Vedanta Demerger: Why Aluminium Became the Market’s Favourite/Darling

By

Arihant Team

Vedanta’s demerger saw four new companies list, but Vedanta Aluminium became the clear market favourite. It opened at ₹522, a 331% premium to its discovered price of ₹121. Strong aluminium fundamentals, low-cost operations, high EBITDA, and backward integration drove investor interest. The market preferred aluminium over power, oil & gas, and iron & steel on listing day.

In This Article

- Introduction

- Why did Vedanta split its business?

- Vedanta Demerger Listing Scoreboard

- Why did Vedanta Aluminum (VAML) rally today?

- Inside Vedanta’s Debt Story

- Investor Takeaway

Introduction

This morning, India's stock exchanges welcomed four new companies before most people had finished their chai.

Vedanta Aluminium Metal listed at ₹522 on the NSE, at a staggering 331.3% premium to its price discovery of ₹121.03. To put that plainly: the special pre-open session priced this company at ₹121, and the market opened at more than four times that number, barely an hour later.

The other three? Vedanta Power, Vedanta Oil & Gas, and Vedanta Iron & Steel all opened at discounts to their discovered prices.

So what just happened and why did aluminium run away from the pack?

Open a free account today

Invest in tomorrow with just one click

Why did Vedanta split its business?

To understand today, you need to go back to September 2023, when Anil Agarwal announced that Vedanta, India's sprawling metals and mining conglomerate would be broken into independently listed entities.

The logic was quite textbook.

When unrelated businesses are bundled together, markets struggle to price any of them properly, and the whole thing trades at what analysts call a "conglomerate discount." Separate them out, and each business gets valued on its own fundamentals, attracting investors who actually want exposure to that specific commodity or sector.

After nearly three years of NCLT approvals, creditor meetings, and regulatory clearances, the demerger became effective May 1, 2026. Shareholders holding Vedanta on the record date received one share each in all four new companies for free, credited directly to their demat accounts.

Today was the first day they could actually trade those shares.

Vedanta Demerger Listing Scoreboard

Here's how opening prices compared to discovered prices on the NSE:

Why did Vedanta Aluminum (VAML) rally today?

The premium was not random, and three concrete, verifiable reasons listed below explain the move:

VAML’s Aluminium Dominance

VAML holds around 60% of India’s primary aluminium production, including BALCO, with capacity of 2.88 mtpa as of March 31, 2026. It is also among the world’s lowest-cost aluminium producers, supported by expanded alumina capacity, large smelting assets, and backward integration through captive coal and bauxite blocks.

In FY2026, its aluminium EBITDA rose 48% YoY to nearly ₹25,500 crore, with EBITDA per tonne at about $1,188.

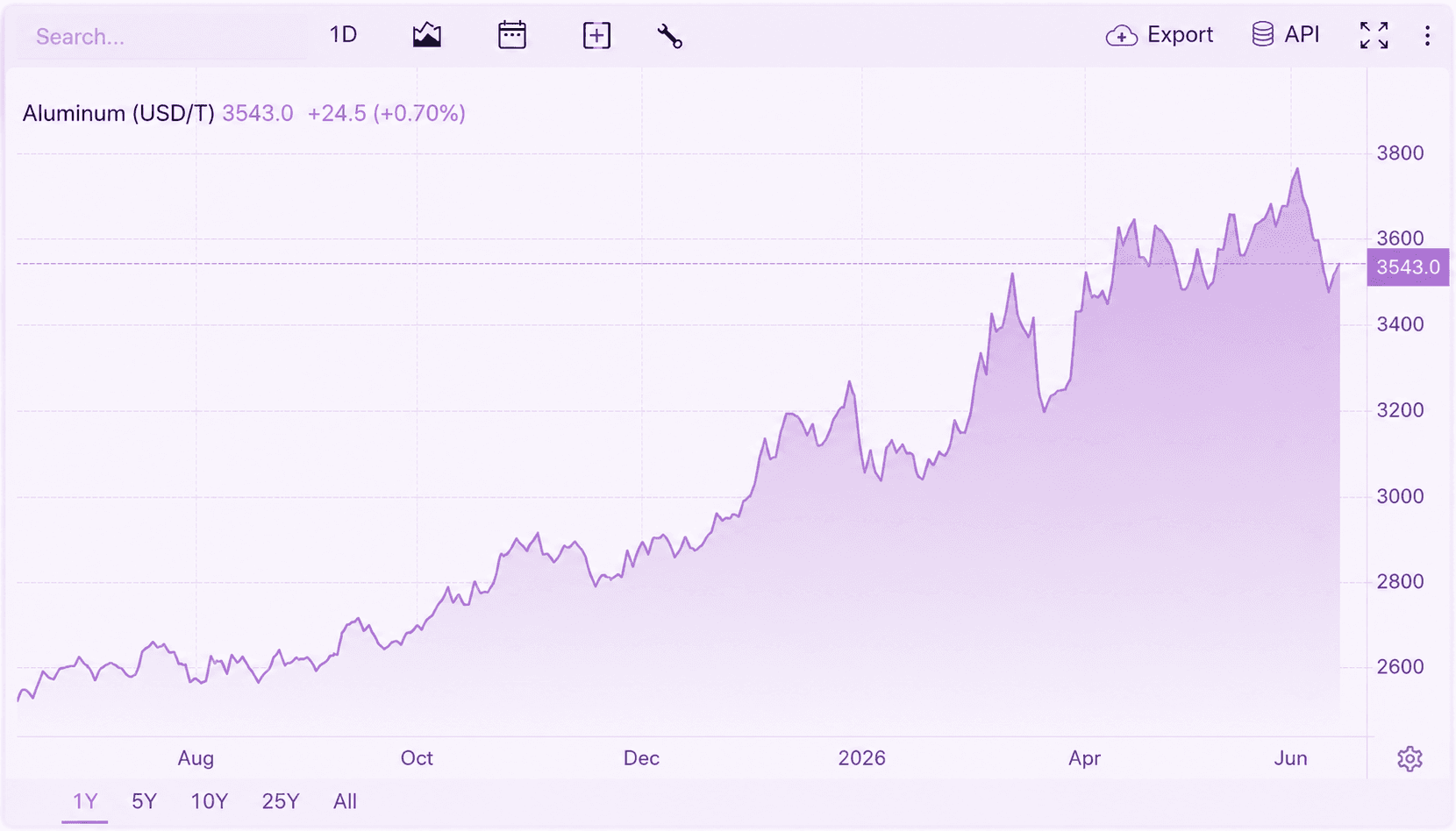

Aluminium prices are elevated, and that directly moves VAML's earnings.

Aluminium prices remain elevated, with LME aluminium around $3,540/tonne as of mid-June 2026. Higher aluminium prices improve VAML's realizations, and given its low-cost production base, a large part of the price increase flows through to profits.

Source: Trading economics

Backward Integration Strengthens VAML’s Cost Edge

VAML’s major aluminium capex projects are nearing completion, and their full benefits should improve the company’s operating profile. The alumina refinery expansion and the upcoming captive coal and bauxite blocks are expected to strengthen cost competitiveness and reduce the impact of raw material price volatility on profits.

VAML has also proposed a ₹1.3 lakh crore greenfield smelter in Odisha, though it remains at the discussion stage with no firm capex commitment.

Inside Vedanta’s Debt Story

The demerger wasn't just about unlocking value. It was also, quietly, a balance sheet restructuring exercise. According to estimates, here's how the ₹53,400 crore in net debt is allocated across the five entities:

VAML takes on the heaviest debt load and that's not a coincidence. The aluminium business holds the largest physical assets, the most capital-intensive operations, and proportionately the highest historical borrowings within the group. But it also generates the most EBITDA, bringing the net debt-to-EBITDA ratio of under 1.3x.

By contrast Vedanta Power carries ₹7,500 crore in debt against estimated FY26 EBITDA of only ~$0.2 billion implying a net debt-to-EBITDA of approximately 4.7x. That's the real reason Vedanta Power listed at a discount. It's not that the business is bad; it's that the leverage is uncomfortably high relative to its near-term earnings.

Oil & Gas, meanwhile, emerges debt-free with a structural advantage but faces exploration uncertainty and a regulatory environment that the market is cautious about.

Investor Takeaway

What Vedanta has done is hand every shareholder a basket of five pure-play companies. Some will hold them all. Many will sell what they don't want and concentrate into what they believe in.

The market has spoken clearly about which one it believes in most at least on Day 1. Whether VAML's fundamentals justify a 331% premium over its discovered price, or whether this is partly listing-day excitement, will be answered over the coming quarters as standalone financials start flowing.

For now, one thing is certain: when you demerge a conglomerate and let the market speak, it doesn't split the difference equally. It picks a favourite.

Today, it picked aluminium.

⚠️ This blog is for informational purposes only and is not investment advice. Prices cited are from opening trade on June 15, 2026, and may have changed.

Related Topics

Rupee Slips Past 95/USD | Factors Driving the Fall Despite RBI Intervention

The Popcorn Trade: How Dhurandhar 2 is driving PVR INOX Stock Higher

Sensex down 8% due to Iran war: Should you pause SIP or buy the dip?

What’s Getting Cheaper & Costlier in Budget 2026: A Simple Money Guide

Maruti Q3FY26 Profit Up 4%: Losing Grip on India’s Car Market?

Gold & Silver Rally Amid US–Venezuela Conflict: What Should Investors Do?

New Year, New Financial Goals: Make SIP Your 2026 Resolution

How Jane Street Snatched ₹36,500 Crore While India's Youth Lost Everything