Rupee Slips Past 95/USD | Factors Driving the Fall Despite RBI Intervention

By

Arihant Team

The rupee hit 95/USD amid strong external pressures like high oil prices and capital outflows. RBI intervened, but is focusing on managing volatility, not fixing levels. Global factors continue to drive weakness despite policy support. The currency remains in a fragile, volatile phase.

In This Article

- Introduction

- RBI’s strategy to support the rupee..

- Why rupee is still under pressure despite RBI intervention

- Real Drivers Behind Rupee Falling

- Investor Takeaway

Introduction

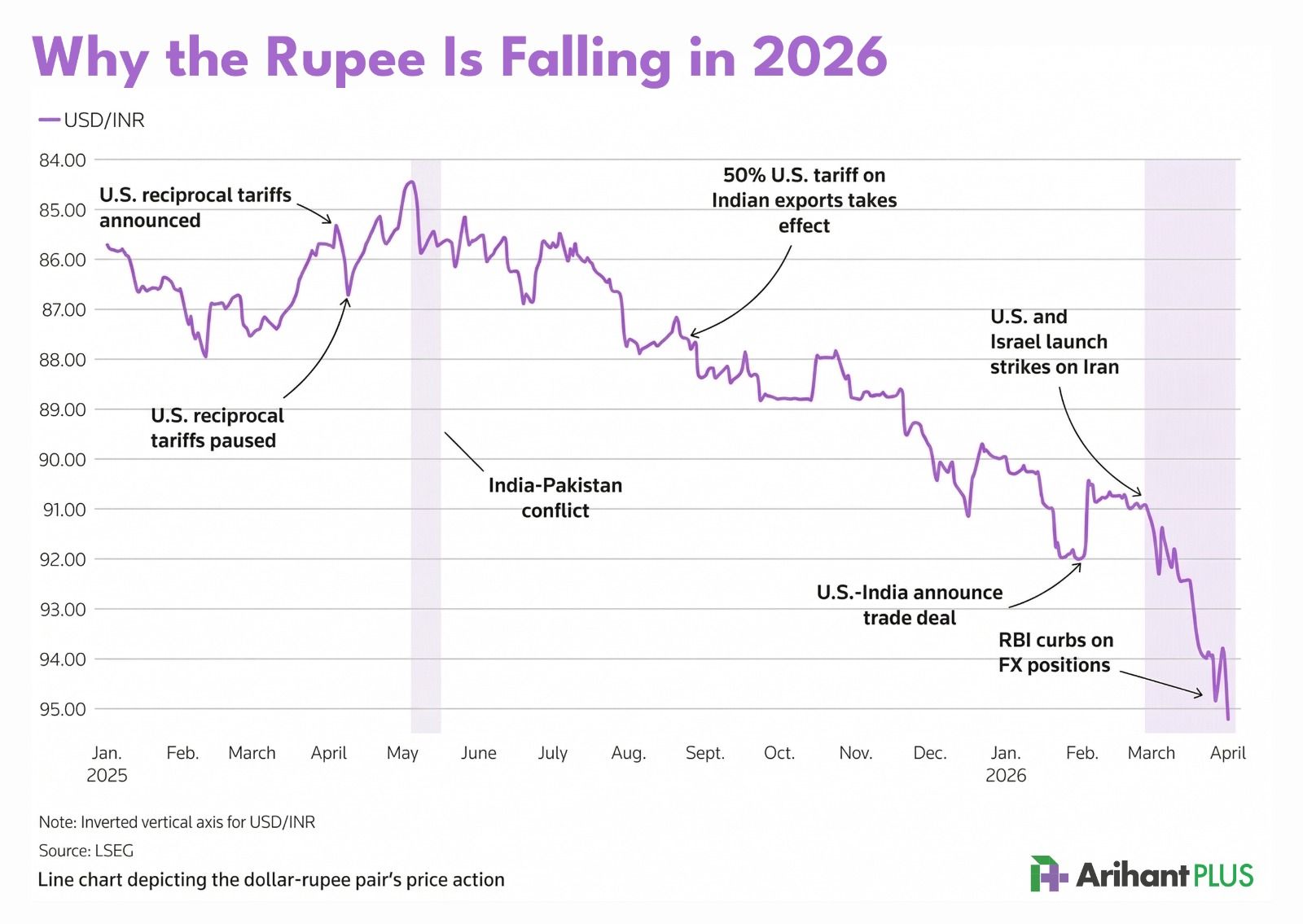

On March 30, 2026, the rupee briefly crossed 95/USD for the first time ever, before closing slightly stronger. But the message was clear, this wasn’t just another dip.

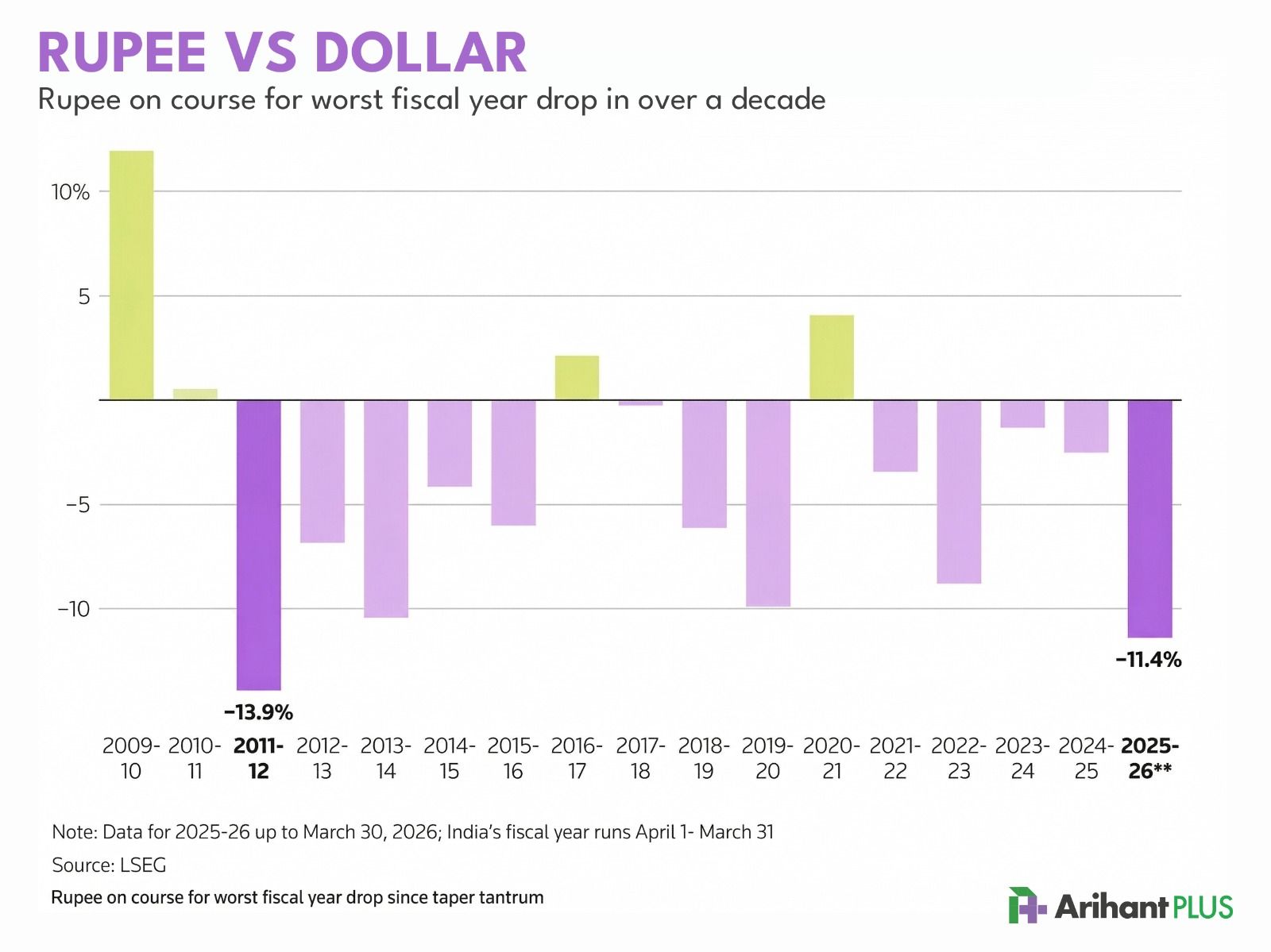

The rupee has already fallen ~11% over FY26, making it the worst annual decline in 14 years. And when a move like this happens in a country like India, it doesn’t stay in the currency market. It spreads.

India, where a large share of energy needs is imported, a weaker currency quickly translates into higher costs. Oil becomes more expensive, the current account deficit widens, and inflationary pressures begin to build. What starts as a move in the currency market gradually tightens financial conditions across the system, affecting bonds, equities, and capital flows.

Open a free account today

Invest in tomorrow with just one click

RBI’s strategy to support the rupee..

Faced with this pressure, the Reserve Bank of India stepped in but not in the way markets typically expect.

Instead of aggressively defending a particular level, the central bank chose to address what it saw as a structural distortion. Banks had built up large positions exploiting the gap between onshore and offshore currency markets. These trades were not just responding to rupee weakness; they were reinforcing it.

By capping banks’ net open dollar positions at $100 million, the RBI effectively forced a partial unwind of these trades. The idea was simple: reduce speculative pressure, narrow arbitrage opportunities, and restore some balance to the system.

Alongside that, it:

Sold dollars in spot & forward markets

Injected liquidity via bond purchases (OMOs)

Managed volatility instead of fixing a level

Taken together, these measures reflect a multi-layered approach. The RBI is not relying on a single lever but is instead attempting to balance currency stability, liquidity conditions, and market functioning simultaneously, a task that becomes significantly more complex in a volatile external environment.

For a brief moment, it appeared to work. The rupee even rebounded 1.5% intraday after intervention.

But the relief didn’t last.

Why rupee is still under pressure despite RBI intervention

To understand why the rupee has struggled to hold even after intervention, it helps to look at the constraints within which policy operates.

At the core is the classic “impossible trinity”, the idea that an economy cannot simultaneously maintain exchange rate stability, allow free capital movement, and retain full monetary policy independence. In the current environment of volatile capital flows and external shocks, the RBI is effectively prioritising monetary flexibility and capital mobility.

That choice has implications.

It limits the central bank’s ability to aggressively defend any specific level whether 94 or 95 without creating distortions elsewhere in the system. As a result, the rupee is being allowed to adjust in a more gradual, calibrated manner, with intervention focused on smoothing volatility rather than fixing direction.

This helps explain the recent price action. The rupee’s breach of 95 reflects the strength of external pressures, while the subsequent pullback toward 94 highlights the presence of policy support. Neither move is accidental, both are outcomes of a system where the central bank is managing trade-offs, not dictating outcomes.

The rupee today is not in a policy-controlled regime, but neither is policy irrelevant. It is trading in a space where domestic intervention and external pressures are both shaping outcomes, often in competing ways.

Real Drivers Behind Rupee Falling

To understand why the rupee continues to remain under pressure, it helps to step back and look at the broader backdrop.

Oil: With crude prices elevated amid geopolitical tensions, India’s import bill is rising at precisely the wrong time. Rising energy costs are likely to push the current account deficit wider, with estimates suggesting it could expand to around 2.6% of GDP in FY27. And this has even got India’s bond market 45 bps up.

Capital flow: Foreign investors have been steadily pulling money out of Indian markets, and the pace of these outflows has accelerated in recent weeks. This is not a slow, gradual shift, it is concentrated and momentum-driven, which makes it harder to counter.

Global environment: A stronger dollar and a risk-averse backdrop have put pressure on most emerging market currencies, and the rupee is no exception. In fact, it has been among the weaker performers in recent months.

Put together, these forces create a dynamic that feels strikingly familiar. The rupee’s decline this year is already among its steepest since FY2011-12, a period that was also marked by high oil prices, external imbalances, and sustained capital outflows.

Although, the comparison is not exact. India’s foreign exchange reserves are significantly stronger today but the underlying pattern is difficult to ignore. Once again, the currency is being shaped less by domestic policy and more by global conditions.

Investor Takeaway

What this episode ultimately highlights is not a failure of policy, but its limits.

The RBI can influence behaviour, reduce excess speculation, and smooth volatility. What it cannot do is fully offset a global shift in risk sentiment or a sustained rise in commodity prices.

For investors, this distinction matters.

The move to 95 is not just a level being tested; it is a signal that the rupee has entered a more fragile phase. In such an environment, the currency is likely to remain volatile, with movements shaped as much by developments outside India as by decisions within it.

History suggests that these phases do not last forever. External conditions eventually stabilise, and currencies find their footing again. But until that shift happens, the rupee is likely to remain under pressure not because policy is ineffective, but because the forces acting on it are larger than any single intervention.

Related Topics

The Popcorn Trade: How Dhurandhar 2 is driving PVR INOX Stock Higher

Sensex down 8% due to Iran war: Should you pause SIP or buy the dip?

What’s Getting Cheaper & Costlier in Budget 2026: A Simple Money Guide

Maruti Q3FY26 Profit Up 4%: Losing Grip on India’s Car Market?

Gold & Silver Rally Amid US–Venezuela Conflict: What Should Investors Do?

New Year, New Financial Goals: Make SIP Your 2026 Resolution

How Jane Street Snatched ₹36,500 Crore While India's Youth Lost Everything