Term Insurance vs Whole Life Insurance Which insurance is the right one for you?

By

Arihant Team

Term life insurance comes with an expiry but offers protection at lower cost, while whole life insurance offers lifetime coverage along with a built-in savings component that accumulates cash value.

In This Article

- "Insurance liya, accha kiya."

- Term life insurance - simple and affordable

- Whole life insurance - covers for your entire life

- Who should actually consider whole life insurance?

- ULIP: A mix of insurance and mutual funds

- ULIP vs Term Insurance: The math nobody shows you

- Term Insurance vs Whole Life Insurance

- Final word

"Insurance liya, accha kiya."

You've seen it everywhere - on that giant billboard near your office, mid-roll on YouTube before your favourite reel, and probably even on your cousin's WhatsApp status

The ad is catchy. The message is right. But here's the thing nobody tells you: which insurance should you buy? Because not all insurance is the same, and the difference can cost you your legacy.

Most people don’t know which insurance is right for them. So, before you buy that seemingly good insurance policy, you need to understand if it’s really for you.

There are two major types of life insurance policies available in India: term life and whole life insurance. And of course, there’s a third one too – ULIP (unit-linked insurance plan).

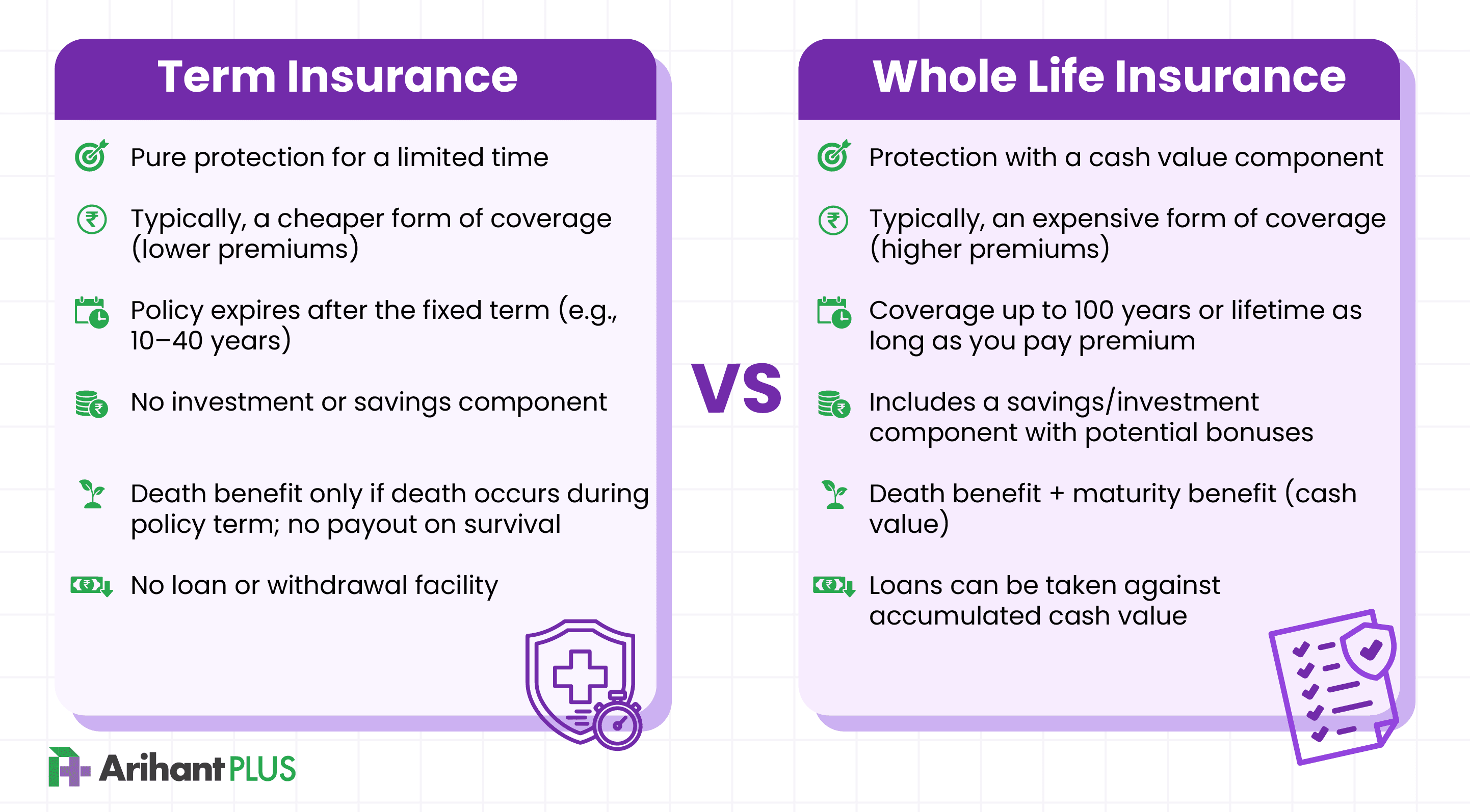

Term life insurance is life insurance with an expiration date, while whole life insurance protects you for your lifetime, it may give you an added cash benefit.

To put it simply, term life insurance is like renting an apartment. You pay every month, you're covered, and when the lease ends, you’re done. You don't own the house anymore, but it worked perfectly for that time you rented it.

Whole life insurance is more like buying a flat with a home loan - higher EMI, you own it forever, and there's a "savings" component built in. Sounds better, right? But is it?

Let's break both down.

Open a free account today

Invest in tomorrow with just one click

Term life insurance - simple and affordable

Term insurance does exactly one thing: it promises to pay your family a large sum of money if you die within a certain period, usually 10, 20, or 30 years. It offers protection for a set period.

That's it. No frills. No gimmicks. Just protection.

Once the policy expires and you survive, there are no payouts. The assumption is that by the time the working member of a family retires, their dependents won’t need the protection of an insurance payout anymore and can support themselves through their earnings or savings, making the insurance unnecessary.

If you're 28, earning ₹10 lakhs a year, and you have aging parents or a spouse depending on you, a ₹1 crore term plan till you are 70-year old might cost you somewhere around ₹700–800 per month. That's less than the cost of a weekend dinner.

And the best part? That ₹1 crore payout to your family is completely tax-free.

What term insurance doesn't do? It doesn't return your money if you survive the policy period. The premium is essentially gone. This bothers a lot of people. But think about it, your car insurance doesn't return your money if you don't crash. That's just how protection works.

Who is term insurance for?

A term insurance is suitable if you are a breadwinner and need income replacement for a specific time, like while you’re raising kids or have other dependents like your ageing parents. It gives you protection until your working years. For a longer-term plan, there’s always SIP investment you can opt for as it saves money.

Whole life insurance - covers for your entire life

Whole life insurance covers you for your entire life, often until age 99 or 100. It doesn't expire at a fixed time. To keep the policy active, premiums typically need to be paid throughout your life. And because it's essentially a guaranteed payout (since, well, everyone dies eventually), it also comes with a cash value component - a savings pool that grows slowly over time.

What whole life insurance doesn’t do: its savings portion can’t keep up with inflation

A term plan that costs ₹800 per month, your whole life insurance will cost you ~₹6,000–8,000 per month or more for the same cover. That's a significant difference. The cash value grows, yes — but the rate often doesn't even keep up with inflation!

And if you ever borrow against that cash value, your death benefit shrinks.

Let's do the math:

Say you're 30 years old and comparing a ₹1 crore cover:

| Term Insurance | Whole Life Insurance |

Monthly premium | ~₹800 | ~₹6,000+ |

Coverage period | 30 years | Lifelong |

Cash value | None | Grows (slowly) |

Returns if you survive | ₹0 | Some cash value |

Death benefit to family | ₹1 crore | ₹1 crore |

Now here's the thing — if you took the ₹5,200 difference every month and put it into a decent mutual fund at a modest 10% annual return, you'd have built a corpus well over ₹1 crore in 20 years. Your family wouldn't need insurance anymore because you'd have actual wealth to leave behind.

If you are an active investor, then you would rather calculate this and say that I will buy term insurance and invest the difference - and it makes a lot of sense.

Who should actually consider whole life insurance?

There are specific situations where whole life plans make sense:

- Legacy planning with guaranteed payouts. If you have lifelong financial dependents, say a child with special needs, and you need to guarantee a payout no matter when you pass away, whole life offers that certainty.

- People who genuinely won't invest the difference. If you know yourself well enough to admit that ₹5,000 extra in your account every month will just get spent, the forced savings of a whole life policy is better than nothing.

But for the average working Indian with a family, loans, and a 25–30-year career ahead? Term insurance, paired with good investments, almost always wins.

Just when you thought you had two options, the insurance industry says: hold on, here's a third.

ULIP: A mix of insurance and mutual funds

ULIP — Unit Linked Insurance Plan — is basically the industry's answer to the question "what if insurance and mutual funds had a baby?" It sounds too perfect on the surface: one product, two benefits- insurance protection and market-linked investment returns. You pay a single amount every month, and the insurer splits it. One part covers your life, the other gets invested in equity, debt, or balanced funds of your choice.

What ULIP actually does?

Your premium gets divided. Say you pay a premium of ₹8,000 per month – a portion goes toward your life cover (say ₹2,000), and the remaining (in this example, ₹6,000) gets invested in market-linked funds according to your risk appetite. You can also switch between funds a few times a year.

The death benefit is typically the higher of your sum assured or your fund value - so your family isn't left empty-handed if markets tank.

In ULIP, there's usually a 5-year lock-in period, which means you can't touch the money for at least five years. After that, you can withdraw your funds partially.

Tax benefits exist too — premiums up to ₹1.5 lakh qualify for deductions under Section 80C, and the maturity proceeds are tax-free under Section 10(10D) (with some conditions for high-premium ULIPs post 2021).

So far, so good. Now here's the part they bury in fine print.

What ULIP doesn't do

- It doesn't give you a meaningful life cover. For the premium you pay, the actual life cover in a ULIP is much lower than what a pure term plan would offer. If you're paying ₹8,000 per month in a ULIP, you might get a ₹10–20 lakh life cover. A smarter thing to do would be to take a term insurance for ₹800 per month and you can get ₹1 crore. That's a 10x difference in protection for one-tenth the price.

- It doesn't invest as efficiently as a mutual fund. ULIPs come loaded with charges - premium allocation charges (taken upfront before your money even gets invested), fund management charges (typically around 1–1.35% annually, capped by IRDAI), policy administration charges, mortality charges, and sometimes surrender charges if you exit early. In the first few years especially, a significant portion of your premium is eaten up by these fees. A direct mutual fund, by comparison, might charge 0.1–0.5% in expense ratio and nothing else.

- It doesn't let you leave easily. If life changes in year two or three - job loss, an emergency, a shift in financial goals, you're stuck. If you exit before 5 years, your money goes into a "discontinued policy fund" earning around 4% until the lock-in ends. Not exactly the market returns you signed up for.

A jack of all trades hence becomes a master at none. This is the core issue. A ULIP tries to be two things at once and ends up being a mediocre version of both.

ULIP vs Term Insurance: The math nobody shows you

Let's say you invest ₹10,000 per month in a ULIP. After charges in the early years, maybe ₹7,500–8,000 actually gets invested. A mutual fund SIP of ₹10,000 per month invests the full ₹10,000, minus a tiny expense ratio. Over 15–20 years, that difference compounds into a meaningfully large gap.

| ULIP | Term + Mutual Fund |

Monthly outflow | ₹10,000 | ₹10,000 |

Life cover | ₹15–25 lakhs (typically) | ₹1 crore+ |

Amount actually invested | ₹7,500–8,500 | ₹9,200+ |

Investment flexibility | Limited fund options | Full market access |

Exit flexibility | 5-yrs Lock-in | No lock-in |

So, who should invest in a ULIP?

To be fair - not every ULIP is a bad product for every person. Newer, leaner ULIPs have lower charges and more transparency. If someone is genuinely disciplined about long-term investing but struggles with self-control when money is liquid, the lock-in of a ULIP acts as forced commitment. For someone who would otherwise let both their insurance and savings lapse, a bundled product at least ensures something stays in place.

But if you're financially aware, have the discipline to run a term plan and SIPs separately, and want maximum transparency, then ULIPs rarely beat the alternative.

Term Insurance vs Whole Life Insurance

Insurance Liya, Accha Kiya. But, which one - Term, Whole or ULIP?

The ad is right. Getting insured is one of the most important things you can do for your family. However, it is important to know that one should always separate insurance and investment. Insurance is not an investment – it is a protection. Using them interchangeably usually means you end up doing both poorly.

Insurance companies often blur the line between protection and wealth creation by positioning insurance as investment. You should know, it is often a trap to get more commission out of you. By bundling savings with coverage, they market it as "comprehensive," because it sounds like you're getting more. In reality, its mostly they who benefit through hefty charges.

So, while insurance is important, but the type of insurance matters just as much as the act of buying it.

- If you're young, healthy, and want maximum protection at minimum cost — term insurance is almost certainly your answer. Lock in a policy early (premiums only get higher as you age), choose a reliable insurer with a strong claim settlement ratio, and pair it with systematic investments.

- If you have very specific legacy or estate planning needs - whole life might be worth a conversation with an advisor.

And if you're genuinely unsure? Don't wing it. Talk to someone who won't just push a product at you. There are platforms now that will walk you through the math, explain the fine print in plain language, and help you make a decision that actually fits your life - not just their sales target.

Because the best insurance policy isn't the most expensive one. It's the one that actually works when your family needs it the most.

Final word

Both term and whole life insurance offers protection for your family. However, it is important to know insurance is not an investment – it is a protection.

Insurance should first and foremost cover your financial obligations: your family's lifestyle expenses, your debts, your children's education. Once that's taken care of, investing separately is almost always more efficient.

A term plan is an affordable option and offers reasonable life coverage, while whole life provides lifelong protection and builds cash value, but at a higher cost. Which one is right for you depends on your financial goals, budget, and long-term needs.