, showing real business momentum beyond calendar effects.

EBITDA margin expanded to 43.1%, showing operating leverage. FY26 EBITDA grew 4.8% to ₹19,003 crore, ahead of revenue growth.

| Consolidated (₹ Cr) | Q4FY25 | Q3FY26 | Q4FY26 | FY25 | FY26 |

|---|---|---|---|---|---|

| Revenue from Operations | 11,014 | 11,323 | 11,332 | 43,571 | 44,873 |

| EBITDA | 4,660 | 4,818 | 4,889 | 18,127 | 19,003 |

| EBITDA % | 42.3% | 42.6% | 43.1% | 41.6% | 42.3% |

| PAT | (7,166) | (5,286) | 51,970 | (20,217) | 34,552 |

PAT swung to ₹51,970 crore in Q4FY26 from a loss of ₹7,166 crore in Q4FY25, but this is largely due to a one-time, non-cash AGR accounting gain. It should not be read as operating profitability.

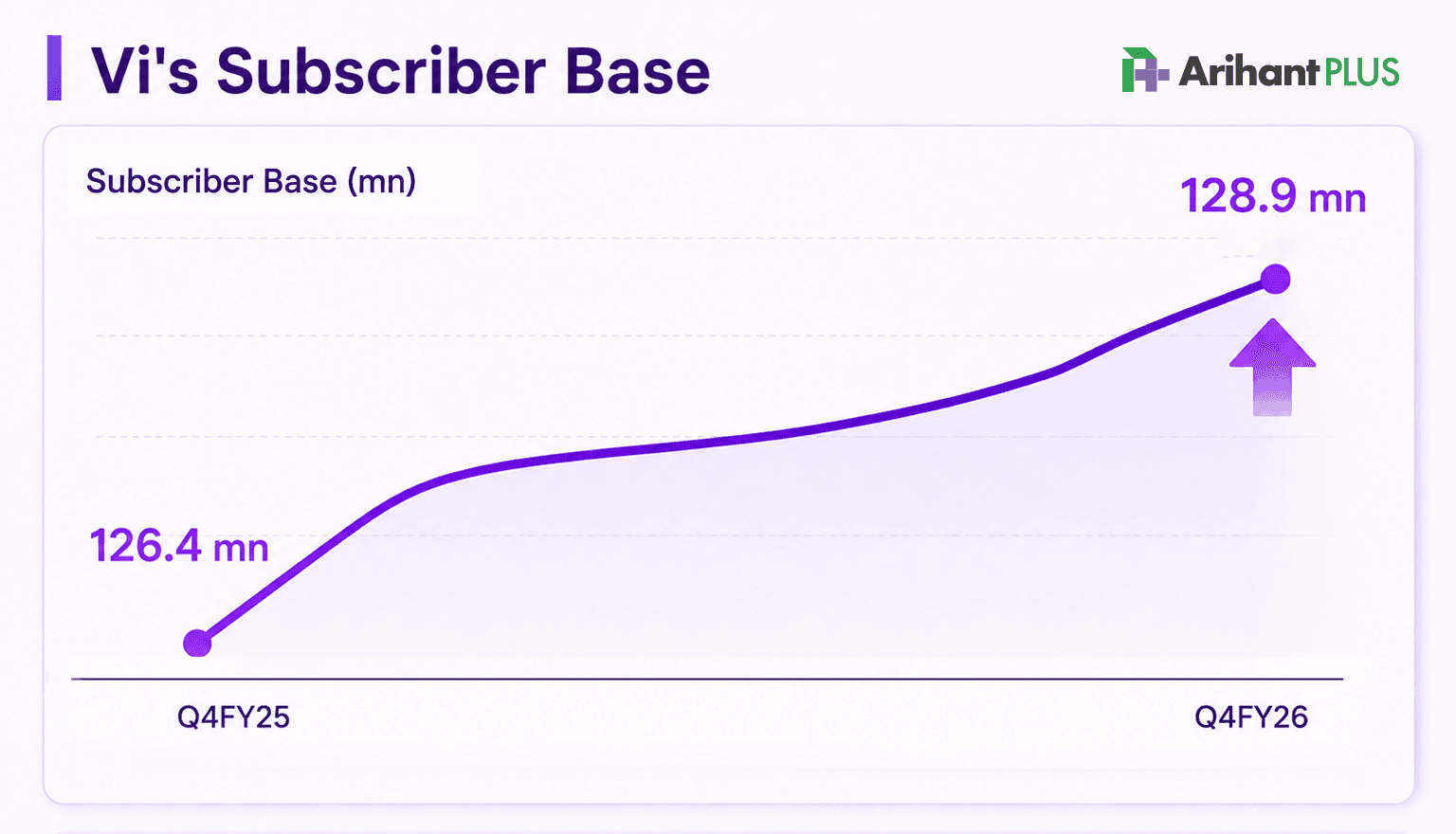

Vodafone Idea’s Subscriber Base

For Vi, subscriber count has always been the key number to watch. After several quarters of decline, the company finally saw monthly subscriber additions turn positive from February 2026.

The total customer base is now stable at 192.8 million. More importantly, its 4G/5G user base has grown to 128.9 million from 126.4 million in Q4FY25. This is the customer segment that matters most, because it supports better ARPU and stronger data revenue.

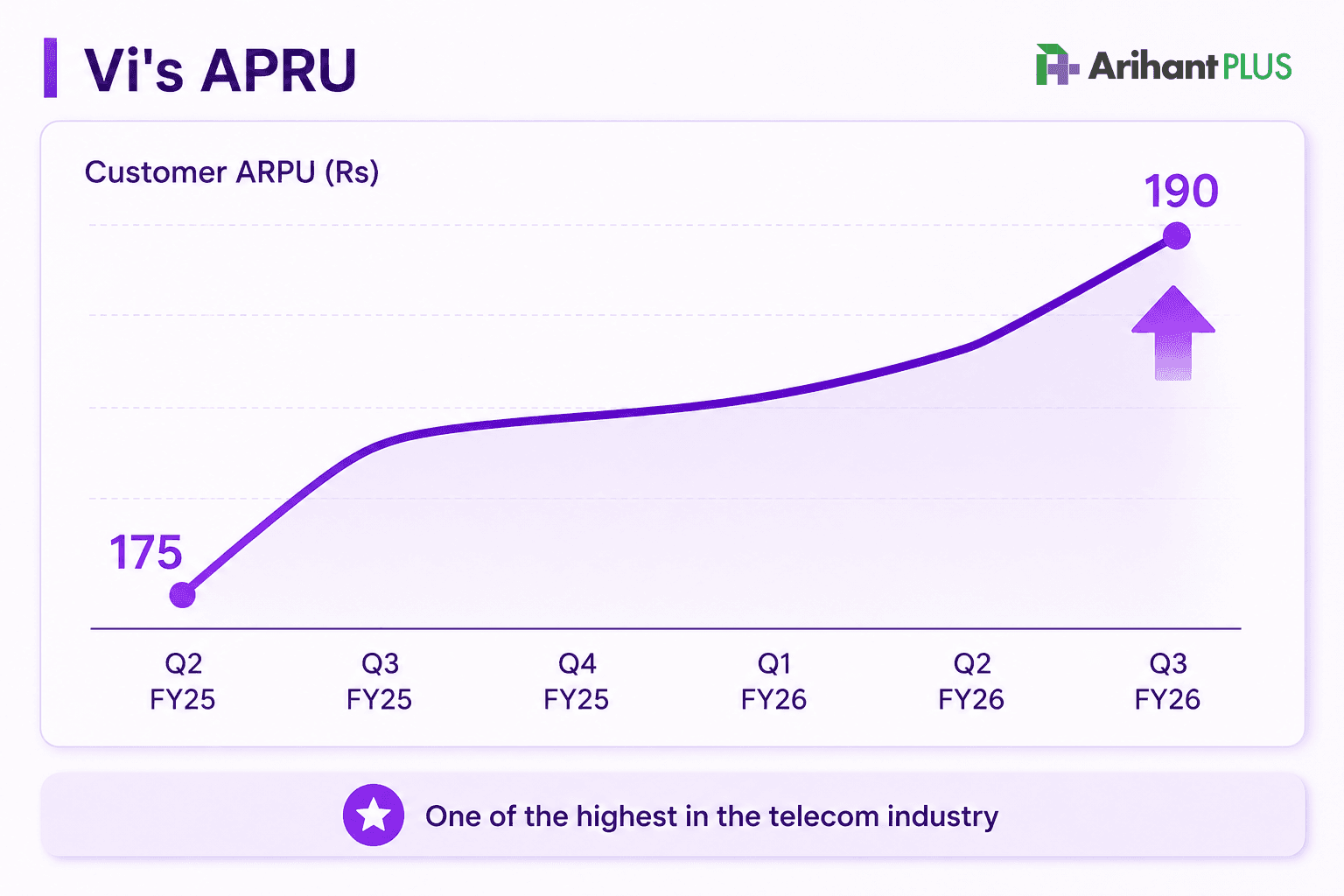

ARPU remains a key positive. It rose to ₹190 in Q4FY26 from ₹175 in Q4FY25, up 8.3% year-on-year and the highest in the industry as per the company.

This matters because Vi is now seeing ARPU growth alongside a stabilising subscriber base. That is a healthier revenue mix.

Postpaid is another steady bright spot. Vi has reported positive net additions for eight straight quarters, adding to a stickier and higher-value customer base.

Vodafone Idea’s Network Expansion

Vi’s recovery comes down to one simple question: can the network improve fast enough to stop customers from leaving?

The capex numbers suggest the company is finally investing behind that answer. After years of pressure, Vi is putting money back into network expansion, coverage, and capacity. That matters because in telecom, better network quality is not just a service upgrade. It is the foundation for retaining subscribers, winning back confidence, and rebuilding growth.

Vi is finally investing where it matters most: the network.

The company launched 5G in Mumbai in March 2025 and has now expanded it across all 17 priority circles, which contribute nearly 99% of its revenue. With 5G live in over 80 cities, Vi is no longer just defending its 4G base. It is back in the 5G conversation.

The 4G network is also improving. Data capacity grew over 12% year-on-year, and coverage now stands at 86.3% of the population. Vi is targeting 95%+ coverage in its 17 key circles with planned investments.

This matters because the network gap was one of the biggest reasons customers left. Closing that gap is the first step to stopping churn and eventually winning users back.

But network repair is only one part of Vi’s recovery. The other major overhang has been the balance sheet, especially the AGR dues.

Vodafone Idea’s AGR Relief

AGR has been Vi’s biggest overhang for years. The uncertainty around dues, timelines, and payment structure made it difficult for investors to value the business with confidence.

Q4FY26 brings some clarity. The one-time accounting gain comes from AGR re-assessment and the recognition of the present value of future payments. In simple terms, the liability is now easier to model, instead of being treated as one large unresolved burden.

This matters for lenders, rating agencies, and equity investors. Vi’s cash obligations are now more visible, which reduces uncertainty around the balance sheet.

The credit market has already responded. ICRA upgraded Vi’s rating to BBB (Positive) from BBB- (Stable) in March 2026. Bank debt has also reduced sharply, from ₹2,326 crore a year ago to ₹726 crore as of March 31, 2026.

Aditya Birla Group’s $500 Million Investment in Vodafone Idea

One of the strongest signals in Q4FY26 is the Aditya Birla Group’s decision to invest $500 million into Vi through fully convertible warrants.

The Board has approved warrants worth ₹4,730 crore on a preferential basis. Each warrant can convert into one fully paid-up equity share.

This is important because it is equity capital, not debt. It is also not a bailout. It is promoter capital coming into the business.

For the market, that matters. A promoter-led equity infusion signals confidence in the company’s future and strengthens alignment with minority shareholders. It shows that the controlling shareholder still sees value in Vi and is willing to back the recovery with capital.

Investor Takeaway

And hence, the bull case on Vi has always been simple: India’s telecom market needs a viable third player.

With Jio and Airtel holding strong pricing power, Vi’s survival matters not just for the company, but for market balance. The government, regulators, and now the Aditya Birla Group have all backed that outcome in different ways.

Q4FY26 shows those bets are starting to work. The question is no longer whether Vi can survive. The question is whether it can execute.

FAQs

Why did Vodafone Idea report a profit in Q4FY26?

Vodafone Idea reported a PAT of ₹51,970 crore mainly due to a one-time, non-cash AGR accounting gain. This should not be seen as normal operating profit.

What was Vodafone Idea’s ARPU in Q4FY26?

Vodafone Idea’s ARPU rose to ₹190 in Q4FY26 from ₹175 in Q4FY25. This was an 8.3% year-on-year increase and reflects a better revenue mix.

How is Vodafone Idea expanding its network?

Vodafone Idea is investing in 4G and 5G expansion. Its 5G services are live in over 80 cities, while 4G coverage has reached 86.3% of the population.

What does Aditya Birla Group’s $500 million investment mean for Vodafone Idea?

The $500 million investment shows promoter confidence in Vodafone Idea’s recovery. Since it is equity capital through fully convertible warrants, it strengthens the balance sheet without adding debt.

Related Topics

Rupee Slips Past 95/USD | Factors Driving the Fall Despite RBI Intervention

The Popcorn Trade: How Dhurandhar 2 is driving PVR INOX Stock Higher

Sensex down 8% due to Iran war: Should you pause SIP or buy the dip?

What’s Getting Cheaper & Costlier in Budget 2026: A Simple Money Guide

Maruti Q3FY26 Profit Up 4%: Losing Grip on India’s Car Market?

Gold & Silver Rally Amid US–Venezuela Conflict: What Should Investors Do?

New Year, New Financial Goals: Make SIP Your 2026 Resolution

How Jane Street Snatched ₹36,500 Crore While India's Youth Lost Everything