FCNR(B) Deposits: What RBI's New Rules Mean for NRIs

FCNR(B) deposits have become more attractive for NRIs after RBI’s new rules. The scheme offers higher interest rates while protecting investors from rupee depreciation. Deposits remain tax-free in India and fully repatriable. With a limited-time window and leverage options, NRIs may consider evaluating this opportunity with their bank.

In This Article

- Introduction

- What Are FCNR(B) Deposits?

- RBI's Big Change: Absorbing the Hedging Cost

- Why this is such a Good Deal for NRIs

- Leverage Facility: Returns of Up to 26%

- Should You Look into this?

Introduction

If you are an NRI who has been watching the rupee slide and wondering whether it is finally time to put your savings to work back home, the Reserve Bank of India has just given you a very good reason to pay attention. Over the past few weeks, the central bank has rolled out a series of changes to FCNR(B) deposits, and together they have turned a quiet, low interest product into one of the most talked about fixed income opportunities for NRIs right now.

Open a free account today

Invest in tomorrow with just one click

What Are FCNR(B) Deposits?

FCNR(B) stands for Foreign Currency Non Resident (Bank) deposits. They allow NRIs to hold fixed deposits in India in foreign currencies such as the US dollar, the British pound, or the euro, instead of converting their earnings into rupees. The big appeal has always been that your money stays in the currency you earned it in, so you are not exposed to rupee depreciation. The returns are tax free in India and the funds remain fully repatriable, which means you can move the principal and interest back overseas whenever you want.

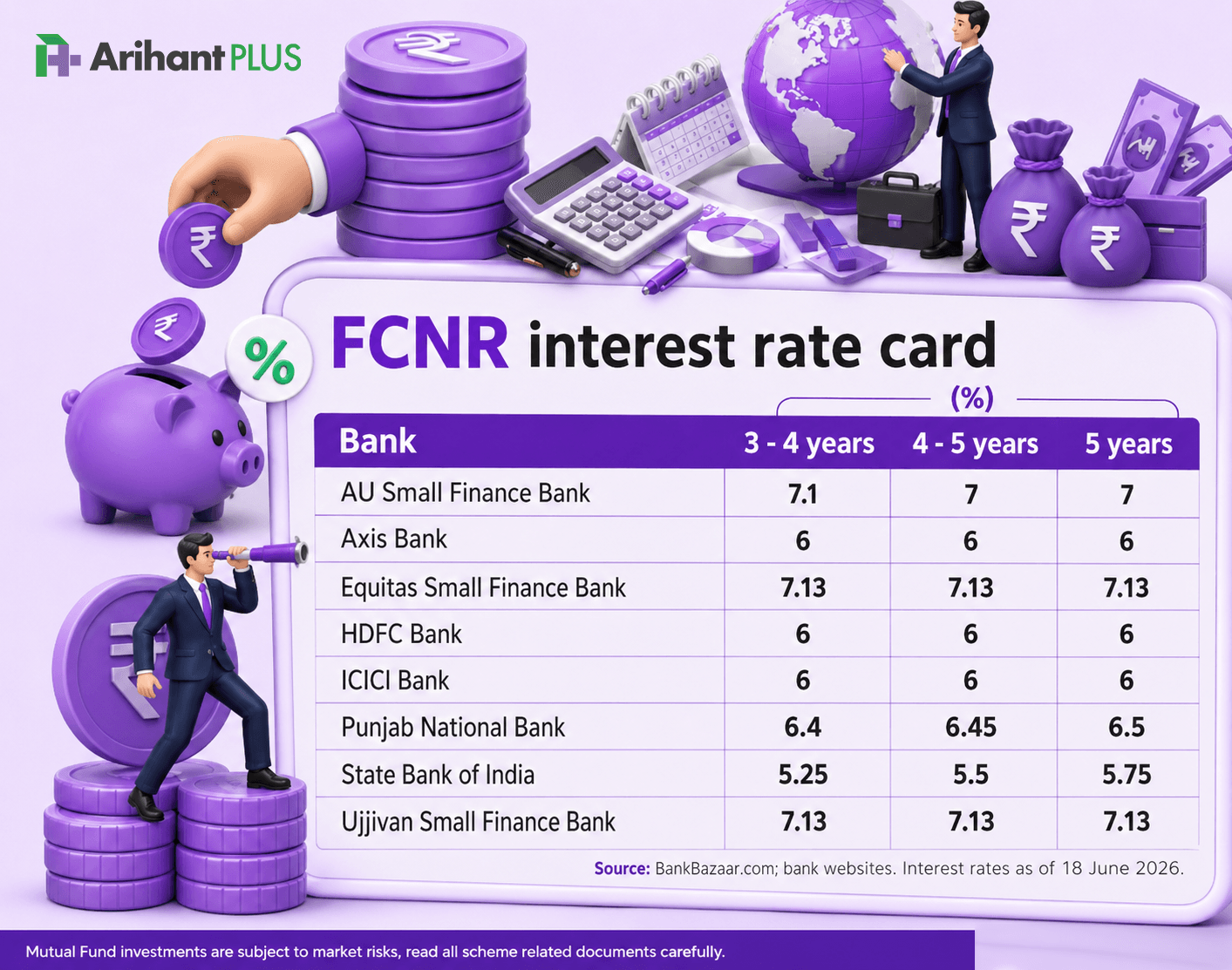

Until recently though, the interest rates on these deposits were fairly modest, usually somewhere between 3.5% and 4%. The reason for that low rate sat quietly behind the scenes, and that is exactly what the RBI has now stepped in to fix.

RBI's Big Change: Absorbing the Hedging Cost

Here is the problem banks have always faced with FCNR(B) deposits. They accept your money in dollars, but they lend it out in rupees. That mismatch creates currency risk, because the bank eventually has to pay you back in dollars regardless of how the rupee has moved in the meantime. To protect themselves, banks buy currency hedges, and those hedges typically cost between 3% and 3.5% a year. That cost does not disappear. It gets passed straight on to depositors in the form of a lower interest rate.

On June 8, the RBI issued a circular that changes this equation entirely.

It introduced a US Dollar Rupee swap facility under which the RBI itself agrees to absorb that entire hedging cost. The facility applies only to fresh FCNR(B) deposits, including renewals, for a minimum tenure of three years and a maximum of five years. Banks sell dollars to the RBI at the FBIL Reference Rate on a spot basis, and buy back the same amount at the same rate once the deposit matures, in multiples of USD 1 million. Each bank can access the facility only once a week, and the amount it is allowed to swap in a given week is capped at the eligible deposits it raised the week before.

There is an added sweetener as well. Deposits raised under this scheme are exempt from Cash Reserve Ratio and Statutory Liquidity Ratio requirements. In simple terms, banks no longer need to keep a portion of this money parked idle with the RBI, so they can deploy more of it and earn more from it.

Put simply, the currency risk has shifted off the bank's books and onto the RBI's, and that single change explains why interest rates have jumped so sharply almost overnight.

Why this is such a Good Deal for NRIs

For NRIs, the appeal of this scheme is straightforward. You get a meaningfully higher interest rate on a deposit that was already tax free in India and fully repatriable. You are not taking on any rupee risk, since your money stays in foreign currency throughout. And because the RBI is absorbing the hedging cost rather than the bank, the higher rate is not coming at the cost of safety. This is still a bank deposit, just a far more rewarding one.

The window is also time bound, which is worth keeping in mind if you are considering it. The scheme closes for new deposits on September 30, 2026, and the swap facility itself closes on October 16, 2026. There are a few caveats too. The RBI's swap cover applies only to the principal, not to the interest earned, and deposits carry a one year lock in before early withdrawal becomes possible at the bank's discretion. Once a bank has swapped a deposit with the RBI, that swap cannot be cancelled, even if you withdraw the underlying deposit early.

Leverage Facility: Returns of Up to 26%

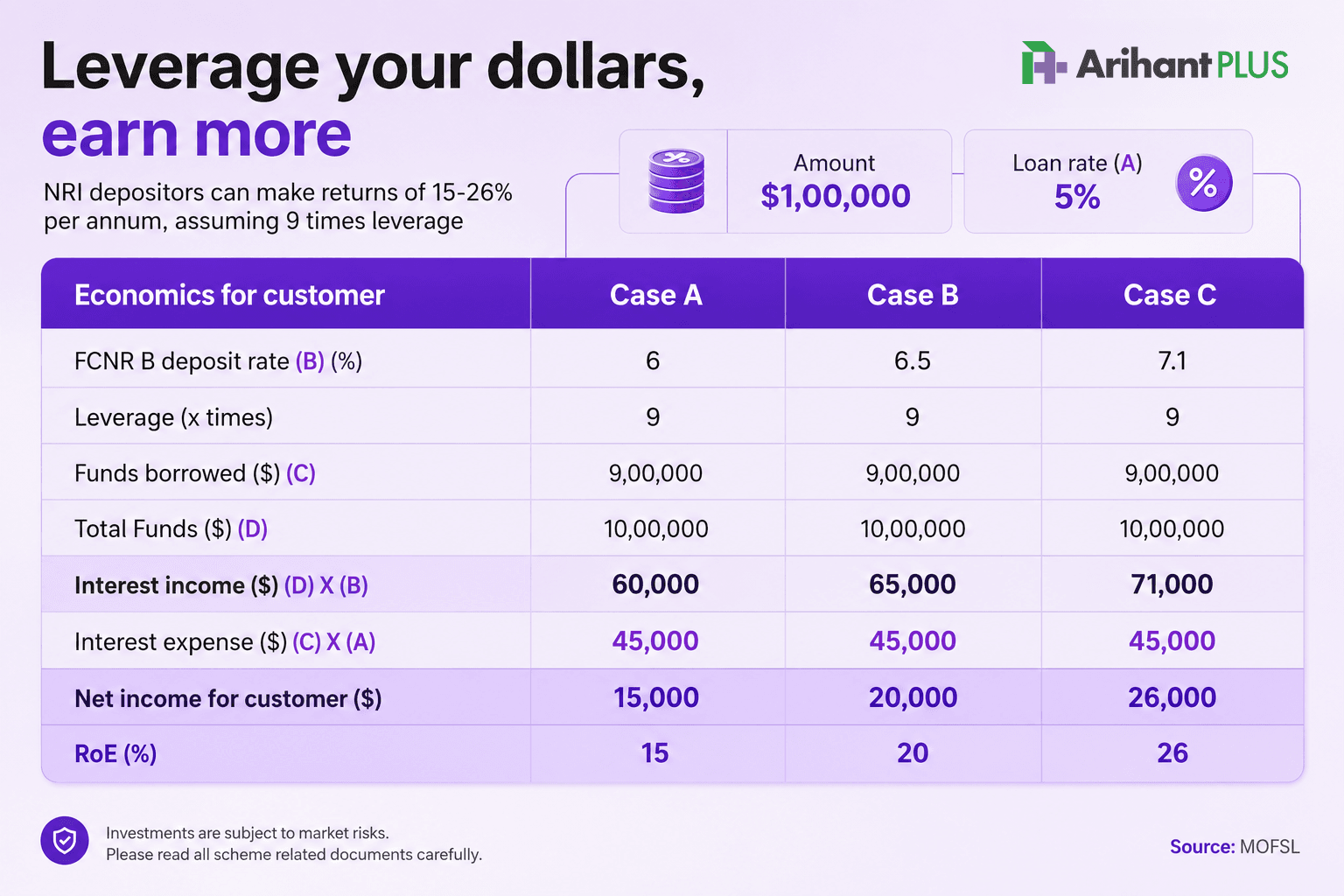

The second major change landed on June 23, when the RBI clarified a question banks had been waiting on. Can they lend against these FCNR(B) deposits?

The answer turned out to be yes. Indian banks, including their overseas branches, can now extend loans or issue standby letters of credit to non residents or overseas lenders against FCNR(B) deposits raised under the swap scheme, and they can place a lien on those funds in the process.

This is the part that has really caught the attention of private bankers and wealthy NRIs. It is not just the higher deposit rate that is exciting people, it is the ability to borrow against the deposit and amplify the return. SBI, for instance, is reportedly offering leverage of up to 9 times the deposit amount. In practice, that means a depositor could place a relatively modest sum in an FCNR(B) deposit, borrow several times that amount overseas using the deposit as collateral, invest the larger sum, and pocket the difference between what they earn on the deposit and what they pay on the loan.

To put a number on it, an NRI depositing $100,000 and borrowing nine times that amount at around a 5% loan rate could end up with effective annual returns ranging from roughly 15% to 26%, depending on the deposit rate secured and the exact terms negotiated with the bank. It is worth noting that the RBI has not prescribed any cap on loan size. That decision has been left entirely to individual banks, which means the exact leverage and terms you get will depend heavily on where you bank and how that relationship is structured.

Should You Look into this?

For NRIs holding foreign currency who do not want the hassle or the risk of converting it into rupees, this scheme is genuinely worth a closer look. It combines currency protection, a noticeably higher yield, full repatriation, and now the option of leverage for those comfortable with that kind of structure. It is rare to see a government backed, bank issued product offer this combination of safety and return at the same time.

The catch is that the window will not stay open indefinitely. With the deposit scheme closing on September 30, 2026, and the swap facility closing on October 16, 2026, anyone seriously considering this should start the conversation with their bank well before the deadline rather than after it.

Related Topics

Vedanta Demerger: Why Aluminium Became the Market’s Favourite/Darling

Rupee Slips Past 95/USD | Factors Driving the Fall Despite RBI Intervention

The Popcorn Trade: How Dhurandhar 2 is driving PVR INOX Stock Higher

Sensex down 8% due to Iran war: Should you pause SIP or buy the dip?

What’s Getting Cheaper & Costlier in Budget 2026: A Simple Money Guide

Maruti Q3FY26 Profit Up 4%: Losing Grip on India’s Car Market?

Gold & Silver Rally Amid US–Venezuela Conflict: What Should Investors Do?

New Year, New Financial Goals: Make SIP Your 2026 Resolution

How Jane Street Snatched ₹36,500 Crore While India's Youth Lost Everything