Beyond the Dark Store: Is Advertising Zepto's Real Business?

By

Arihant Team

Zepto may be building an advertising business on top of quick commerce. Grocery delivery brings frequent users but has thin margins and high costs. Ads offer higher-margin revenue by targeting customers ready to buy. Investors should watch if ad revenue can improve Zepto’s profitability.

In This Article

- Introduction

- Inconvenient Truth About Grocery Economics

- Advertising: The Hidden Revenue Engine

- This Pattern Is Showing Up Across All Three Players

- How Zepto Is Using Its IPO Money

- What Retail Investors Should Monitor Over the Next 5 Years

- Investor Takeaway

Introduction

Walk into any quick commerce pitch meeting or read any analyst report on Blinkit, Zepto, or Swiggy Instamart and you'll hear the same framing: dark stores, delivery speed, and grocery wallet share. The race, as the story goes, is about getting to your door in ten minutes before the other guy does.

This is not arbitrary. Grocery is the single best acquisition tool in consumer commerce. It is daily, habitual, and non-negotiable. People don't "try" grocery shopping the way they try a new streaming service. They need it, regularly, repeatedly, for life.

This is the foundation of the entire quick commerce thesis. Indians don't do one big monthly grocery run the way consumers in the US or Europe might. They shop often, in small quantities, close to home. That behaviour is deeply ingrained and it creates the opening for a 10-minute delivery model.

Most strikingly, quick commerce now accounts for over two-thirds of all online grocery orders in India.

Inconvenient Truth About Grocery Economics

Grocery delivery sounds like a great business from a distance. People need it. They order repeatedly. The market is enormous.

Up close, the economics are brutal.

Grocery margins are thin at the product level, often 5-15% at best, depending on category. Every order requires a picker inside the dark store, a packaging cost, and a rider on a bike. Dark stores require rent, cold storage for perishables, and round-the-clock staffing.

Customers are extremely price-sensitive and will switch platforms for a ₹20 discount.

Zepto's own FY26 numbers tell the story plainly.

Revenue from operations more than doubled to ₹22,624 crore but net losses widened 26% to ₹5,905 crore. Total expenditure surged to ₹29,027 crore, with procurement of traded goods alone consuming 63% of all costs.

The problem is not unique to Zepto. Swiggy Instamart posted an adjusted EBITDA loss of ₹858 crore in Q4 FY26. Only Blinkit, the largest player with 45% market share and the greatest scale advantage, managed to reach adjusted EBITDA profitability and that happened for the first time in Q3 FY26, four years after the quick commerce model took off in India.

The lesson: grocery delivery creates frequency and trust. But on its own, it barely pays for itself. You need something else riding on top of it.

Advertising: The Hidden Revenue Engine

Now, think about this.

Every time a customer opens Zepto, they are in an unusually valuable mental state. They are not scrolling Instagram half-distracted. They are not passively watching YouTube. They are actively shopping with money in hand. They are about to buy something.

Brands know this. And they are willing to pay a significant premium to reach customers at exactly that moment.

This is why advertising is structurally different from grocery delivery. It has almost none of the same cost drivers. Once the ad technology is built: the bidding engine, the attribution system, the campaign management tools, incremental advertising revenue is largely margin.

You don't need another dark store. You don't need another rider. You need the platform to already have the users, which Zepto has been spending years and billions acquiring through grocery.

According to the company's DRHP, advertising revenue grew from just ₹49 crore in FY24, to ₹651 crore in FY25, and then to ₹1,636 crore in FY26!! A more than 33-fold increase in two years, growing far faster than the overall business.

Critically, some of these brands like AU Small Finance Bank and CRED don't even sell products on Zepto. They are buying access to Zepto's user base, not shelf space.

This Pattern Is Showing Up Across All Three Players

This is no longer a Zepto story; it is a structural shift across quick commerce.

Goldman Sachs values Blinkit at approximately $13 billion, higher than Zomato's own food delivery business. Advertising and in-app sponsored listings are a named component of Blinkit's revenue model, alongside product margins and delivery fees.

Swiggy Instamart has been explicit that advertising is a strategic lever for improving its economics. Management confirmed that Instamart expects advertising to account for ~7% of its quick commerce GMV going forward.

Industry estimates in Zepto's own DRHP suggest that quick commerce platforms collectively generated ~₹6,000 crore in advertising revenue in CY2025, and that quick commerce's share of India's total digital advertising market could rise from approximately 1% in CY2023 to nearly 5% by CY2025.

The pattern is consistent: every major player is building the same type of business on top of their grocery operations. The grocery brings the customer while the advertising captures the margin.

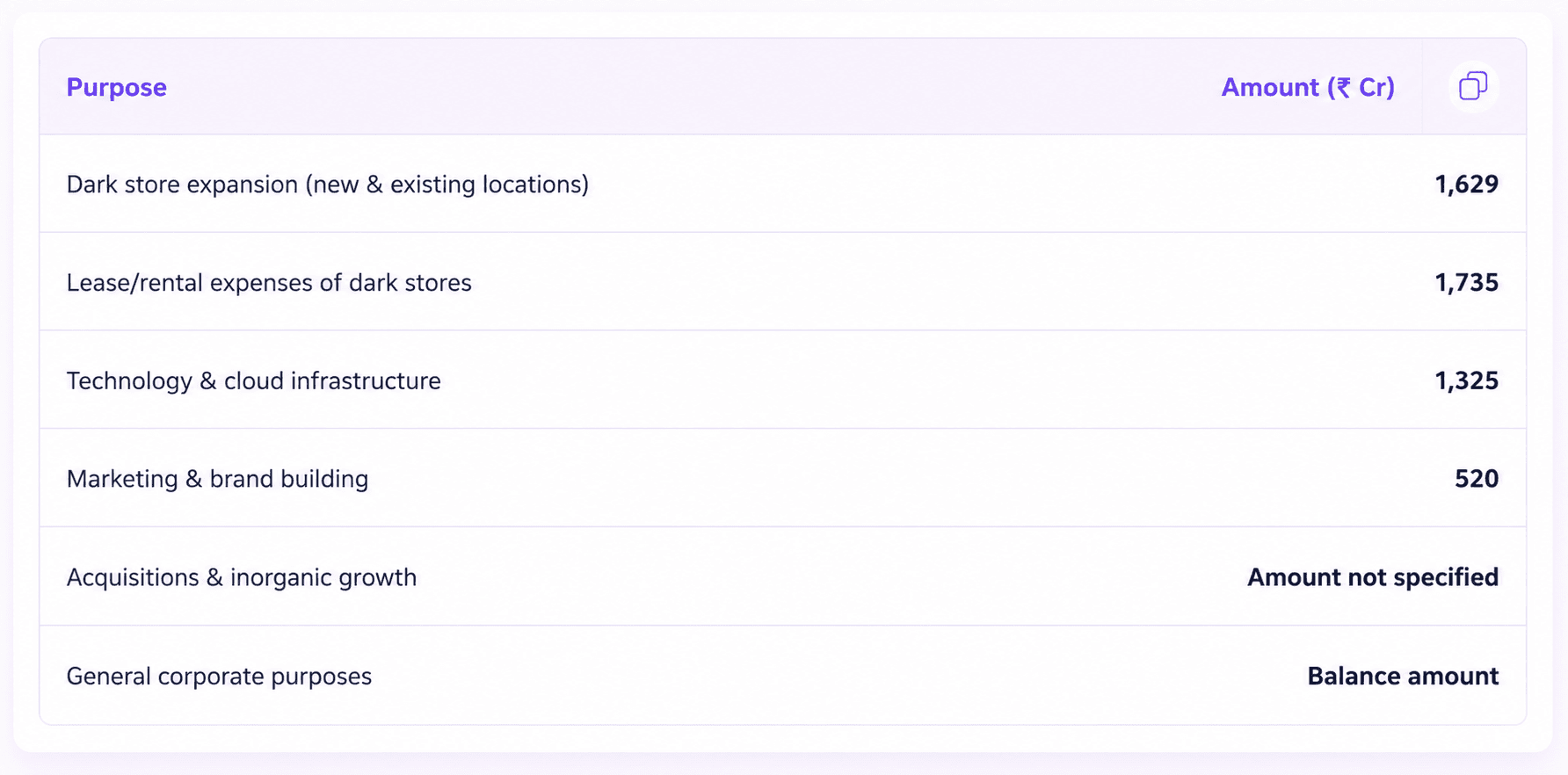

How Zepto Is Using Its IPO Money

Zepto is raising ₹8,010 crore through its IPO fresh issue.

On the surface, this looks like a grocery logistics company funding more logistics. But read it again. The ₹1,325 crore technology allocation is substantial and the advertising tech stack (Jarvis, Zepto Atom, attribution systems, the bidding engine) lives inside that investment. The ₹520 crore for brand promotion will also shape Zepto's ability to attract more premium advertising partners.

Investors should be clear-eyed: the majority of capital is genuinely directed at physical infrastructure. Zepto is still building a delivery network first. But the technology investment, if it materially advances the ad platform, could produce returns with a completely different margin profile from dark stores.

What Retail Investors Should Monitor Over the Next 5 Years

If you are tracking Zepto as a public company, here are the specific metrics worth watching:

Advertising revenue as a share of total revenue: It is currently 7.2% of operating revenue. The question is whether it can approach ~20% over the next three to four years. At that level, the margin profile of the business changes materially.

Take rate trajectory: The take rate is what Zepto keeps from every transaction after accounting for inventory. Advertising income directly lifts this. Blinkit's take rate, boosted by ads, was meaningfully higher than Instamart's in the most recent available comparisons. Watch whether Zepto's equivalent metric expands.

Number of non-endemic advertisers: Banks, fintechs, insurance companies, and consumer brands unrelated to groceries represent an advertising market far larger than FMCG. If this segment grows, it signals that Zepto's platform value has transcended the grocery category.

Per-order loss and EBITDA trajectory: Watch whether advertising revenue is actually closing the gap between revenue and cost, or just making the losses look slightly less alarming.

- Dark store productivity vs. ad revenue productivity: If Zepto eventually breaks out contribution margins by segment as Amazon does between its retail and services businesses, this will be the clearest signal of whether the platform is becoming an advertising business wearing a grocery delivery hat.

Investor Takeaway

Quick commerce companies built their businesses on the most fundamental consumer need: food, delivered fast. That is why grocery was always the starting point. It creates frequency, trust, and an enormous captive audience.

But grocery alone does not produce the returns that justify multi-billion dollar valuations. The unit economics are hard, the competition is fierce, and the capital requirements are relentless.

Advertising changes that equation because it monetises the same customer, the same session, the same moment of purchase intent, at a fraction of the marginal cost.

The one question that will truly define Zepto's long-term valuation is whether Zepto can make more money from the attention of that customer than from the groceries themselves.

Needless to say, the market will be watching!

Related Topics

NSE Extends F&O Market Close to 3:40 PM: What Traders Must Know

Elon Musk’s $119 Billion Terafab Bet: Can It Reshape AI Chips?

Rupee Crashes to ₹96: How Investors Can Profit From the Fall

The Rise of India’s Defence Sector: Stocks, Trends & Opportunities

SEBI introduces Verified Badge for Trading Apps to Curb Fake App Scams

TCS Q4 Concall: AI Infrastructure to Drive the Next Growth Cycle

Oil Is Surging After The Iran Strikes. So Why Isn’t Gold Following?

Union Budget Day & Market Behaviour: 15 Year Trend Analysis (2011-2025)

Infosys ₹18,000 Crore Share Buyback: Record Date & Why Promoters Opted Out?

Nifty 50 Performance Since Last Muhurat Trading: Nifty Top 10 Performers

Diwali Muhurat Trading: Can Nifty’s 7-Year Winning Streak Continue?

Tata Motors Demerger Gets NCLT Nod: What Shareholders Must Know

Muhurat Trading 2025 on 21 Oct: Everything You Should Know

Tuesday is the New Thursday: NSE & BSE Expiry Shift from Sep 2025

Axis Bank Q1FY26 Results: A Mixed Bag, but Long-Term Picture Still Intact