Aastha Spintex IPO 2026 | Should You Apply?

By

Arihant Team

India's textile sector is threading a structural comeback driven by the China+1 shift, government PLI incentives, and rising export demand. Aastha Spintex IPO closes Wednesday, July 1st, and it's sitting right in the path of that tailwind. But there's an aggressive acquisition in play, real customer concentration risk, and a valuation that's pricing in a lot of optimism. Is it actually worth applying?

In This Article

- Introduction

- Key IPO Details: Aastha Spintex IPO

- Business Overview

- Where Will Aastha Spintex's IPO Proceeds Go?

- Financial Performance

- Peer Comparison

- Key Risks

- Investor Takeaway

- FAQs

Introduction

India's cotton yarn industry is at an inflection point. Global brands are cutting their China exposure quietly but deliberately and integrated Indian manufacturers with the right certifications and export muscle are the ones picking up that business.

Aastha Spintex is one of them. A Gujarat-based cotton ginning and spinning company that's grown profits 22x in two years, built out a renewable energy cost advantage most peers don't have, and is now chasing a capacity-doubling acquisition funded entirely by fresh IPO money.

The offer: ₹170 crore, all fresh issue, 1.25 crore equity shares at ₹125-₹136 per share.

The real question isn't whether the story is interesting. It is. The question is whether the price is fair and whether Falcon Yarns, the acquisition at the heart of this IPO, is as good a deal as management thinks it is.

Open a free account today

Invest in tomorrow with just one click

Key IPO Details: Aastha Spintex IPO

Business Overview

Think of Aastha Spintex as a mill-to-market cotton company. It was set up in 2013 and runs out of Halvad, Morbi; in the middle of Gujarat's cotton belt. The facility is 65,762 sq. metres, runs 24x7, and turns out carded, combed, and compact combed cotton yarns across Ne 26 to Ne 40 counts, along with cotton bales and by-products.

Everything it sells goes to other businesses. Textile manufacturers, yarn exporters, bulk buyers, fabric processors, Aastha's world is entirely B2B. Its yarns end up in denim, terry towels, shirting, bed sheets, sweaters, socks, home textiles, and industrial fabrics.

The structural advantage is integration. Most spinners buy their cotton bales from the market. Aastha Ginning Division processes harvested cotton into bales at 12,000 MT per annum, and the Spinning Division converts those bales into finished yarn at 7,700 MT. In a commodity-adjacent business, controlling your raw material intake matters. It's not a moat, but it's a cushion.

A few other details worth flagging:

Certifications: The company has GOTS and OEKO TEX certifications. These are not marketing badges. They are actual entry requirements for quality sensitive export markets in Europe and the United States. A supplier does not get approved by brands like H&M or Inditex without these certifications.

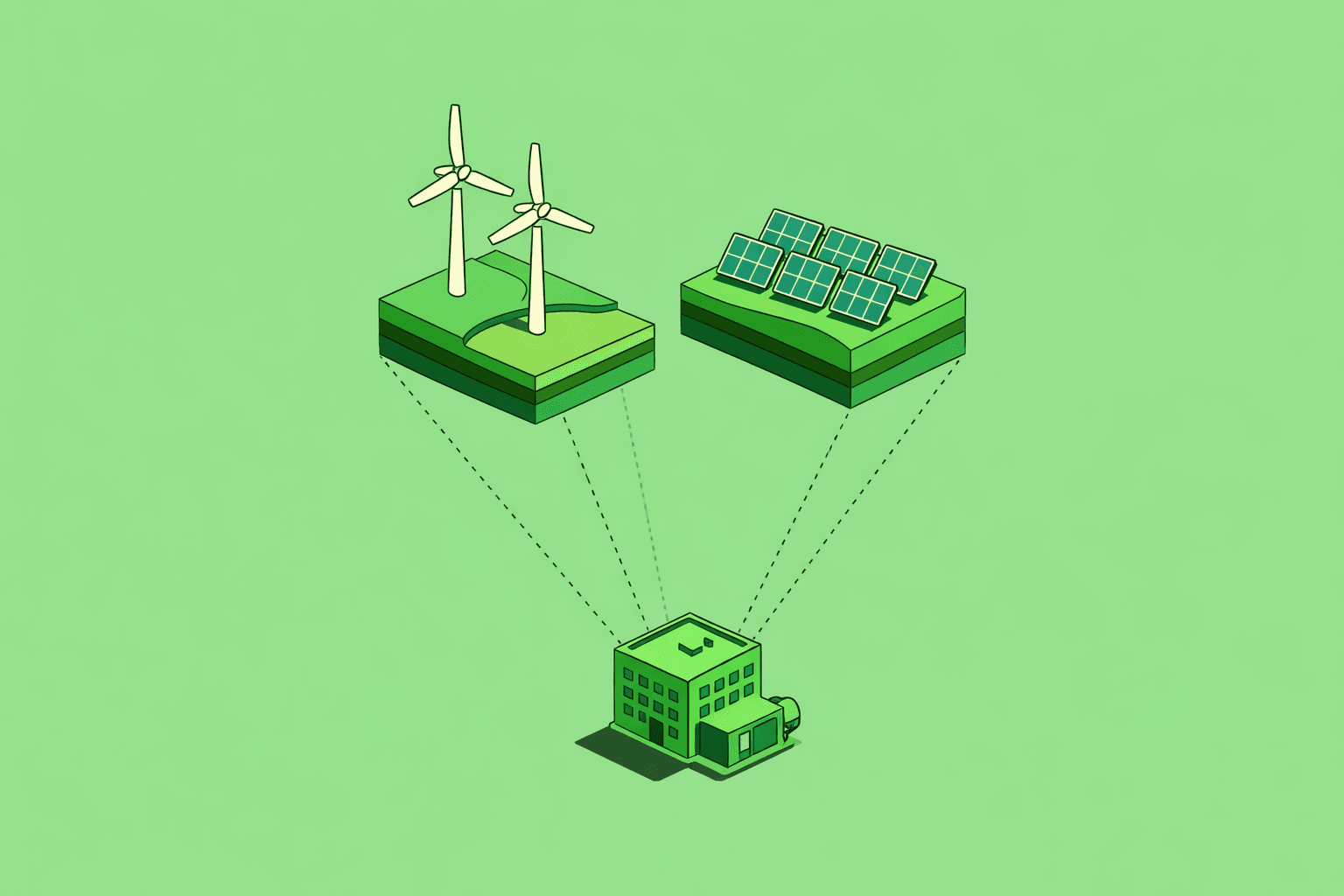

Renewable energy: The company also has 7.7 MW of captive renewable power capacity. This includes 1 MW of rooftop solar, 4 MW of ground mounted solar, and 2.7 MW of wind energy. Together, these sources cover roughly 80 percent of the plant’s power requirement. This has reduced energy costs by 45 percent, from ₹13.46 crore in FY23 to ₹7.36 crore in FY25. That is a real and recurring cost advantage.

- Capacity utilisation: Capacity utilisation stood at 96.57 percent in FY25. There is no idle capacity here. The plant is running almost at full capacity.

Where Will Aastha Spintex's IPO Proceeds Go?

Here's one thing that separates this IPO from a lot of what's been hitting the market: it's a 100% fresh issue. No promoter is selling a single share. Every rupee raised goes into the company — not into anyone's pocket.

The complicated part is what the company's doing with it.

₹111.51 crore; roughly 65.6% of gross proceeds is earmarked for acquiring Falcon Yarns Private Limited. There's also an inter-corporate deposit component to fund Falcon's working capital post-acquisition. The remainder is for general corporate purposes, which is the standard catch-all.

Financial Performance

The numbers Aastha Spintex has put up over the past three years are genuinely hard to ignore. They are also the first thing investors should stress test.

Revenue went from ₹239.69 crore in FY23 to ₹352.17 crore in FY25. That is a 47 percent expansion over two years. For the nine months ending December 2025, the company clocked revenue of ₹314.02 crore. That annualises comfortably above FY25 levels.

Then comes the profit story. PAT was ₹1.06 crore in FY23. That was essentially close to zero. By FY25, PAT had increased to ₹22.92 crore.

That is a 22 fold increase. For 9M FY26, PAT stood at ₹17.56 crore. Annualised, that comes to roughly ₹23 crore to ₹24 crore. That is broadly consistent with FY25.

EBITDA margins have gone from 4.85% to 13.37% in two years: over 850 basis points of expansion.

D/E ratio moved from 1.35 to 0.78 between FY23 and FY25, which is a real signal of financial discipline rather than just accounting. But there's a caveat: operating cash flows have been negative. ₹18.13 crore negative in FY25, ₹13.55 crore negative in 9M FY26. The company is profitable on paper but burning cash in operations, driven by rising working capital requirements. Post-Falcon, those working capital needs are going to get bigger, not smaller.

Peer Comparison

Aastha's RHP lists three peers: Ambika Cotton Mills, Lagnam Spintex, and Pashupati Cotspin.

At ₹136 (upper band), Aastha is asking ~26x on FY25 earnings and somewhere between 22–25x on annualised 9M FY26 numbers.

Here is the data formatted into a clean table that you can easily copy and paste into Excel, Word, or any document:

On straight P/E, Aastha is roughly double what Ambika and Lagnam trade at and those two are the only genuinely comparable businesses. Ambika Cotton has 38 years of history and an export moat built around fine-count specialty yarns. It trades at 13.8x. Lagnam operates in a similar count range to Aastha and trades at 9.8x.

Pashupati Cotspin's P/E of ~132x is an outlier driven by compressed earnings, not a benchmark anyone should use.

Key Risks

Single Customer Concentration: Aastha channels virtually all its sales outside Gujarat through one reseller: 7 Seas Impex. In FY23, that single entity accounted for 66.61% of total revenue. By FY25 it was 33.88%, and 22.99% in 9M FY26. The trend is clearly improving. But 23% of revenue running through one pipe is still a concentration risk most investors would flag in any other context.

Falcon Acquisition Risk: This is where most of the IPO money is going, and it's the variable that'll make or break the thesis. Falcon's net profit has dropped over 66% between FY23 and FY25. The price Aastha is paying has been marked up significantly from an earlier internal buyback.

Cotton Price Volatility: Cotton is bought once a year, during harvest season, and stored in bulk. That means Aastha is making large inventory bets on where cotton prices will be with no ability to hedge the timing. A bad season or a currency move can squeeze margins fast.

Negative Operating Cash Flows: The company has been PAT-positive for two years but cash-flow-negative from operations in both FY25 and 9M FY26. That's a tension worth watching. Post-Falcon, the working capital intensity goes up. If the cash flow trend doesn't reverse, the company will need either debt or equity to fund growth, both of which have costs.

Legal and Tax Proceedings: Ongoing criminal and tax proceedings involving the company and its promoters. Adverse outcomes could affect operations and perception. The RHP has the details; worth reading.

- Cyclicality: Cotton spinning isn't a consumer staple business. Margins compress when cotton spikes or demand softens and it can happen fast. Running at 96.57% utilisation means there's almost no buffer if orders slow down.

Investor Takeaway

Aastha Spintex isn't a promoter-exit vehicle dressed up as a growth play, the IPO is entirely fresh, the money is going into the business, and the operating performance over the last two years has been genuinely strong.

If you're a growth-oriented investor comfortable with textile cyclicality and happy to sit through two or three years of integration noise, this has enough going for it to be worth considering. If you prefer to see the Falcon chapter play out before committing, waiting for post-listing price discovery is a perfectly rational call, there'll likely be multiple opportunities to enter at reasonable levels once the acquisition's actual progress becomes visible in quarterly numbers.

FAQs

What are the IPO dates for Aastha Spintex IPO?

The IPO opens June 29, 2026 and closes July 1, 2026. Listing on BSE and NSE is scheduled for July 6, 2026.

What is Aastha Spintex IPO GMP?

GMP is unofficial, unregulated, and volatile. It shouldn't drive your application decision either way. Check here for the current number, but treat it as sentiment data, not a forecast.

What is the lot size for retail investors?

110 shares per lot. Minimum investment at the upper band: ₹14,960.

Is Aastha Spintex IPO a fresh issue or an OFS?

Entirely a fresh issue: 1.25 crore shares aggregating ₹170 crore. No promoter is selling. All proceeds go to the company.

Where will the IPO proceeds be used?

₹111.51 crore goes towards acquiring Falcon Yarns Private Limited. The rest covers Falcon's working capital requirements and general corporate purposes.

Should I invest in the Aastha Spintex IPO?

That depends on your risk appetite and time horizon. The profitability turnaround is real, the macro tailwinds are genuine, and this isn't a promoter-exit IPO. But the Falcon acquisition is a high-stakes bet on a business with deteriorating financials, the valuation isn't cheap relative to peers, and operating cash flows have been negative. Growth investors with patience may find it interesting. Conservative investors are better off watching the first few quarters post-listing before deciding.

Related Topics

Important IPO terms all investors should understand before investing

Meesho IPO Opens on 3Dec - Is this ₹5,421 crores IPO worth investing?

10 Things to Know About Sudeep Pharma IPO: Date, Price, GMP & Complete Review

Canara Robeco AMC IPO: Should You Apply for MF Giant’s Public Debut?

Smartworks Coworking Spaces Limited IPO: 10 Key Things to Know Before Investing

Travel Food Services Limited IPO: 10 Key Things to Know Before Investing

Ellenbarrie Industrial Gases Limited IPO: 10 Key Things to Know Before Investing

HDB Financial Services Limited IPO: 10 Key Things to Know Before Investing

Sambhv Steel Tubes Limited IPO: 10 Key Things to Know Before Investing

Indogulf Cropsciences Limited IPO: 10 Key Things to Know Before Investing

Prostarm Info Systems Limited IPO: 10 Key Things to Know Before Investing

Aegis Vopak Terminals Ltd IPO: 10 Key Things to Know Before Investing

Schloss Bangalore Limited IPO: 10 Key Things to Know Before Investing

Belrise Industries Limited IPO: 10 Key Things to Know Before Investing

Hexaware’s Billion Dollar Markets Hits in Bear Market: Should You Invest?